Greetings again from the belly of the beast.

(The United States)

Yesterday I promised more stories from the road, and America has already delivered.

The Yanks stand accused of rigging the World Cup.

Their star striker copped a one-match ban, then watched it get quietly overturned in time for the next game.

Belgium is playing them as I write this, and half of Europe is muttering about Trump manipulating the biggest sporting event in the world.

Honestly, the outrage is kind of misplaced.

America has been rigging a much bigger game for 80 years.

Ever since the Bretton Woods deal at the tail end of World War Two, the US Federal Reserve has effectively set the rules of global finance.

The dollar became the world’s reserve currency, and every central bank on earth has danced to the Fed’s tune since.

Which makes what’s happening right now at the US Fed all the more strange.

Referee just put the whistle away

New Fed chair Kevin Warsh has torn up the forward guidance playbook.

At his first press conference, he stripped the policy statement of any language hinting at where rates might head next.

He reckons markets work best when they respond to actual economic data, and he thinks traders waste far too much energy trying to reverse-engineer the Fed’s next move from carefully planted clues.

He even refused to submit his own “dot” in the Fed’s famous dot plot of rate forecasts.

Pressed for hints at the European Central Bank (ECB) forum last week, his answer was blunt: “No forward guidance, no forward guidance.”

So, the referee who has run the global financial game since 1944 just binned the whistle.

Markets are now expected to judge conditions for themselves.

Call me a crazy Yank, but this actually seems like a better system than the one we’ve become accustomed to.

So, if the Fed is now listening to the market rather than the other way round, what is the market telling us?

Have a look at the IPO pipeline.

America is building tall again

Check out this chart…

Source: Renaissance Capital

[Click to open in a new window]

US IPO proceeds have already hit US$114.7 billion in 2026, and we are barely into July.

That is closing in on the US$142.4 billion full-year record from the 2021 frenzy, and more than double last year’s US$44 billion.

Now look at the black line on that chart.

The number of actual deals is low.

A handful of monster floats are doing the heavy lifting. SpaceX pulled off the largest IPO in history last month, and Alphabet is raising US$85 billion to fund its AI buildout.

South Korea’s SK Hynix is next in the queue.

The world’s top supplier of high-bandwidth memory, the specialised chips that feed Nvidia’s AI processors, wants to raise about US$28 billion through a US listing.

Its Seoul-traded shares are up roughly 260% this year, pushing its market value past US$1 trillion.

The deal is already oversubscribed, and at this size it would rank alongside Saudi Aramco’s US$29.4 billion debut in 2019 as one of the biggest floats in history.

Trading starts on 10 July under the ticker SKHY.

The AI memory squeeze behind all this is very real.

Apple and Microsoft recently hiked prices on Macs, iPads and Xbox consoles within hours of each other, both blaming an unprecedented shortage of memory chips.

The skyscraper signal

Property investors know an old rule of thumb called the skyscraper index.

The world’s tallest buildings tend to open their doors right as the boom that funded them rolls over.

The Empire State Building opened during the Great Depression, the Petronas Towers went up around the 1997 Asian financial crisis, and the Burj Khalifa arrived just as Dubai’s property market imploded.

Record towers get built when money is cheap, confidence is soaring and everyone assumes the party runs forever.

IPO waves work the same way in the sharemarket.

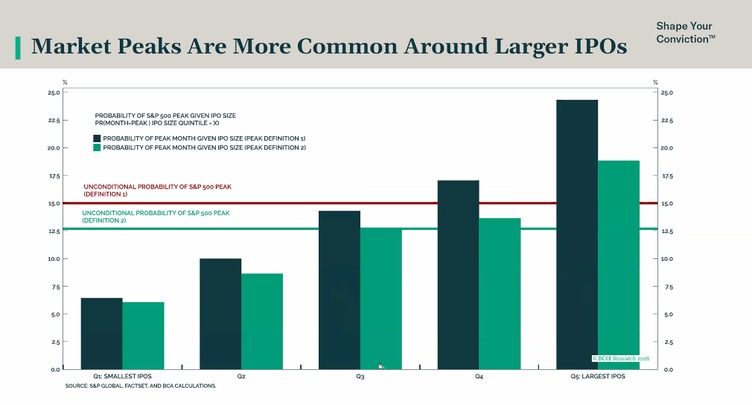

Academic research backs this up.

In 2003, two academics found that IPO waves cluster when share prices are high and expected future returns are low, which is exactly when private owners choose to sell to the public.

Source: BCA Research

[Click to open in a new window]

Think SpaceX IPO – this is potentially the exit liquidity where the big dogs exit into the poor saps that bought into the frenzy.

History agrees with the professors.

The dot-com float frenzy peaked alongside the Nasdaq in 2000, Blackstone listed within months of the 2007 credit market top.

Then in 2021, Coinbase and Rivian floated during the 2021 speculative surge that unravelled the following year.

To be clear, none of this means a crash lands next week.

Remember, IPO surges are like the tallest towers in the property cycle.

So always ask who is on the other side of the trade.

What about the ASX?

Our market looks positively sleepy.

Local float waves peaked around 2000, 2006–07, and 2021.

Right now, the ASX IPO calendar is subdued, and that may be no bad thing.

So keep one eye on the American skyline.

The referee has gone quiet, the mega-floats keep stacking up, and the towers keep getting taller.

By the time the tallest one tops out, the party is usually much closer to the end than anyone wants to admit.

By the way, look into the Jeddah tower in Saudi Arabia, which is due to be finished in 2028:

Source: Wikipedia

Something to consider if you are expecting the mega-cap, US-based AI gravy train to roll on, unimpeded for the next two years.

Food for thought indeed.

Warm regards,

Lachlann Tierney,

Australian Small-Cap Investigator and Fat Tail Microcaps

Comments