The last couple of weeks have been ugly.

Gold dropped sharply, silver even harder, and the “AI disruption” favourites over in tech land finally cracked and pulled down the big indices.

And with them, small-caps and micro-caps were forced lower.

On your screen it looks like one trade breaking.

In reality, I think it was the market adjusting to a new version of the same story.

On the tech side, big software names were hit because their old edge was suddenly exposed.

For years they lived off centralised access to data and big teams of coders.

Now smaller outfits can plug cheap, powerful code‑generation into niche data sets and spin up products fast.

That was the market repricing competition risk in the incumbents, not killing the AI theme.

On the commodity side, the Warsh Fed chatter gave traders the excuse they needed to dump leveraged paper exposure to gold and silver after a huge run.

It was a classic deleveraging and profit‑taking event in precious metals, not some grand verdict on whether we still need “stuff” in the real world.

And we absolutely do.

AI needs real stuff

The basic thesis has not changed.

AI lives in hardware, power and wires.

Every new wave of AI capability needs more hyperscale data centres, more servers, more cooling, and a lot more electricity to keep it all on.

That means:

- More substations and transmission lines.

- More grid‑scale batteries and storage systems.

- More copper, uranium, gas, lithium, nickel and assorted metals to build it all.

You cannot talk about “AI everywhere” and then pretend we can coast on the same old energy system.

The big tech firms know this.

Microsoft has been inking multi‑gigawatt clean‑energy deals to feed its cloud and AI data centres.

Amazon has been signing massive renewable and battery contracts and working directly with utilities to lock in power for its server farms.

In simple terms, tech companies are quietly turning into power buyers of last resort.

Once they sign those long‑dated power deals, the energy developers on the other side have to go and find the fuel.

That is where the commodities come in.

And here’s the investable output…

If you are an energy company with access to a big undeveloped resource, this moment matters.

Because suddenly you are not just some “option on the cycle”.

You are a potential solution to a binding AI power problem.

The first assets to benefit I think are likely in the energy resource space.

We have already seen a version of this in one of the uranium developers in my Fat Tail Micro‑Caps service, where interest stepped up once it became clear that nuclear is back in the conversation for baseload and AI‑driven demand.

A US energy company offtake appeared out of the blue…in Namibia?

Yep.

I expect more of this.

Because now the AI-commodities connection is pointing straight at energy resource developers.

They sit in that awkward phase where the story is real, but the cash flows are still in the future.

Which brings us to a tool I keep coming back to.

A Lassonde moment?

I saw Lassonde speak in Toronto two years ago.

Here’s a grainy picture with my signature terrible photo composition to prove it:

Source: Lachlann Tierney

The room was PACKED.

And he had some thoughts on AI and commodities which remain very relevant.

I’ll discuss those tomorrow.

The Lassonde Curve shows how a typical resource stock trades as it moves from discovery, to studies, to funding, to production.

You normally think of resource companies in terms of company news.

Drill hits.

Scoping studies.

Feasibility work.

Funding deals.

But now there is a big external driver influencing how the curve plays out.

The AI build‑out, and the power and metals it needs, are giving certain industries and individual companies a macro tailwind.

Developers with serious energy or critical‑mineral assets can suddenly line up offtake deals, strategic investors and financing because someone, somewhere, has promised a tech giant a decade of power.

That is where I think this recent sell‑off is quietly setting up opportunity.

Not at the glossy end of AI software as it exists in the world of Big Tech, but down in the dirt where energy and metals are pulled out of the ground.

Tomorrow I will share more on how I am using that Lassonde Curve view to target energy resource developers that could be next in line.

Warm regards,

Lachlann Tierney,

Australian Small-Cap Investigator and Fat Tail Microcaps

***

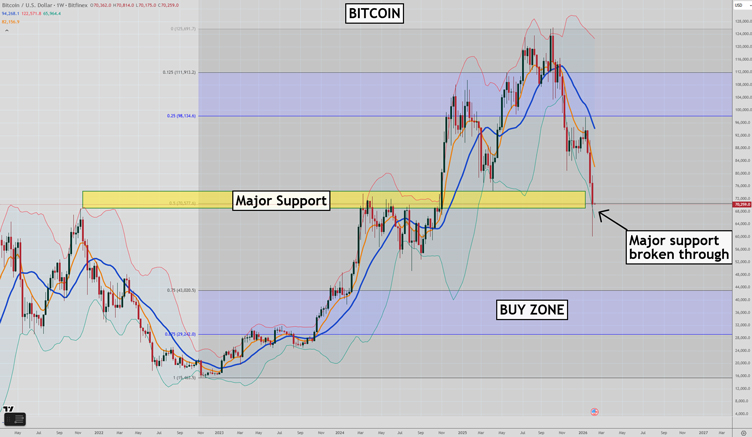

Murray’s Chart of the Day – Bitcoin

Source: TradingView

Despite the welcome bounce in bitcoin on Friday evening from extremely oversold levels, risks remain that more downside is coming.

We saw a major failure below the US$70,000-75,000 level last week.

It has changed the situation for bitcoin, with the uptrend since 2022 potentially finished, and a false break of the 2021 high confirmed.

Unless there is a dramatic recovery in the price and the weekly trend turns up, I will remain bearish on bitcoin.

This correction could see the price fall into the buy zone of the previous uptrend between US$29,000-43,000.

There should be plenty of resistance around US$80,000-88,000 while this downtrend remains.

Regards,

Murray Dawes,

Retirement Trader, International Stock Trader and

Murray’s Trading Room

Comments