What brilliant economic doctrine determined (somewhere in and around) 2% was the appropriate rate of inflation?

Was it devised by…Keynes? Minsky? Friedman? Schumpeter?

No. None of the above.

It was…a Kiwi politician.

During the 1980s, memory of the highly inflationary 1970s was still fresh in people’s minds. Was the inflation beast really tamed or would it go rogue again?

In 1988, NZ Finance Minister Roger Douglas (he of ‘Rogernomics’ fame) was asked in a TV interview about the appropriate level of inflation.

Roger Douglas made this off-the-cuff comment…‘[I am] aiming for inflation of around zero to 1 percent’.

The comment was not one of guidance, but of reassurance.

Don’t fret, the days of high inflation are behind us.

There was no economic science or formula to support Roger’s stated aim…the percentages were genuinely plucked out of the air.

The New York Times tells the rest of the story:

‘[In 1989] with Mr. Douglas’s figures as a starting point, Mr. Brash [NZ Reserve Bank Governor] and Mr. Caygill [the newly appointed NZ Finance Minister], agreed that it would be best to expand the range to give them more room to maneuver, but only a bit. New Zealand would aim for inflation between zero and 2 percent.

‘Not surprisingly, the passage of a law to reform the central bank governance of an archipelago of 3.4 million people received no coverage in the major American papers. But across the close-knit world of global central bankers, people started to notice the Kiwis’ monetary policy experiment.’

What was experimental is now enshrined

All major central banks have adopted the completely arbitrary 2% as the inflation target:

|

|

| Source: RBA |

And the big dog of central banks ask:

|

|

| Source: US Federal Reserve |

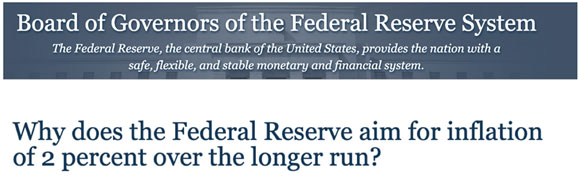

To which it answers (emphasis added):

‘The Federal Open Market Committee (FOMC) judges that inflation of 2 percent over the longer run, as measured by the annual change in the price index for personal consumption expenditures, is most consistent with the Federal Reserve’s mandate for maximum employment and price stability.’

The randomly selected 2% is the Holy Grail our (clueless) inflation warriors so covet…and slavishly pursue.

Belief in this target is now so absolute, no one in the economics profession or financial industry asks the question ‘why do we have this target?’.

Even though there isn’t a shred of evidence to support its existence, society has come to accept the target as gospel.

If people were asked ‘which of the following household budget items would you like to pay more for next year and indefinitely…electricity, fuel, food, education, alcohol, housing, etc.?’…

How many would agree to voluntarily paying more?

My guess…none.

Oh, but the rising cost of living is offset by CPI wage increases.

Hmmm…dog chasing tail comes to mind.

Costs go up 2%.

Wages go up 2% BEFORE tax.

In net terms, wouldn’t it be better to have ZERO CPI and ZERO wage growth?

Unfortunately, this far better outcome fails to satisfy one very important policy agenda…it doesn’t create the illusion of growth.

Ignorance enabled the Fed

Universal acceptance (or ignorance) of this mythical target is what enabled the Fed (and other major central banks) to not only begin, but doggedly persist with the most batsh*t crazy stimulus strategy in history.

The Fed was legislated into existence in 1913.

Over the next 95 years (to 2008), US money supply (M2) grew to US$7.5 trillion.

In the space of just 14 short years (2008 to 2022), M2 did not just double…it tripled.

M2 now totals US$22 trillion.

After 2008, the Fed’s foot remained on the interest rate throat for seven long years…then the foot was lifted slightly…until COVID. Then the Fed’s foot was slammed down hard again.

Savers choked and borrowers went for broke:

|

|

| Source: Federal Reserve Economic Data |

This reckless and completely unhinged strategy was done all in the name of achieving…2 percent…as measured by the annual change in the price index for personal consumption expenditures [PCE].

