I know I’ve banged this drum before. I’ve written many times about the demand for energy infrastructure and the commodities that go into them.

But I’m once again back on my podium. First, I want to do a quick retrospective.

I went back and looked at my ASX-focused energy article called ‘Wiring the Future’ that specifically called out several ASX stocks in this space.

That was October last year. So, how have they done?

The stocks mentioned were all core to the Australian grid infrastructure theme. Since October those stocks are:

- IDP Group [ASX:IPG] up +52%

- GenusPlus Group [ASX:GNP] up +51%

- APA Group [ASX:APA] up +20%

- Ventia Services Group [ASX:VNT] up 16%

Source: TradingView

[Click to open in a new window]

Ok, so we can all pat ourselves on the back for the right call occasionally. But that isn’t what this is about.

This is about underscoring the quiet growth in this sector while everything else has been drowning it out.

Now the big noise in markets is inflation.

But what’s needed in this energy-led inflation moment?

More energy. Bigger grids. And the commodities to build them.

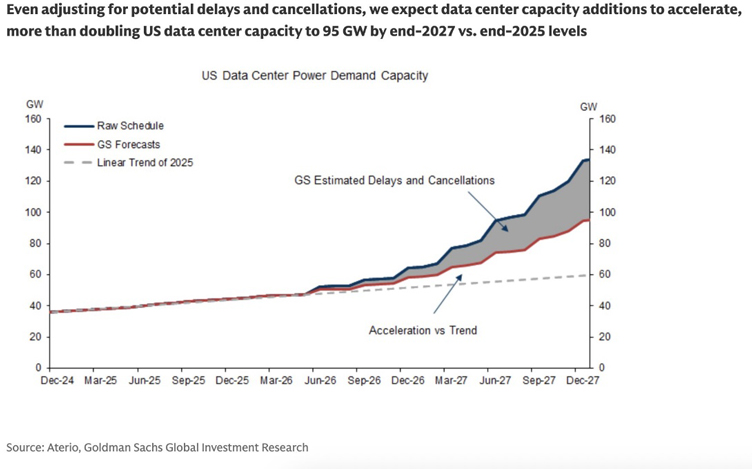

Turning to the US, Goldman Sachs recently updated its energy demand estimates for the States.

They estimate that things are accelerating. From their outlook:

‘We expect US data center power demand to increase from 31 GW in 2025 to 41/66 GW in 2026/27 assuming a capacity utilization rate of 70%.

By 2027, we expect data centers to account for 8.5% of total US power demand.’

Source: Goldman Sachs Global Investment

[Click to open in a new window]

The subtext here is that — even with all the growth we’re seeing — a mammoth buildout is still needed between now and the end of the decade.

That’s a major theme to follow. And if that wasn’t enough, the US government is now stepping in to push it along.

A Defense Production Act for the Grid

On 22 April, Trump invoked Section 303 of the Defense Production Act of 1950 to designate grid infrastructure essential to national defence.

The order names:

- Transformers

- Transmission lines and conductors

- Substations

- High-voltage circuit breakers

- Power control electronics

- Protective relay systems and capacitor banks

And electrical core steel as ‘nation critical industrial resources’.

This move authorises direct purchases, multi-year commitments and financial support for new production capacity by the US government.

A similar decree was given to large-scale power infrastructure.

These are the same statutes that covered ventilators during the pandemic and lithium processing in 2022.

What it signals is that the federal government is prepared to underwrite the supply chain rather than wait for the market.

A new order from the Office of Electricity called SPARK is one example of this.

An acronym that deliberately includes ‘Speed to Power’, the data-centre industry’s catch phrase for connecting new load ahead of competitors.

The numbers behind the policy push are not small.

With AI compute capex from the hyperscalers running into the high hundreds of billions per year, the policy response is being sized to that.

An ASX Perspective

The relevant point for our markets is that the major inputs to the American grid are produced overwhelmingly outside the United States.

And three commodities anchor this new build cycle.

Copper is the primary conductor in transformers, substations and high-voltage cabling.

Each gigawatt of new transmission consumes thousands of tonnes of the refined metal.

ASX exposure runs through some of our largest and strongest names in this current market.

Next on the list is Uranium. Nuclear power is re-emerging as a politically acceptable answer to baseload power for AI compute.

Many have their hopes tied to Small Modular Reactors as the pathway to demand. Even without these, the supply story is heading towards a deficit.

That’s supported by Trump’s executive orders last year, which committed the United States to quadrupling nuclear capacity by 2050.

The major Aussie listings are well known, with a longer tail of smaller developers behind them.

Considering the long-term trends in uranium prices, this also looks like a solid bet in upgrading future grids. Here’s the spot price for uranium since 2023:

Source: TradingView

[Click to open in a new window]

Lithium sits less obviously inside the grid narrative. But battery storage is still the cheapest way to firm renewables and shave peak load while transmission builds catch up.

Yes, gas is going strong, but the infrastructure is now facing backlogs. Some, like gas turbines, have wait times over 5 years.

So lithium is going to remain in play for the foreseeable future.

Australia has some of the largest lithium reserves globally and a suite of top-tier miners making hay while spodumene prices remain high.

And while the lithium trend has run hard this year, there are still pockets worth your time.

My colleague Lachlann Tierney has been tracking this trend since the beginning. He’s currently putting an updated report together on what he sees ahead for the sector.

And what he sees is opportunity.

So that’s three major commodities at the centre of the ASX you should consider.

Whether it’s AI or governments pushing the grid, the need for these resources is a major theme in the years ahead.

More power to you.

Regards,

Charlie Ormond,

ATLAS and Altucher’s Investment Network Australia

Comments