Markets are expected to start weaker this week after a red-hot inflation figure from the US on Friday.

A key report from the Commerce Department showed consumer prices rose by 0.6% from December to January.

It was the highest pace since June, but it wasn’t what markets were hoping for.

It now seems likely central banks will keep their foot on the pedal and increase interest rates again over the next few months.

Indeed, the bond market has already reacted savagely to the report.

The 10-year US Treasury note hit 3.96%, and the shorter-term two-year bond is sitting at 4.78%.

To put this in context, a year ago, this was at 1.54%.

Some now estimate the terminal rate — that is the maximum interest rate we’ll see in the US — could hit as high as 5.5% or even 6%.

This would be the highest level since 2001.

It took a while to get here, but the consensus in markets has now shifted from ‘pivot imminent’ to ‘higher for longer’.

But is that actually feasible?

Look, I highly doubt it…

A sustainable ‘risk-free’ return north of 5% for investors would see billions of dollars exit riskier assets, like stocks and property, and cause markets to go into freefall.

Millions of projects, investments, and developments would be mothballed based on lower present value calculations.

Heck, the US couldn’t even pay the interest bill on its own debt if we had high interest rates for too long.

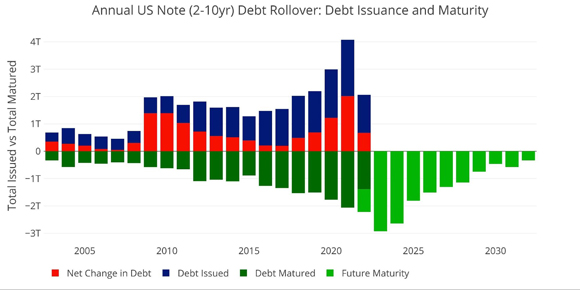

As you can see below, there’s a heap of US government debt due to be refinanced in the next two years:

|

|

| Source: SchiffGold |

So ‘higher for longer’ really would be shooting themselves in the foot.

I mean, would you put interest rates up on your own mortgage if you had the chance not to?

Despite what happens over the next few months, I just can’t see interest rates staying high for too long.

But here’s the thing…

In the ongoing battle against inflation, central bankers need us all to believe they will.

They need people to act like it’s going to happen — to pull back on spending and hopefully get inflation down — without them having to go as hard as they’re saying.

In short, it’s all just psychology!

And there’s actually a bit of economic game theory at play.

It’s a real-life version of the classic Prisoner’s Dilemma…with all of us as the prisoners!

Let me explain what I mean by this, and how it suggests we could be setting up for a big opportunity down the track…

Prisoner’s Dilemma for investors

The Prisoner’s Dilemma is a famous economic thought experiment where two criminals are captured by the police.

They’re each interrogated in separate cells and given a choice.

They each can either stay silent (and hope their mate does too).

Or they can dob in their mate and get a lighter sentence.

The payoff matrix looks like this:

|

|

| Source: Wikipedia |

The possible outcomes are:

- A: If A and B each betray the other, they each serve five years in prison.

- B: If A betrays B but B remains silent, A will be set free while B serves 10 years in prison.

- C: If A remains silent but B betrays A, A will serve 10 years in prison and B will be set free.

- D: If A and B both remain silent, they will each serve the lesser charge of two years in prison.

I’ll let you work through the various connotations here…

But the weird conclusion is, the rational thing to do is to betray your partner. Even though if you’d both kept schtum, you’d get the best total outcome (least combined sentence).

How does this relate to markets right now?

Well, as I said before, central bankers want people, businesses, and investors to act like they’re going to go hard on interest rates.

So we’ve all got a choice to make in response.

Believe them and act accordingly.

Or ignore them and act like they won’t go through on their threats.

The basic point I’m making is that everyone’s actions in aggregate effect the eventual outcome.

If we all call their bluff, we probably all lose as we make them increase rates.

But if only a few of us do, we benefit greatly at the expense of those who did ‘what the Fed wanted’.

I think we’re entering that window of opportunity soon.

After a bullish start to 2023, the ‘pivot soon’ crowd is about to be outnumbered by the ‘higher-for-longer’ one.

If that’s the case, markets could fall sharply.

But there’s a broader effect to that narrative setting in.

Pessimism will perpetuate through the system as a whole.

And it won’t just be investors that decide to sell out of stocks.

Some businesses will decide to sack staff and consumers will cut back on their spending. This then leads to more economic problems down the road.

Over the next six months, I fully expect earnings downgrades and more layoffs as people start to tighten their belts.

But here’s the interesting thing…

Make your plans now

The sooner this happens, the sooner future interest rate rises will probably start to come off the table.

And if things get too bad, we might even get interest rate cuts later in 2023, sooner than most people think.

So, that could be a good opportunity to buy ‘the dip’.

If we get one.

What I’m saying here, I suppose, is that there’s a rational reason for individual investors to ‘cheat’ — at some point anyway — and try to look for buying opportunities when everyone is still fearful and selling.

Because when everyone believes the ‘higher-for-longer’ narrative and acts accordingly, the probability of it happening actually falls.

I think timing that moment — the moment the crowd completely gives up on fighting the Fed — is going to be key for investors in 2023.

You can afford to be a bit patient as it’s likely we’re not quite there yet.

But you can’t just wait for general sentiment to improve or central banks to change their messaging before you act.

You’ll miss the boat if you do that.

In short, I think a classic contrarian set-up is coming soon.

The only dilemma is timing it…

Good investing,

|

Ryan Dinse,

Editor, Money Morning