I’m back today, but only just.

If you didn’t hear, many in our team were struck with a hard-hitting influenza strain over the weekend. Worst I’ve had in a while.

Not fun, a good reminder that good health is everything.

Anyway, I’m going to try and shake my flu-ridden head into writing something that’s (hopefully) worth your time.

Luckily, I wrote part of today’s piece last week.

So here goes….

As you might know, focusing on out-of-favour and undervalued commodities has been a decent strategy in recent years.

The most recent examples have been oil, gas and coal.

Before that, platinum and silver.

If you added those metals to your portfolio at any point over the last 12 months, then you’ve probably done well.

Find a commodity that’s been in a bear market, sit on a few stocks linked to that theme and wait for the inevitable revaluation.

Sounds simple, right?

In hindsight, yes. But as you’ll recall, in 2025, the oil market was dead. It took a brave investor to put capital into this unloved sector.

But as I was saying back then, oil’s rise sat as a very real possibility. Given the commodity cycle’s ability to float all boats. It just needed a spark to create price momentum.

We’ve certainly seen that now.

But it’s nothing new. This time last year, it was Chinese trade embargoes on critical minerals that created a surge in rare-earth stocks.

The year before that, it was central bankers in emerging economies that shifted out of U.S. dollars and into precious metals. That sparked gold’s momentum.

If you still hold onto the idea that this sequence of events is just a coincidence, you’re missing the bigger picture.

These events are playing out just as we’d expect, following the same script as cycles prior.

But understanding that there is a commodity cycle is one thing. Putting that into real investment outcomes is quite another.

For my paid readership group, O&G companies have been our #1 focus over the last 6 months.

And these stocks have done exactly what we asked of them: hedged against geopolitical risk.

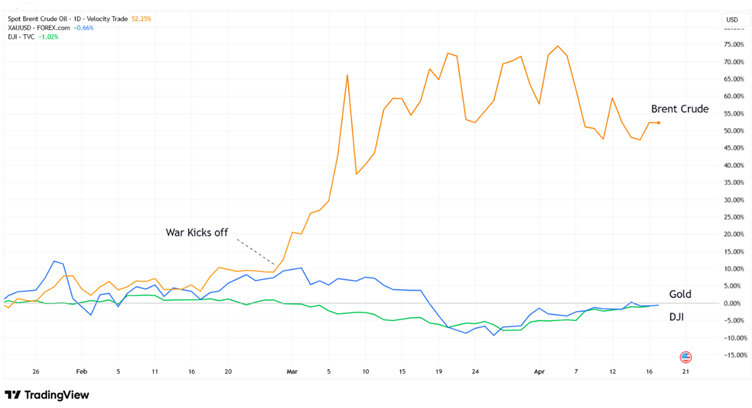

Forget gold or bonds, oil is where today’s true portfolio protection lies, as you can see below:

[Click to open in a new window]

Of course, gold did have a massive run-up over the last two years. But oil didn’t. So, it’s a simple methodology, really.

Bottom line: If we hold the idea that the commodity cycle floats all boats (eventually), then what ‘value-focussed’ commodity should you look at next?

One Option to Consider: Nickel

Like oil 6 months ago, the nickel market has been roiling in a deep bear market over the last two to three years.

Surging output from Indonesia’s nickel laterite mines has flooded the market with new supply.

In response, Australia’s nickel mines shut up shop. It was the same across Europe and Canada.

Andrew Forrest’s Wyloo Metals closed the door on its nickel acquisition in Kambalda, Western Australia. A project formerly owned by Mincor Resources.

BHP’s Nickel West operations did the same.

The global response to oversupply was predictable and unanimous. Operations across the West shifted into care and maintenance.

But as is always the case in commodity markets, over time, that will take supply off the table.

And slowly, but surely, the setup in nickel has been building…

Indonesia’s Stranglehold on Nickel Supply

Indonesia’s dominance of nickel supply is a structural crisis in the making for this key industrial commodity.

You see, concentrating supply into a single region makes the sector less responsive to rising demand. It also exposes the nickel market to sudden production cuts and geopolitical risk.

As mines close abroad, the country has free rein to cut back its own supply and dictate prices.

And we may be seeing early signs that it’s starting to use its leverage in the nickel market…

Earlier this year, the Indonesian government forced key domestic players, such as PT Weda Bay Nickel, to cut output quotas by up to 71%.

Double that up with potential sulphur supply shortages, a critical input for nickel hydrometallurgical processing, and the nickel supply glut could revert quickly.

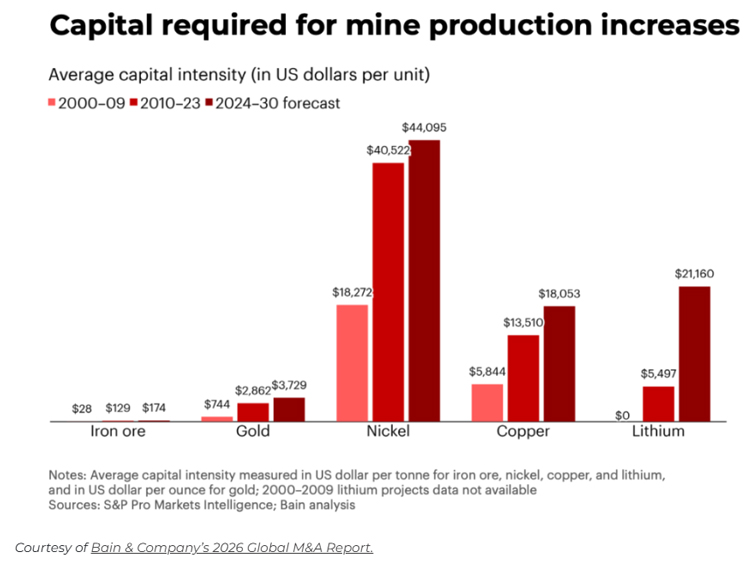

Another problem: the capital required to mine and process nickel is among the highest for any metal.

For nickel, the average unit cost to boost output (beyond current supply) is about $40,000. In terms of copper its only $13,000:

[Click to open in a new window]

Bottom line: developing nickel mines is capital-intensive.

That’s been obscured in recent years by heavily subsidised Chinese investment into Indonesian mines, flooding global nickel markets.

Slowly, the dynamic in the nickel market is turning.

Put it on your watchlist, nickel stocks could emerge from the dust this year, just as traditional energy has in recent weeks.

Until next time.

Regards,

James Cooper,

Mining: Phase One and Diggers and Drillers

Comments