A blocked AI deal in China.

Re-cut iron ore deal terms.

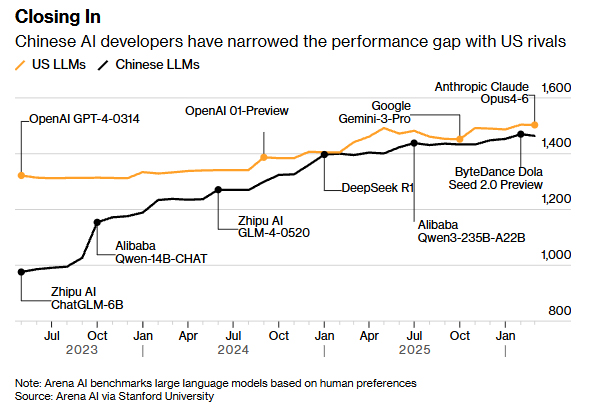

A chart that shows China’s AI nipping at the heels of Anthropic.

And it’s approaching midnight on China’s money clock…

This is the backdrop for the big face-to-face between the two head honchos.

Trump and his circle will be all too aware of that when the US president meets China’s Xi Jinping in the coming weeks.

Will it be a grand handshake for the ages?

A dud photo-op? Or somewhere in between?

China bull or bear?

My colleague Charlie Ormond and I were on a panel in Melbourne last week kicking around some of the ideas I’m going to share with you today.

And if you read his piece yesterday, you’ll know he’s generally bullish on Beijing’s ability to keep climbing the geopolitical ladder while Washington is distracted and overstretched.

Consider this…

The US has burned through close to half of some of its key missile stockpiles in the Iran war, including Patriot and THAAD interceptors, and it will take years, not months, to rebuild them.

Gee whiz those little headlines about defence procurement are important…

That buys China time.

But I’d argue it doesn’t buy them financial freedom.

China’s power – and its box

On the hard‑power side, China is playing a smart long game.

They’ve got oil stockpiles to the moon — it’s a great buffer.

It is also doubling down on the raw material base of power – solar, batteries, EVs, industrial robotics and the metals supply chains that feed them.

Yet on the financial side, the story is much weaker.

A lot of China’s AI surge is funded by state banks and local governments, not private capital, and forecasts show public money will carry most of the AI capex bill through to at least 2028.

So they need to play smarter and more efficiently.

Levers in a grand game

Look at AI.

Pound-for-pound, I agree with Charlie.

If this were boxing, China is a disciplined lower-weight-class type, throwing high-impact punches against a larger incumbent heavyweight champion.

It’s true, China gets more bang for its buck in the AI model-chip-compute war.

Despite chip sanctions and far smaller war chests, Chinese labs like DeepSeek, Zhipu and Alibaba’s Qwen have pushed models into the global top tier by making them leaner and more efficient.

So check this chart out…

Benchmarks now show Chinese large language models running close to, and in some cases matching, US leaders on headline performance:

Source: Bloomberg

The catch is that China’s best private players are still heavily dependent on subsidised power, state‑backed capital and political goodwill at home.

And then there’s this little nugget that shows you how sensitive things are:

Source: Bloomberg

Today’s move by Beijing to force Meta to unwind its US$2 billion acquisition of Manus — a Singapore‑based AI agent company with Chinese roots — shows how far Chinese regulators will go to keep “crown jewel” tech from drifting offshore.

This is a very bold grab back.

“Hands off that’s mine! Don’t go running away with that precious AI.”

Says China, ahead of the big meet and greet between Donald and Xi.

Chinese diplomacy ahead of the summit has one clear theme: create an image of stability and reasonableness while Washington looks distracted and exhausted by war.

So, China leans harder on the levers it does control — industrial policy and (increasingly) tech.

Master Confucius says…Don’t

embarrass them Donald

Here’s where Confucius comes in.

In the Confucian tradition, order, hierarchy and face — how you appear to the world and your peers — are not superficial ideas; they’re central to political legitimacy.

If Trump is clever, he will play straight into that.

Give Xi something that looks like a win and squeeze harder away from the cameras.

The AI and semiconductor space is the natural theatre for this kind of deal.

China wants relief on export controls and space to keep building out its AI stack.

For one simple reason — they’re under the pump financially.

