‘Late-cycle valuations. Mid-cycle growth. Early-cycle revisions. End-of-cycle politics.’

That line came from a US hedge fund manager this week.

It also captures the confusion facing anyone trying to read the pulse of the economy right now.

Because right now, the data depends entirely on where you look.

On one side, the commodity cycle is alive and well, supporting Aussie miners. Investors who moved early into miners are sitting comfortably.

On the other, it’s a very different story.

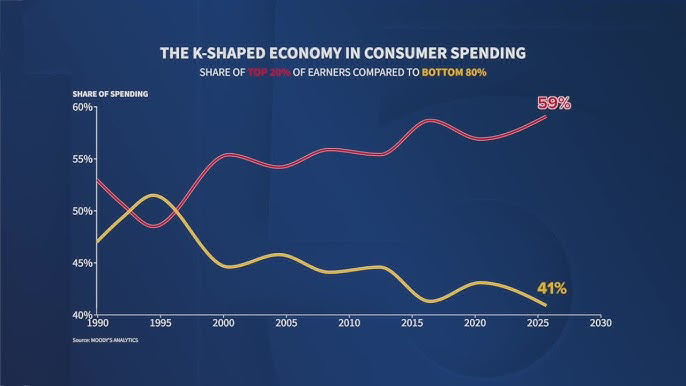

We’re living through a K-shaped economy, where the haves continue to spend, and the have-nots pull back.

We don’t have clean data for Australia. But in the US, the top 20% of earners now account for nearly 60% of all consumer spending.

Source: ABC15 | Moodys Analytics

[Click to open in a new window]

That’s an extraordinary concentration. It also explains why headline data can look fine while large parts of the population feel anything but.

The Vibecession Returns

In a similar vein, I’ve been tracking the revival of the phrase ‘vibecession’ online.

It’s the idea that consumer sentiment vibes are poor, despite relatively benign economic data.

Usually, that gap doesn’t really exist. Consumer sentiment tracked closely with hard data.

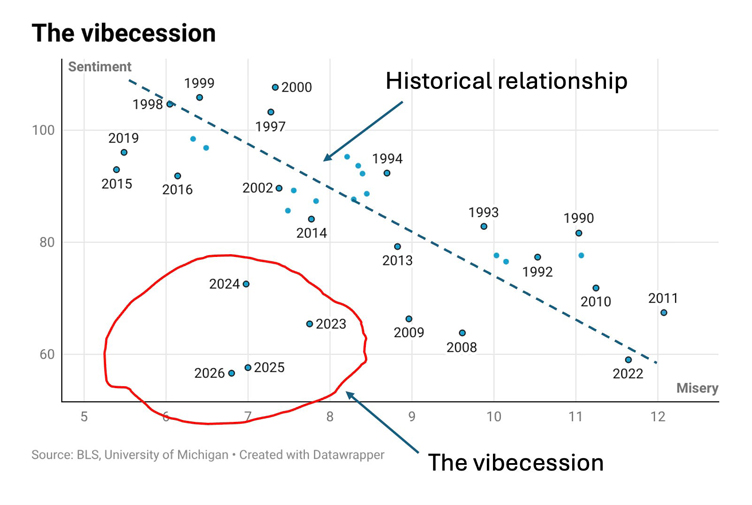

Historically, you could explain sentiment with one metric — the misery index (inflation + unemployment).

In a post-COVID world, that relationship has broken down. Here’s what consumer sentiment’s relationship with the misery index has looked like since 1990.

Source: Paul Krugman| Datawrapper

[Click to open in a new window]

You can already see that the first few months of 2026 show US consumer sentiment in new ominous territory.

But Americans aren’t alone. Across developed markets, sentiment has remained weak even as labour markets held up and growth avoided a formal recession.

And now, Australia has joined in.