What did yield starvation, excessive money printing, outright market manipulation, and liberating society’s inner speculative spirit actually achieve?

The use of all this financial energy got the Fed close to (but not in excess of) the desired 2% annual change in personal consumption expenditures:

|

|

| Source: Federal Reserve Economic Data |

This bloody-minded commitment to hitting an imaginary target, combined with an equally bloody-minded commitment to rid the world of low cost and reliable energy, unleashed inflationary forces not seen for more than four decades.

Yes, COVID did disrupt supply chains.

However, overly generous fiscal and monetary policy responses put in motion an unexpected and unnecessary level of demand.

Too much money was chasing too few goods.

This blinkered approach to hitting a mythical 2% inflation target meant central banks ignored the far wider picture…the speculative bubbles, the demonisation of fossil fuels filtering through to higher commodity prices, the ballooning of private and public sector debt, and the artificial creation of demand.

The Fed’s extraordinary and unprecedented efforts (using QE and interest rates) to create a sustainable, ‘healthy’, and totally meaningless 2% inflation rate failed miserably.

Which brings us to the here and now.

What on Earth makes anyone think the Fed (or any other central bank), using basically the same tools (QT and interest rates), has a ‘snowball in Hell’s chance’ of engineering a ‘soft landing’?

Central bankers are reckless

These serial bubble blowers have proven beyond a shadow of doubt they are to economics what Charles Ponzi was to value investing.

Given their inability to see anything beyond the imagined 2% target, they’re likely to go too far in the opposite direction…raising rates beyond the level needed to curb consumer buying behaviour.

Plucking a target out of thin air, on its own, is silly enough.

But to then do all in your considerable power — irrespective of how nonsensical and reckless the policies of free money and plenty of it might be — to achieve this made-up objective, qualifies as certifiably insane.

This madness is accepted (by most) as responsible economic management.

Sadly, it’s going to take a whole lot of economic and financial pain before the penny drops with the public. Central bankers are pompous, incompetent morons…and that’s being oh-so polite.

This damning commentary applies to the whole central bank cohort.

Crises in every corner of the world

Europe. China. Japan. Britain. The US.

Each one is struggling with one or more crises…energy, debt, food, housing, and/or currency.

The idiotic pursuit of a target, manufactured into existence to serve a political purpose — to soothe public concerns — has put us between a rock and a hard place.

There are no good outcomes from here.

After decades of mismanagement, central bankers have run out of easy fixes.

Pushing the cost of debt servicing higher is going to make an already bad situation a whole lot worse.

And, if they don’t push interest rates up, they’ll risk a repeat of the 1970s…persistently high inflation.

5% inflation begets a 5% pay rise, which begets another higher CPI reading.

And the dog keeps chasing its tail.

Expecting those who created this problem to have the solution is most definitely a case of hope triumphing over our lived experience.

Central bankers ARE academic blowhards whose theories have proven time and again to produce bad outcomes.

How many more bubbles need to be blown and blown up to have this statement of fact recognised?

As always, the market WILL, in the fullness of time, provide the solution.

Folks, the party is over

Anyone expecting the next decade to be anything like the last one is going to be severely disappointed.

Just as the 1930s was nothing like the 1920s, the remainder of the 2020s is going to be the polar opposite of the 2010s.

DO NOT be conned by the central banks’ words of assurance.

The same neatly calibrated economic models that prompted Bernanke to say ‘subprime will be contained’ are now indicating a soft landing ahead.

What a joke.

Central banks have no idea how this is going to play out in the world outside their academic bubble. Market forces are highly unpredictable and when harnessed, extremely powerful.

Look at the recent win/loss record…

Dotcom bubble: Markets — One, Central Banks — Zero

US housing bubble: Markets — One, Central Banks — Zero

The everything bubble?

Are you willing to bet your financial future backing a different outcome this time around?

Regards,

|

Vern Gowdie,

Editor, The Daily Reckoning Australia