Yesterday, a tanker docked in Tokyo Bay carrying 900,000 barrels of crude oil. Half a day’s worth of Japanese consumption. National television ran the story.

The cargo left Texas near the end of March, squeezing through the Panama Canal.

It was the first US oil shipment to reach Japan since the Iran war began in late February.

That this made national news tells you everything.

Japan sources over 90% of its crude through the Strait of Hormuz. With the Strait effectively closed, Tokyo and Seoul have already drawn tens of millions of barrels from strategic reserves.

Now they’re routing American energy halfway across the planet.

This is what a country looks like under pressure.

Beijing isn’t blinking

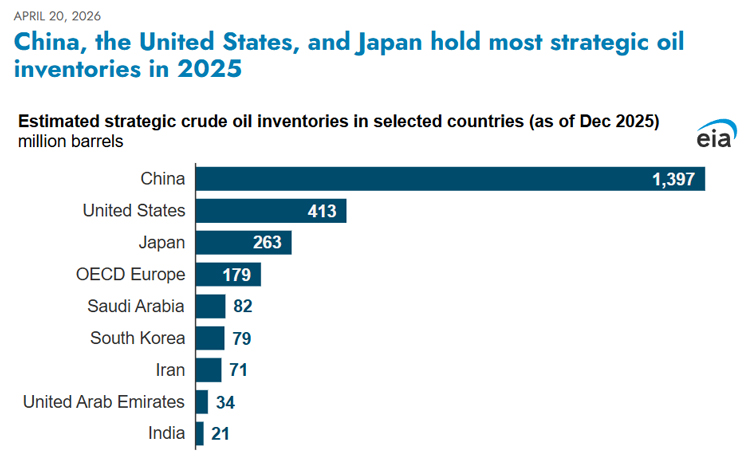

Now look at China.

China’s commercial and strategic crude stockpile is estimated at 1.2–1.4 billion barrels.

That’s more than three times the US Strategic Petroleum Reserve.

Source: EIA

[Click to open in a new window]

Since the war began, that hoard has shrunk by less than one million barrels.

Less than one million. In two months. With the world’s largest oil chokepoint shut.

It seems Beijing is rerouting around the shock rather than running down stockpiles.

State refiners have cut their processing rates and resold light-crude cargoes — now trading at a premium — to Taiwan and Indonesia, according to Bloomberg.

While so-called independent ‘teapot’ refiners in Shandong, fed mostly by sanctioned Iranian and Russian crude, have lifted outputs to multi-year highs.

But they are neither independent nor teapot-sized; they’re massive operations specialising in heavy crude from Russia, Venezuela and Iran.

Beijing has handed them extra import quotas, the State’s signal for ‘get to work’.

Iranian oil purchases are set to hit a record near 1.9 million barrels a day this month, according to Kpler.

Iranian crude is now trading at a premium against Brent. China keeps buying anyway.

Beijing also suspended diesel and gasoline exports in early March, keeping domestic fuel at home.

The pattern is hard to misread. China is paying twice as much as last year for sanctioned barrels rather than drawing on its own reserves.

This isn’t a country thinking about short-term pain. It’s a country hedging against something worse.

The export squeeze

The hoarding extends well beyond crude.

China’s export restrictions affect a slate of materials Australia’s economy depends on. Layered on top of Hormuz disruption, the picture is grim.

Below, in blue, shows what the Iran conflict has hit. And in red, you can see China’s global share.

Source: Asia Global Institute

[Click to open in a new window]

Sulphuric acid is the standout. Roughly half of its global trade is blocked by the Hormuz closure. Now, Beijing says it will ban all exports of the acid in May.

Urea faces a 35% blockage from the Strait, plus 9% under China’s restrictions.

Phosphates are down 25% plus ~13% from China. Jet fuel, diesel, and gasoline are squeezed by similar percentages.

Sulphuric acid matters because it is the working fluid of base metals processing.

Australian copper and nickel producers run heap-leach and pressure-leach circuits that consume it by the trainload.

Combined with a diesel shortage, this supply gap will eventually bite.

Just look at copper powerhouse Chile. In 2025, they bought nearly 1/3rd of China’s sulphuric acid.

China’s shipments in March? Zero.

Cost warnings are now trickling into miners’ reports as they scramble for alternative supplies.

What Beijing might be telling us

So, back to the question. What is China seeing that markets are not?

Three possibilities are on the table.

The first is that Beijing expects Hormuz to remain disrupted for longer than we’re pricing.

The second is that China is hedging against a broader regional escalation. Saudi infrastructure has already been struck. The fragile ceasefire could fold.

Third, which markets aren’t pricing at all, is that China is preserving its options for a future event of its own choosing.

A Taiwan scenario. A trade rupture. Anything in which oil access becomes politicised in an afternoon. China’s hoarding would then give it an extraordinary advantage.

You don’t have to settle on one explanation. You only have to notice that Beijing is behaving as though the current economic pain isn’t the main event.

Where to from here?

There is some hope for a new deal. Axios’s White House insiders claim Iran has tabled a new deal, pushing the nuclear question to a later date, but opening the Strait.

From Washington’s view, the blockade is filling Iranian oil storage to a level that will eventually force Tehran to negotiate.

Like many of Trump’s comments, there’s a grain of truth in his recent claims that Iran’s pipes will explode in three days if they don’t ship oil soon.

Pipelines don’t actually explode when oil stops flowing. The real pressure point is at the wells.

Many of Iran’s fields are mature, water-flooded reservoirs that don’t tolerate sudden shutdowns.

Stop the pumps, and you risk permanent damage. Pressure decline, water contamination, and lower ultimate recovery when you try to restart.

The thing that breaks isn’t the pipeline. It’s the reservoir.

Iran’s main export terminal at Kharg Island handles around 90% of its crude exports, and with the US blockade preventing tankers from loading, the onshore tanks are filling up.

Tanker Trackers reckons there’s about 13 million barrels of spare room left, with roughly 1 million barrels still flowing in each day.

That puts the storage ceiling about two weeks away — not three days.

Still, Iran pulling a 30-year-old crude carrier out of retirement shows the pressure is biting.

Source: X.com

On the Iranian side, the early decapitation strikes killed many of the (relatively) moderate figures.

The new cohort is fragmented across hardline factions, several of whom are profiting from the crisis. That makes a coherent negotiating position difficult.

Iran’s only real leverage now is to extend the blockade and inflict more pain on the global economy.

Sadly, Australia is in the crossfire more than most.

At the outset of this conflict, many Trump-aligned think pieces portrayed it as part of a broader strategy to corner China.

Now, more reports are coming out saying China is among the least affected.

Wood Mackenzie went so far as to call China the ‘out-and-out winner’.

I wouldn’t venture that far. But still, a deeper signal sits underneath all this. Markets are pricing a clean resolution. China is pricing many years of friction.

When the country sitting on the world’s largest crude stockpile refuses to draw on it during the worst oil shock in a generation, that’s a signal worth weighing.

Regards,

Charlie Ormond,

ATLAS and Altucher’s Investment Network Australia

Comments