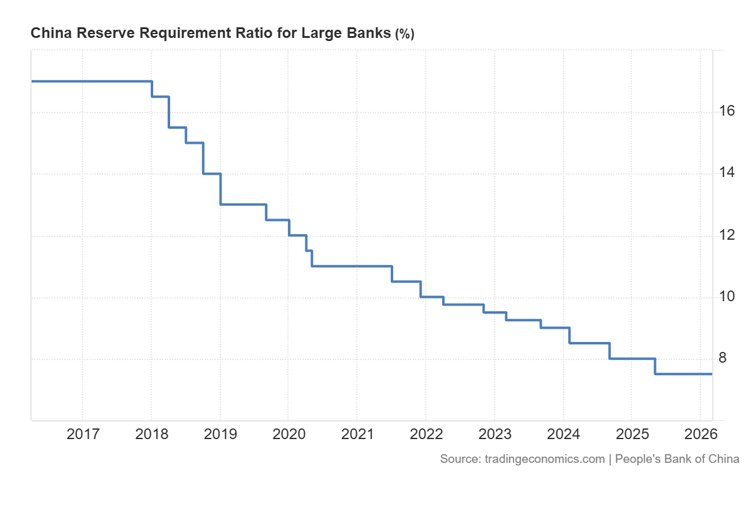

Ghost cities, stretched regional banks and less and less monetary stimulus available from the Reserve Requirement Ratio.

This is roughly speaking, the required cash on hand China’s big banks need to have (think “Tier 1 Capital Ratio”):

Source: Trading Economics

[Click to open in a new window]

It’s how China puts money in the system and, for me, is a good measure of how much monetary stimulus ammo the country has in the chamber.

And it doesn’t look great on the money front for China.

The weak hand on money

Under the surface, you can see why Beijing is so touchy about outbound deals like Manus.

When Chinese founders shift to Singapore or the US, associated IP, capital and senior talent migrate with them — plugging directly into Western markets and valuations.

That’s exactly where China is boxed in.

China’s domestic stock market remains volatile, and its digital‑currency experiments have not yet produced a true rival to the dollar system.

So the regime falls back on what it can scale fast — factories, data centres, and hard‑asset projects along the Belt and Road.

Why this all loops back to the ASX

For an Australian investor, here’s the important bit.

If the big contest is US finance and IP versus Chinese factories and resources, Australia sits uncomfortably — and profitably — in the middle.

China cannot keep its AI‑and‑infrastructure push going without iron ore and high‑grade metallurgical coal.

Those factories underpin Chinese solvency, which is where the success of their AI push ultimately rests.

Recent reports of Beijing trying to re‑cut pricing and volume arrangements with majors like BHP are a reminder that its fiscal health is STILL structurally linked to keeping that ore tap open:

Source: Australian Financial Review

At the same time, Washington has finally woken up to how exposed it is on critical minerals.

US policy now explicitly targets alternative supply of lithium, copper and rare earths, and a growing chunk of that future tonnage is expected to come from Australian projects, or Aussie‑led ventures offshore.

That makes the ASX a kind of fulcrum between two gyrating powers.

On one side sit the big, cash‑gushing iron ore houses that Beijing needs to keep solvent.

On the other, a rising wave of smaller lithium, copper, nickel and rare‑earth developers that sit neatly in Washington’s “China‑proof the supply chain” playbook.

So how do you position?

For now, I’d call it a cautious bull market.

At least as far as the top end of the market goes.

But I’m seeing strong rotation over the last month of trading into ASX small-cap developers and DFS-stage mining projects.

Neither power can run the global supremacy play without rocks in the ground.

Those rocks are on the ASX.

They lie in the rich dirt of this country — and increasingly in projects Aussie geologists are picking up in Africa and the Americas.

If Trump and Xi walk out of their summit smiling, the market will focus on tech headlines and AI models.

If they walk out scowling, it will focus on tariffs and sanctions.

In both cases, the world still needs what Australia digs up.

Your job, as I see it, is to understand that the real negotiation table for this new cold war runs straight through the ASX. Then own the smartest, most adventurous teams finding and expanding those deposits.

This is the crux of the major multi-year investment thesis I present here.

Warm regards,

Lachlann Tierney,

Australian Small-Cap Investigator and Fat Tail Microcaps

Comments