You might be looking at BHP’s lofty share price today of ~$55 and wonder, ‘did I miss the boat?’

Fear not.

I’m convinced there’s still plenty of time to invest in quality mining companies.

Just look at what’s happening in mining deals right now.

Global mining and metals M&A is off to the strongest start in years, with more than US$20 billion of deals announced already in 2026.

The total value of these deals is already running about a third higher than at the same point in 2025.

A lot of that money is chasing gold, copper and critical minerals, and private equity has suddenly muscled in to take more than 20% of total deal value after being almost nowhere last year.

There’s a great way to conceptualise all of this, which I shared with readers of Australian Small-Cap Investigator a couple of weeks back.

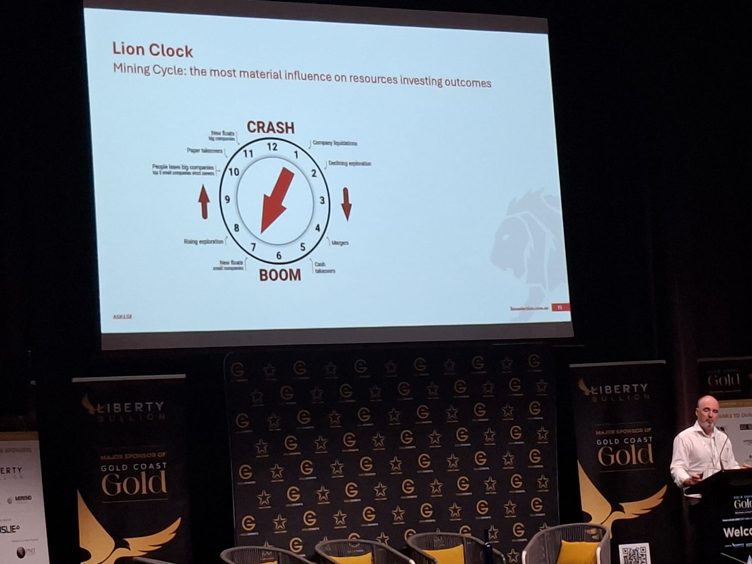

We’re at about 7 o’clock

Listed funds manager Lion Selection Group [ASX:LSX] uses this clock diagram to represent the predictable nature of the mining cycle:

Source: Lion Quarterly

[Click to open in a new window]

At 1 o’clock, prices are depressed, and capex dries up, meaning no one wants to fund unprofitable mines.

Slowly, though, that capex drought leads to decreased supply as demand ramps.

Prices start to rise, and investment comes back in…

So, where are we on Lion Selection Group’s mining cycle clock?

They reckon we’re at about 7 o’clock right now – I got that straight from the horse’s mouth when I went to a gold conference on the Gold Coast a month and a half ago:

Source: Lachlann Tierney

[Click to open in a new window]

And on their framework, the real frenzy in deals comes in the late‑boom zone.

That is when big miners, flush with cash and emboldened by high prices, start paying silly prices for marginal assets.

If you look at this cycle, I don’t think we are there yet.

Yes, deals are lifting.

But the pattern is different to the old blow‑off tops where management teams chased any old project and then had to write off the assets a few years later.

This time, the drivers sit mostly outside the boardroom.

You have the energy transition, data centres, defence and re‑shoring all pulling hard on the same set of metals.

Things like copper, nickel, lithium, rare earths, and uranium.

Even old‑world steel inputs (coal, iron ore) are back in focus as governments talk about ports, rail, transmission lines and onshoring basic industry.

There are simply too many demands feeding into the same supply pit, which has been starved of proper capex for roughly 10–15 years.

That’s why this wave of M&A

isn’t a “top‑of‑cycle” moment.

If anything, it is a sign the majors are waking up late to how tight the system is and how much real capital spending will be needed to loosen it.

Remember what central banks actually need if they want to cut rates and keep them down.

They need inflation in the real‑world “thing economy” to cool.

Food, power, rent, and manufactured goods.

The only honest way to do that over time is to bring more supply online.

And that runs straight through mining.

More ore, more processing, more logistics, more competition.

Which means we will need a long period of elevated capex around the world, not a quick sugar hit.

New projects, expansions and restarts across multiple commodities and jurisdictions.

Australia should be a prime

beneficiary of that process.

Whatever the headlines say about the Iran war and risk‑off global moods, the ASX still lists some of the best‑run and best‑positioned miners on the planet.

From gold producers to copper developers to rare‑earths hopefuls, this is where global capital comes when it wants scale, rule of law and geological quality.

Just look at the proposed Vault Minerals [ASX:VAU] and Regis Resources [ASX:RRL] — two big gold miners deciding to get married to create a monster gold company.

This is indicative of the great window of opportunity still open for ASX investors.

Yes, there may be a financial crash due to private credit, war, pestilence…you name it.

But we’re not yet at the part of the mining cycle dial where corporate hubris usually peaks.

There’s simply too much demand across a range of commodities.

As a result, I think the best opportunities over the next year or two may not be the big, diversified mining companies doing the buying.

It is more likely to be the late‑stage developers, the near‑term producers, and the single‑asset companies that look deliciously bite‑sized to global predators.

These are the stocks that can re‑rate sharply as sentiment improves, feasibility studies firm up, and the market starts to price in either first production or a takeover bid.

I’m already seeing some of this capex and takeover speculation hit a range of companies across Australian Small-Cap Investigator and Fat Tail Micro-Caps.

This is only the beginning.

Warm regards,

Lachlann Tierney,

Australian Small-Cap Investigator and Fat Tail Microcaps

Comments