Narendra Modi touched down in Melbourne last night to a red-carpet welcome. Tonight, he’ll be the guest of honour at a sold-out Marvel Stadium as business leaders cheer India’s Prime Minister.

It’s the usual circus when Modi comes to town. His unique style of ‘Hindutva,’ what we’d call ethno-nationalism in the West, has a familiar political ring in this moment.

But the main event happens earlier, behind closed doors. Modi and Albanese are expected to sign a commercial uranium supply agreement today.

It would end twelve years of frustration for one of Australia’s most maligned sectors.

Twelve Years of Paperwork

Australia and India signed a nuclear co-operation pact back in 2014. It was controversial at the time, as India never signed the nuclear non-proliferation treaty.

That pact promised uranium exports for peaceful use. In practice, almost nothing shipped. Technical and regulatory barriers on the Indian side have kept the trade stuck near zero for over a decade.

Those safeguards have now been reworked, clearing the path for serious volumes.

India’s ambitions here are enormous. The country wants to lift nuclear capacity from around 8 gigawatts today to 100 gigawatts by 2047. Its state nuclear operator plans 18 new reactors by 2032, and private companies are also sniffing the opportunity.

Part of this is about weaning off coal. Ninety-six of the top 100 most polluted cities by air quality are in India. The other four are all in neighbouring countries.

The single biggest contributor is open fires, but coal-burning byproducts (especially sulphur dioxide) are the primary force multipliers to this problem.

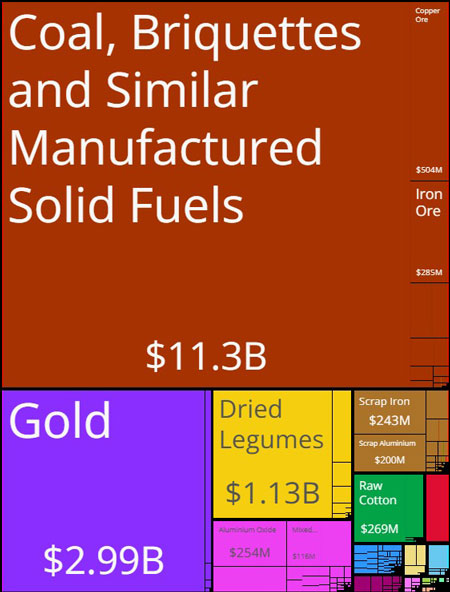

And we’re their second largest supplier of coal after Indonesia.

Exports from Australia to India

Source: Observatory of Economic Complexity

So, times are slowly changing. The latest driver of change is data centres.

Google, Meta and Amazon are pouring billions into Indian facilities to serve the world’s most populous nation, and all that computing requires a steady baseload of power.

India’s High Commissioner said earlier this year that the country would take as much uranium as Canada’s Cameco could produce. That’s the mood of the buyer here.

The Sleeping Supplier

Australia sits on almost one-third of the world’s known uranium reserves, the largest share of any country. Yet we rank just fourth in production.

Part of the reason is political. Mining the metal is banned in every state except SA and NT. That leaves a limited list of local producers who often suffer from higher regulatory costs.

The sector has been out of favour since the 2023–24 bull market faded. Share prices have continued to fade this year since their short-lived spike in January.

Source: TradingView

[Click to open in a new window]

But a committed Indian buyer could change the maths on this sleepy sector.

Early Move or Dead on Arrival

Before anyone gets carried away, remember what this sector does to believers.

Uranium was one of the hottest trades in ‘23. Then the spot price slid from around US$100 per pound to US$64 lows.

Short sellers feasted on the wreckage. At one point, uranium companies filled six of the twenty most shorted spots on the ASX.

Today, the spot price is drifting sideways, and Lotus Resources remains the second-most shorted stock on the ASX, at ~23% shorted.

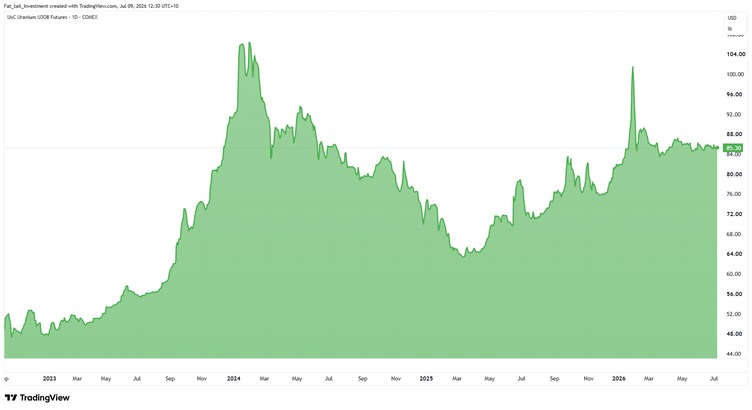

Uranium Futures: 2023–Present

Source: TradingView

[Click to open in a new window]

It’s worth mentioning that spot is often the wrong thing to watch in this slow-moving sector.

Utilities hold between one and two years of inventory, so they can sit out for long stretches. So demand always shows up later than the bulls expect.

But overall, things are decidedly boring. In my opinion, that’s the time when you want to be laying your bets.

The long-term structural case never went anywhere. Analysts see global demand reaching 230 million pounds a year by 2030, against mine supply closer to 205 million.

Deep Yellow’s founder puts the unfilled supply gap at two billion pounds by 2042. That number sounds great, but it’s a bit like asking a barber if you need a haircut.

Still, the tape has started to lean the same way. Spot prices are slowly grinding higher since the 2025 lows.

The long-term contract price, where utilities actually transact, hit US$95 in June, its highest in more than 18 years.

Shorts remain heavy across some of our major names. But that positioning can also force giant reversals. If Indian demand proves real, crowded bearish bets could unwind violently.

Nobody rings a bell at the turn, and this could yet prove another false start. Often previous rallies have leaned on demand forecasts over supply shortfalls.

A supply deal signed directly with these companies is firmer ground for them to regain the ASX’s good graces.

And a signed agreement will not move pounds overnight. Contracts must be negotiated, mines expanded and shipments scheduled.

But in a market this tight, direction matters more than speed.

The Great Race

Our resident geologist, James Cooper, has been ahead of this shift for a while now. He called the surge across commodities before the mainstream caught on, from oil and gold through to uranium and rare earths.

James argues none of these moves are random. He sees them as pieces of a single accelerating event he calls The Great Race. A fracturing world order, a scramble for resources, and a rush to re-arm.

In his view, this race is pulling markets into a new regime. Deals like the one Modi signs this week are a small preview of what that looks like.

James has put together a full presentation on The Great Race and how Australian investors can position for it.

Regards,

Charlie Ormond,

ATLAS and Altucher’s Investment Network Australia

Comments