Tech corporation Megaport [ASX:MP1] has released its quarterly report with increase of 14% in Monthly Recurring Revenue (MRR), which had grown to the sound total of $14.1 million quarter-on-quarter.

Total revenue for the group had gone up 3% compared with the second quarter, the group expressing it will see its earnings reach above the general market consensus for both 2023 and 2024.

Shares for the tech stock were rocketing 46% by midday, boosting MP1’s stock price from $3.98 to $5.80 at the time of writing.

The boost today has upped the group’s stock price 43% in the past month, yet its still 8% down so far in the year:

Source: TradingView

Megaport achieves revenue gains in third quarter

On a busy morning for ASX-listed companies reporting quarterly results, this tech company was thrilling investors, with some clear uplift to results in the last quarter ending last month.

Over the third quarter of fiscal 2023, the company said it had achieved MRR growth of 14%, an increase of $1.7 million, to total $14.1 million in the March quarter.

Excluding impacts of foreign exchange on the weaker Australian dollar, underlying MRR grew $1.6 million, or 13%, largely thanks to Cloud VXC repricing.

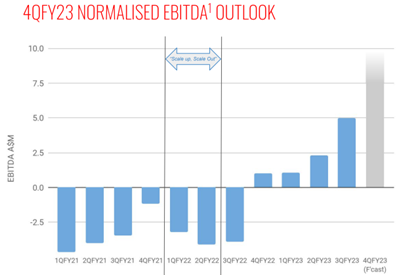

Megaport reported total revenue for the quarter of $38.1 million, a 3% incline from the pervious quarter and delivered EBITDA (earnings before interest tax, amortisation, and depreciation) of $7.2 million compared with the $2.4 million earned in Q2.

This result marks the fourth consecutive quarterly period Megaport has reported positive EBITDA.

Cash burn for the quarter churned though $8.9 million, with cash and bank balances at the end of the period of $48.6 million.

MP1 also added 607 new services, including 188 customer ports, 34 MCRs, and 25 MVEs in the last quarter, broadening its service range for higher income streams.

Source: MP1

Megaport declares earnings to rise above consensus

The tech group released a separate announcement pertaining to its EBITDA guidance for the remainder of the year FY23 and for FY24.

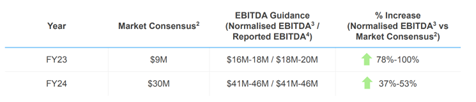

Megaport believes that as a result of various initiatives designed to improve the company’s operating, and financial performance and cash generation, it now expects Normalised EBITDA to be ‘materially above’ market consensus of $9 million (in FY23) and $30 million (in FY24).

The group now expects normalised EBITDA in FY23 in the range of $16 million to $18 million, and normalised EBITDA in FY24 in the range of $41 million to $46 million.

MP1 says that the recent improvements to financial performance and cashflow as well as the $48 million cash in bank gives the company confidence it will not need to raise any additional capital to operate, aside for any ‘strategic or opportunistic’ cases that may arise.

Source: MP1

Jim Rickards’ ‘Sold Out’ book offer — grab your copy now

Supermarket shelves are bare, with glaring random gaps in place of once readily available items.

Banks are permanently closing more and more branches across towns and suburbs.

Used car prices are rising, and sourcing new ones for speedy delivery is getting harder by the day.

Prices in general are skyrocketing while packaging is shrinking.

Is it all just inflation, COVID ramifications and market volatility, or is there more to the story?

Thing is, these are just some of the seemingly unrelated signs pointing to something bigger.

Mere ‘inconveniences’ are just the start.

Geopolitical expert Jim Rickards has been making very apt, on-point predictions for decades.

And now he’s predicting ensuing financial chaos. Yes, more so than there is right now.

He explains it all, offering a unique perspective that should not be ignored, in his book, SOLD OUT: How Broken Supply Chains, Surging Inflation, and Political Instability Will Sink the Global Economy.

You can grab a free copy when you sign up for The Daily Reckoning Australia, also free, right here.

Regards,

Mahlia Stewart,

For Money Morning