All year we’ve heard about the crisis in energy and the acute effect it’s having on Europe.

But you wouldn’t know it walking around Spain, which is what I’ve just done for the last month.

And the war in Ukraine? That felt as distant to daily life there as it does here.

That’s not to say the issues aren’t real…only that, whatever happens, the world keeps turning.

One wonders, too, how much of this energy issue is built into prices.

If not 100%, it must be mighty close.

I’m back in Australia now.

For this reason, I’m turning my eyes north to China today. All the news is about the latest Communist Party shindig.

But here’s what I’m thinking about…

Have you noticed that the price of iron ore is still at more than US$95 a tonne?

That sticks out like the proverbial to me.

Here’s why…

For more than 12 months, Chinese property developers have been struck in a liquidity and solvency crisis as they deal with a stalled property market, defaulting loan payments, and protesting buyers.

All we ever hear about in Australia is how iron ore goes into steel, and most steel is used in Chinese construction, especially property.

Why, then, does iron ore remain so resilient?

Now, a cynic might say that it’s down from the giddy heights of US$200 a tonne it hit last year…

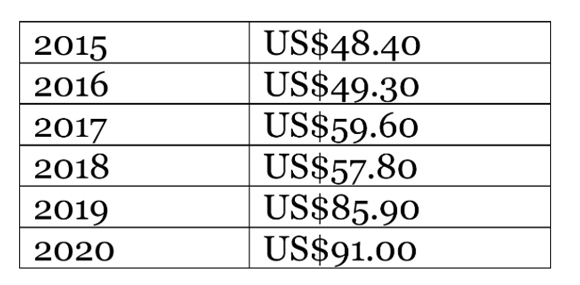

But here’s a table I put together last year of the average iron ore price back to 2015:

|

|

| Source: Fat Tail Investment Research |

Today’s price is still a boomer, relatively speaking.

And, again, consider the context that Chinese growth continually gets written down from COVID lockdowns, weak property sales, and the general global dog’s breakfast going on right now.

Something doesn’t quite square here. Either China’s growth is better than presumed, or iron ore is less available than presupposed.

Or perhaps China is stockpiling it, regardless of the fundamental economics of the market.

I can’t tell you what the answer is.

What I can say is that the current price continues to pour huge revenue through Australian miners and the Australian Government.

You need to follow the market a bit to see the significance of this price, too, in a different way.

Many analysts expect the iron ore price to fall back to US$60 a tonne. I’m sure a few of them would have thought it would be there by now.

Now, it’s perfectly possible iron ore will fall to US$60 a tonne. But what if it doesn’t?

Do you see the implication?

It will give the Aussie Government the fiscal firepower to offset the global contraction happening now with deficit spending.

It could also see BHP, Fortescue Metals, and Rio rally because too much negativity is currently built into their prices. They’ll still be generating huge cash flows at this price.

And goodness me, what if iron ore rallies?

Suffice it to say I take nothing for granted regarding the market. There is an awful lot of negativity built into the market now.

It only — well, maybe only — needs the news to become ‘less bad’ for a rally to happen.

And with so many looking for cues from interest rates and central banks, it might just be that it comes from something left of field…like a booming iron ore/China move.

Take that as the speculation it is. But the onus is on us to table different scenarios that are currently baked into people’s perceptions.

But, as above, it’s not as if energy, rates, and a slowing economy are now ‘fresh’ news.

The market will move well ahead before any recovery is apparent in mainstream headlines.

That might sound like wishful thinking, especially considering the weak market we’ll likely see today.

However, the market is designed to wrong-foot us most of the time. It’s too easy, and usually expensive, to go with the herd for too long.

Granted, nothing is clear about today’s market. It’s been one of the most difficult I can recall.

However, just as a unique cluster of factors drove the markets down, it may be a unique cluster that drives them back up.

Personally, since about September last year, I’ve advised my readers to exercise a lot of caution.

Now I’m comfortable suggesting becoming more aggressive because the risk versus reward equation — with a decent time frame in mind — is a lot better when individual stocks can be down 40% or more off their highs.

I’m putting my money where my mouth is too and buying for my SMSF (self-managed super fund).

Will I call the bottom? Nope. Will these stocks be in profit in, say, two years? The odds favour it, in my view.

I have a tonne of ideas to share on this theme. Stay tuned!

And speaking of new ideas, tomorrow night, I’m unveiling a new, AI-powered system designed to target stocks defying this downtrend and shooting higher. Check out all the details here if you’re interested.

Best wishes,

|

Callum Newman,

Editor, The Daily Reckoning Australia

Comments