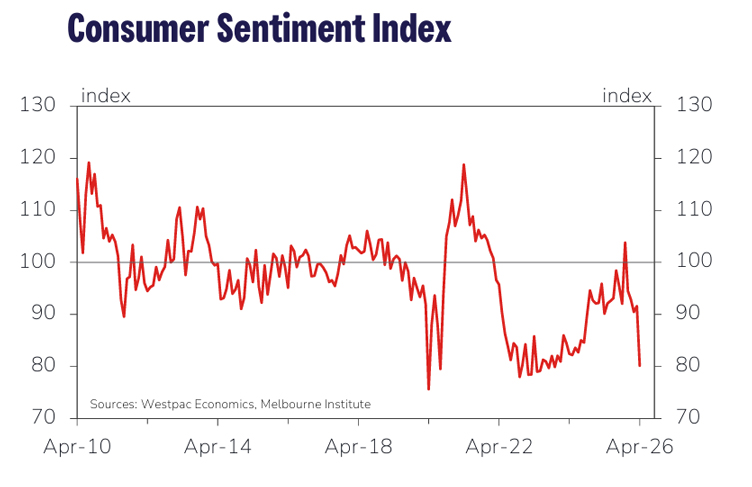

The Biggest Sentiment Fall Since COVID

The Westpac-Melbourne Institute Consumer Sentiment Index crashed 12.5% in April, to just 80.1.

That’s the sharpest monthly fall since the first COVID lockdowns.

At 80, the index sits near historical lows. It is still above the depths of the pandemic and the recessions of the 80s and 90s. But not by much.

Source: Westpac-MI Survey

[Click to open in a new window]

The trigger for this is hardly subtle. It stares at us from every servo.

Average pump prices hit $2.40 per litre in early April.

While prices have eased slightly — helped by a temporary halving of the fuel excise — the geopolitical backdrop hasn’t improved.

The Strait of Hormuz remains effectively constrained, and tensions continue to keep energy markets tight.

Banks and consumers now expect further hikes at the May meeting, with more to follow in the back half of the year.

Relief, in other words, looks distant.

What It Means for Investors

This leaves the RBA in a difficult position.

Inflation is still running above its targets. And at the same time, real per capita incomes are under pressure, and consumer demand is weakening.

That’s a tough combination.

For investors, it highlights the need to be an active investor.

A widening dispersion between the stocks that win and lose will leave ETFs underperforming.

Start with what to avoid.

When sentiment collapses this quickly, it rarely stays contained. The first cracks show up in discretionary spending.

Big-ticket retail is usually first in the firing line — electronics, furniture, homewares.

When households feel poorer, they delay these purchases.

Our big retailers tend to see earnings downgrades in the subsequent quarters. Margins get squeezed, inventory builds, and pricing power disappears.

The same caution extends to housing-linked exposure. As rate expectations rise and price expectations fall, activity slows.

That feeds through to developers, building materials, and anything leveraged to transaction volumes rather than long-term structural demand.

Remember, you’re effectively dealing with an RBA-led slowdown. But this isn’t a blanket risk-off environment.

It’s a rotation.

On the other side sit the beneficiaries of the same forces driving the pain.

Energy remains the most obvious. Huge geopolitical risk and constrained supply continue to support energy prices.

For LNG exporters like Woodside and Santos, that translates directly into earnings resilience, even as domestic consumers feel the squeeze.

It’s an uncomfortable dynamic, but an important one.

Beyond energy, the focus shifts to pricing power and necessity.

Companies that sell essentials, or hold market sway (think big supermarkets), tend to hold margins far better in this environment.

They don’t rely on consumer confidence to the same extent. Demand may soften, but it won’t disappear.

Likewise, exporters and globally exposed businesses offer some insulation. Their revenue streams are less tied to the Australian consumer and more leveraged to external demand or currency dynamics.

In other words, the playbook shifts from ‘growth-at-any-price’ to ‘resilience-at-a-reasonable-price’.

Low debt and solid balance sheets matter more. Cash flow matters more. And exposure to the marginal Australian consumer matters a lot less.

That’s the key takeaway.

The vibecession isn’t just about how people feel, it’s about where the pressure shows up next.

And right now, it’s pointing in a fairly clear direction.

Avoid where confidence matters most.

Focus where it doesn’t.

Regards,

Charlie Ormond,

ATLAS and Altucher’s Investment Network Australia

Comments