On Friday, January 30, 2026, global precious metals markets experienced one of their most dramatic sell-offs in decades.

Gold prices went from setting all-time new highs earlier in the week to suffering one of their biggest one-day percentage drops ever recorded.

Silver posted its steepest single-session decline since 1980.

The shock resonated through the bones of precious metal investors as they watched, in horror, billions of dollars wiped off the valuation of metals and mining stocks.

Few appreciate how voluminous this move was, in part because gold and silver had already posted significant gains in the weeks prior.

But in many ways, January 30, 2026, was the black Friday for precious metal markets and a day that will go down in investor folklore.

However, January 30 did not mark the bottom of the gold correction…

That came several weeks later, as war suddenly erupted in Iran, putting an end to the unchecked speculation in the precious metals market.

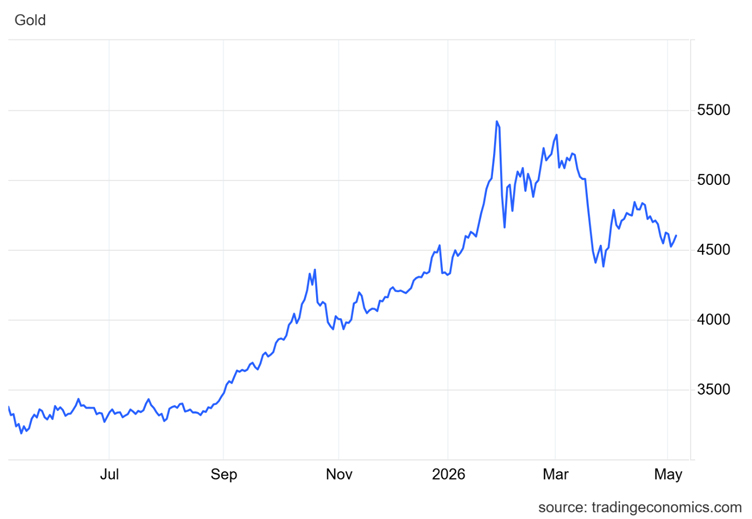

The March bottom and war sell-off would mark the ultimate low in the precious metals market, with gold briefly dipping below $4,500 per ounce.

Gold’s line in the sand has been observed.

So, will it hold?

Earlier in the year, the fear of missing out progressed rapidly into the fear of not being able to cash out.

A miner from the early 1900s would have felt right at home in the wild precious metals markets of 2026.

Unrestrained volatility is a hallmark of this market, rooted in some of the world’s most infamous gold rushes, such as the Klondike Gold Rush of the late 1890s.

Yet, since those March lows, conditions in the precious metals market have stabilised… Trading volumes have dropped, and daily price fluctuations have moderated.

Thankfully, for those long-term investors, gold is gradually returning to its traditional role as a portfolio ballast. Gold’s inertia has equilibrated.

And today, it’s arguably in a much stronger position versus the hyperbolic pre-war phase, when gold traded as high as US$5,400–$5,500 per ounce.

The war in Iran served an important purpose; chiefly, it shook out the weaker hands in this market, thanks to a testy 20% freefall in the spot price over March.

Today, gold trades within a tight range and is showing every sign of consolidating above this important March low:

[Click to open in a new window]

From a technical perspective, gold is holding firm, displaying resilience after its first major test in its current secular bull market.

Again, that should be a point of optimism for gold investors, buoyed by the fact that unsustainable speculation has truly departed.

The geopolitical asset

But in terms of gold’s role as a geopolitical hedge, it has failed in its role miserably…

Various excuses have been presented on behalf of gold, such as the need for liquidity and the fact that gold was an easy choice given that investors were sitting on strong paper profits.

Perhaps. But I don’t buy it. Gold’s role as a geopolitical hedge has always been murky; war is not gold’s stated purpose.

Some historical takeaways: The Yom Kippur War of the 1970s…

Back then, gold surged almost 35% in the 3 months following the conflict’s kick-off. And it then swelled by almost 70% 12 months after the war.

Clearly, that’s strong correlative evidence of gold’s safe-haven status? The Yom Kippur War has often been cited as a reason to own gold.

The same could be said for gold’s stellar performance following the 2003 Iraq War… That catalysed a major gold rally, with gold rising 12% over the 12 months following the start of that conflict.

But was it war that supported higher gold prices, or was it the backdrop that underpinned strong commodity prices throughout the 1970s and early 2000s?

Well, to answer that, we could turn to another conflict in the Middle East, one that didn’t coincide with a decade of strong commodity price inflation… Say, the Gulf War of 1990.

In that instance, gold prices remained dull, 3 months out from the war. And they remained flat 6 months out, and 12 months after the conflict began:

Source: Trading View/Perplexity

[Click to open in a new window]

In other words, when gold wasn’t in a commodity price inflation era, war had little impact on pushing prices higher.

Gold’s role as a safe-haven asset clearly has some cracks… And the evidence was there well before the war in Iran.

The 1970s were a decade marked by higher gold prices, and the Yom Kippur War was just one of many factors that supported this investment class.

Bottom line: don’t put too much weight on what’s happening in Iran and the future trajectory of gold prices. Keep them separate.

And weigh gold against its real barometer…

Like this one: Governments are divided on a lot of issues, but destroying the collective value of their currencies isn’t one of them.

Sovereign debt, reckless fiscal spending, falling tax receipts, and unchecked war budgets; all these issues will be offset by their weakening currencies.

And it’s why gold remains a ‘buy-the-dip’ asset class.

And that’s why you should get a hold of the ‘gold investors bible,’ a book written by my colleague and friend, Brian Chu.

A bloke who has spent the better part of a decade analysing and obsessing over the gold market and the stocks within it.

He’s truly put his life’s work into this book, and it’s well worth securing a copy, reading it and locking it up alongside your bullion so that you can pass it on to future generations.

Make sure you secure your copy here.

Until next time.

Regards,

James Cooper,

Mining: Phase One and Diggers and Drillers

Comments