Every large technology company is now selling investors the same story. Spend enormous sums on AI today, and the profits will follow tomorrow.

Margins will widen, AI-led productivity will climb, and the golden era of fat cashflow that defined Big Tech will return.

It’s a hopeful pitch, and it has carried share prices a long way. It’s also looking shakier with each passing quarter.

The four biggest US hyperscalers plan to spend close to US$700 billion on capital projects this year, up roughly 77% on 2025.

Almost all of that increase goes into data centres, chips and power for AI. The strain is already visible, with Amazon’s free cashflow expected to turn negative in 2026.

But Amazon isn’t alone. Since 2022, the overall trend in the S&P 500 has been that shareholder distributions (in green below) have given way to expanding capex (in black).

Source: BCA Research

[Click to open in a new window]

Seemingly, that capex expansion is all for a purpose. A push into an incredible new technology that promises to solve our productivity crisis. I’m partially sold.

You see, much of the bull case rests on a simple idea about costs. Swap expensive staff for cheaper machines, and margins improve. Plenty of firms have already started down that path, trimming headcount in the name of efficiency and AI adoption.

That logic only works if the machines are genuinely cheap. At the moment, they’re not, because the companies selling AI are selling it well below what it costs them to provide.

Sold at a Loss

The two leading American labs, Anthropic and OpenAI, are not yet profitable.

Industry reports suggest a developer paying US$200 a month for a coding tool can consume around US$5,000 worth of computing power.

OpenAI is widely thought to lose money on its consumer subscriptions as well.

The wider business looks just as fragile. Of OpenAI’s more than 900 million weekly users, only about 5% pay anything.

Revenue has to be coaxed out of a base that has grown used to getting the product for nothing.

This is why both labs are now steering customers towards metered pricing, charging by usage rather than a flat monthly fee. The cheap introductory phase is quietly being wound down.

The pattern should be familiar to any investor. A product is handed out below cost to build a user base and a habit.

Once the dependence is there, the price climbs. AI firms are running that playbook at a scale rarely seen before.

When the Bill Comes Due

For now, private capital is happily funding these losses. That arrangement has a natural endpoint. Because at some stage, these companies meet public markets and the discipline that comes with them.

OpenAI shows the tension clearly. It filed confidentially for a US listing at a valuation of around US$1 trillion.

However, the latest reports suggest it may push that debut back to 2027, with Sam Altman refusing to accept anything below the trillion-dollar figure.

Whenever the listing arrives, the incentives shift. Public shareholders generally prefer profit to open-ended cash burn, and the pressure to lift prices will build quickly.

That’s where the trouble spreads to the rest of the economy.

Higher AI bills would land on companies that have already cut staff to make room for the technology. Having let the workers go, they would be tied to a tool that suddenly costs a great deal more.

Such a squeeze would arrive late in an economic cycle, with many balance sheets already stretched.

A productivity gain bought on the promise of cheap AI could curdle into a fresh cost shock instead.

Echoes of the Dot-Com

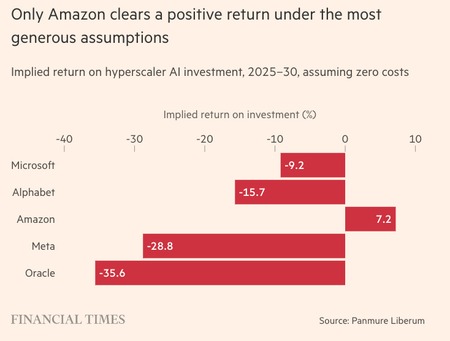

The returns on all this spending already look thin. On the Financial Times’ own figures, even under best-case assumptions, the picture is unflattering.

Source: FT

[Click to open in a new window]

The comparison that keeps returning is the dot-com era. Remarkable technology does not automatically produce sustainable economics.

The internet survived and reshaped the world, yet most of the internet companies of that period did not.

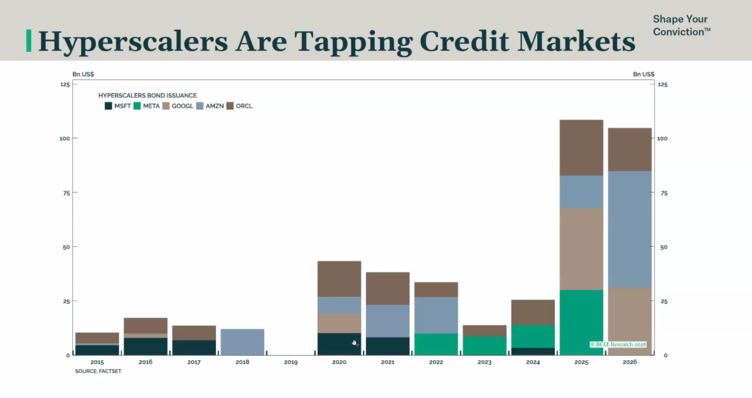

The funding structure adds to the unease. In some estimates, spending now runs at around 86% of revenue at Oracle, 54% at Meta and 47% at Microsoft.

To cover the gap, the group has leaned on credit markets for more than US$100 billion in 2025, and is ready to push past that in the second half of this year.

Source: BCA Research

[Click to open in a new window]

There is also a catch to the obvious escape route of higher AI prices. If the labs raise prices to chase profit, cheaper open-weight models from China stand ready to undercut them.

Either margins stay thin, or higher prices invite a flood of low-cost substitutes.

For Australian readers, none of this is a distant problem. These same names sit at the top of most global index funds and inside a large slice of your superannuation.

Local data centre exposure through stocks such as NextDC and Goodman Group rides the very same trade. I would suggest sticking to the ‘shovel plays’ further down the pecking order such as commodities.

The buildout may still pay off in time, since the technology is real and the demand could yet catch up.

But the hyperscalers are spending trillions on the hope that it does. That’s not certainty. It is a leveraged bet, and one that deserves closer scrutiny than today’s share prices imply.

For those who lack the discipline or time to scan the markets in this environment, I can offer one possible solution.

My latest AI-assisted trading system ATLAS was made for exactly this choppy trading environment. With over 2,000 stocks on the ASX, it’s impossible for one person to scan every chart, every sector, or rotation.

ATLAS can offer a clean, simple interface so you can reap the rewards as the AI continuously scans the market for new opportunities. Next week, we’re unveiling a series of new updates to the system, which will provide even deeper scanning of markets.

And for the end of the financial year, we’re offering a 50% off deal for the next 12-months.

This also applies to existing members who want to get a discount next year.

We rarely do these offers, so it’s a good time for you to capitalise on it by EOFY, where you also may be able to get a tax deduction (speak to your accountant to confirm).

If you have any queries/wish to do it over the phone you can contact our Melbourne-based customer service directly on 1300 667 481.

Regards,

Charlie Ormond,

ATLAS and Altucher’s Investment Network Australia

Comments