Erratum: We got our charts mixed up the other day. No problem: we’re sure you figured it out.

Our story so far…

Presidential candidate, Robert F Kennedy Jr wanted to know what we thought.

‘Go back and read our daily messages for the last 25 years’, we might have said.

‘And don’t miss our five books; you need to read those too.’

Instead, we prepared an ‘executive summary’. In Part I, we explained how the post-1971 dollar was cut loose from the real world of time and resources. Its gold-backing was removed. This allowed the financial economy to race ahead of the real economy of goods and services.

Money is just a way of keeping track of who owes what to whom, like tickets in a parking garage. ‘Financialisation’ is what happens when you add tickets; you go to get your car and find that someone else has driven away in it. It meant that a lot of people thought they had ‘wealth’ that didn’t really exist. Their stocks weren’t worth as much as they hoped. Their houses were overpriced. Their pensions were underfunded. Their government deficits piled up…waiting for a day of reckoning. Our chart showed GDP output practically flat, while ‘assets’ increased 10 times.

So, let us pick up our letter to RFK Jr (we promised fewer than 1,000 words…alas, we ran over), where we left off:

Dear Robert,

The second major change to the financial system occurred in the late ’80s when Alan Greenspan gave out his famous ‘Greenspan Put’. Investors then knew that the game was rigged — in their favour. When they made money, they pocketed the gains. When they lost money, the losses were shared out — by lowering interest rates and inflating the currency — to the general population.

This was dramatically demonstrated in 2001–04, 2007–16, and again in 2019–22. Each time, the ‘market’ tried to reduce asset prices and debt, and the Fed stepped in with cheaper credit (and more debt). Remarkably, the Fed’s key lending rate remained under the inflation rate for the whole period 2008–23 to today (excepting a few months in 2019).

In other words, instead of allowing the economy to correct mistakes and excesses, the Fed made them worse. It drove down interest rates, claiming — perhaps believing — that it was ‘stimulating’ the economy. Between 1999 and 2023, the Fed added some US$8 trillion in new money. The federal government added some US$28 trillion in deficits. This should have been more than enough ‘stimulus’ — enough to wake a dead man.

But if there is a success story, in which real growth was stimulated by fake money lent out at fake interest rates, it is absent from the historical record. Every instance of excessive money-printing — from ancient Rome in the time of Diocletian…to Zimbabwe, Venezuela, and Argentina in our own time — shows the real fruit of ‘stimulus’ is bitter…even fatal. It leads to poverty and discontent, not prosperity.

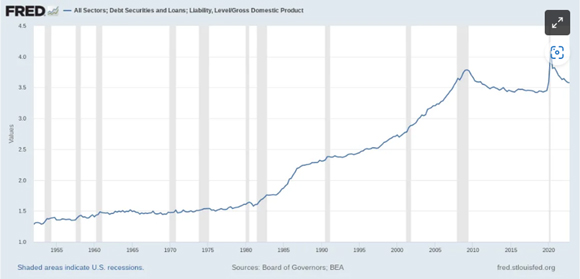

Here’s Chart #3. It shows what happens when you leave interest rates way too low for way too long. You get a lot of debt:

|

|

| Source: US Federal Reserve |

Cause, meet effect

Absurdly low interest rates enticed people to borrow. Debt grew proportionally. Federal debt is now 86 times higher than it was in 1971. Credit card debt nears US$1 trillion. Student loans have surpassed US$1.7 trillion. Total US debt is more than US$90 trillion. The federal government already owes US$32 trillion and expects more US$1 trillion deficits ‘as far as the eye can see’.

The effect of these two policy changes — the ‘flexible’ post-1971 dollar…and ultra-low interest rates — was exhilarating to the rich. But devastating to everyone else. A family in the top 1% now has 680 times as much wealth as one in the bottom 50%.

Trillions of dollars’ worth of easy money created an unnatural hot-house environment. People got used to 4% mortgages. Businesses got used to rolling over their debt at a 3% interest rate. The federal government got used to borrowing at a negative real rate on its 10-year bonds. And speculators got used to ‘negative carry’. At one point, they borrowed at the Fed’s low rates, then lent the money back to the government (by buying US Treasury bonds). The transaction was economically sterile and fruitless. But it was profitable. And the Fed’s ‘forward guidance’ removed the risk of a sudden shift in policy. But now, like a dense jungle canopy, exorbitant debt shades and stifles the eco-system beneath it.

Then, in July 2020, the credit cycle hit bottom (the lowest yields in 500 years). Interest rates began to rise. And today, 10-year Treasury bond yields are five times higher than they were just two years ago. The correction that the Fed has postponed for more than three decades is upon us. The traditional, dreaded feedback loop has reasserted itself; the Fed can no longer stimulate the economy, not without causing consumer prices to rise.

Inflate or die

None of this would have happened without the bumbling intervention of the Fed. Market-set interest rates would have risen a long time ago. Higher rates would have halted the build-up of debt, flattened the bubble in asset prices, and encouraged real capital formation.

In a better world, the Fed would be disbanded. After all, the idea that a group of greying lawyers and economists can set interest rates for a US$24 trillion economy is pure fantasy. Neither theory nor experience supports it.

As it is, the Fed faces a grim choice. Inflate or Die. Either it backs off and allows the bubble economy to die…with a crash on Wall Street, recession, bankruptcies, unemployment, and all of the other nasty things needed to correct its own policy mistakes. Or it protects the gains of the rich and the powerful by continuing to inflate the economy.

The inflation option postpones the reckoning…but it increases the pain. And it destroys the middle class. The poor get inflation-adjusted handouts. The rich have their assets, their hedges, and their hustles. But the middle classes sell their time by the hour. Prices go up. Real wages go down. Jobs disappear. And houses, where the middle classes keep their savings, become debt traps. As prices rise, families borrow heavily to buy them. Then, they must refinance…at higher and higher rates.

An honest democracy cannot exist without a strong, independent middle class. The poor are easily distracted with circuses and bribed with bread. The rich may still call themselves ‘capitalists’, but they become ‘crony capitalists’…manipulating the masses and the financial system to extract as much fast, easy cash as possible.

So, it is not just the financial system that is in danger. It’s the whole kit and kaboodle of US society. Money affects everything.

Our guess is that when the going gets tough the deciders will choose the worst option — inflation. Politically, it is the smoother road…for a while.

But maybe you can be the decider who will change that.

Good luck,

|

Bill Bonner,

For The Daily Reckoning Australia