Historically, properties that have attracted the most capital growth through the cycle are houses.

By that, I mean houses on suburban, sub-dividable blocks of land in the middle ring suburbs of the bigger cities. Areas that are attracting population growth into well-facilitated suburbs with limited supply.

I have mentioned this many times in Cycles, Trends & Forecasts when educating investors on what and where to buy, but there’s also a report that evidences it.

I’ll briefly run through the findings because it will assist your knowledge.

The report is produced each quarter by CoreLogic and is called the ‘Pain and Gain’ report.

The ‘Pain and Gain’ report looks at all the resales of established properties over each quarter and records details of those sold for a profit (‘Gain’) and those sold at a loss (‘Pain’).

(Just in case there is confusion, a loss is where the vendor sells for less than the purchase price. It doesn’t consider stamp duty, etc.)

The analysis breaks down the ‘Pain and Gain’ in capital city markets, investor versus owner occupier resales, regional markets, and capital city council regions — so it’s well worth a read.

In doing so, it marks the separation between units and houses.

A house is a property that sits on its own block with no shared land.

A unit is any property that sits on a strata title.

A strata title is where the title holders own a shared claim to common land that multiple properties sit on.

So units in this report are not just apartments.

They also include different property types, such as villas and townhouses. Any property type that shares common land.

In a moment, I’ll share the findings with you — but note that in each report to date, the sales that consistently record the greatest profit Australia-wide are houses, not units.

The reason is simple and underpinned by the first golden rule of real estate investing.

- It’s land (its zoning and location) that appreciates — not buildings.

Buildings depreciate.

To gain the best growth, maximise the proportion of your budget spent on the land component of the investment over the building component.

Of course, there’s a lot more to successful property investing, but understanding this basic rule underpins the rest.

Note that our biggest buying demographic in Australia is families with children (or those planning on having children).

They drive demand into the suburban house/land sector.

But additionally, the high volume of unit development that took place between 2013–16 in the first half of the cycle significantly diluted unit prices over time.

Not just apartments, but also townhouses and villas.

If you live in Melbourne, Sydney, or Brisbane in particular, you would likely have witnessed it yourself over recent years.

Many suburban blocks of land are being increasingly subdivided into 2, 3, 4, and 5 — often after being rezoned for higher-density development.

Unbroken blocks of land — around 5–600sqm and more — diminishing in supply as the cycle turned.

These blocks still fall under high demand from our biggest buyer demographic and likely also an increasing number of developers as the industry recovers from its difficulties over the last few years.

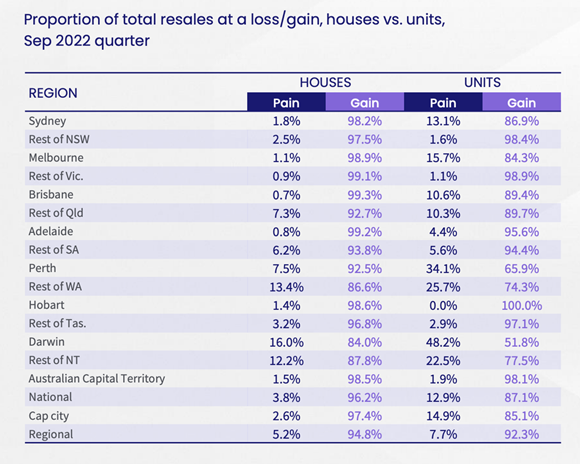

The most recent ‘Pain and Gain’ report evidences it.

As an overview, the report analysed around 83,000 property resales in the September 2022 quarter.

93.3% of resales made a nominal gain in the three months to May (down from a recent high of 94.2%).

The combined profit from resale over the quarter was $26.1 billion, down from a revised $30.4 billion in the June quarter (a decline of minus 14.1%). The combined value of loss-making sales rose 3.2% to $308 million.

But note the following from the report:

‘Through the September 2022 quarter, 96.2% of house resales made a nominal gain, compared with 87.1% of unit resales.

‘Houses accounted for 67.8% of resales through the September quarter, but only 38.1% of loss-making resales.

‘Units accounted for 32.1% of resales in the September quarter, but 61.9% of lossmaking sales.

‘Both houses and units saw a decline in the incidence of profit-making sales in the quarter.

‘Despite national house values declining faster than units through the three months to September, units saw a faster deterioration in the incidence of profit-making sales. ….

‘The rate of lossmaking house sales rose a comparatively small 40 basis points to 3.8% in the quarter, while loss-making unit resales were up 110 basis points to 12.9%.

‘This means a loss-making unit sale was almost three times as likely a loss-making house sale through the quarter.’

So just a cursory glance at the report will show that you have a better chance of selling for a higher profit if you own a house on its own block of land, compared to a unit on shared land.

| |

| Source: CoreLogic |

This is evident in the ‘Pain and Gain’ report, no matter what the holding period.

Still, many capital growth-seeking investors still fall into the trap of purchasing the wrong type of property.

Obviously, a house on a block of land is more expensive than a unit in the same area. So typically, the choice to buy a unit (apartment, townhouse, or villa) is based on budget.

But the bottom line — and from my own experience — if you’re looking to max out on capital growth:

- Looking a few suburbs out and buying a suburban house on a block of subdividable land in a prime position within that suburb is going to give you a better chance of maximising the growth potential. That’s in comparison to trying to get a foot in the door on a tight budget and buying a unit or townhouse closer to the city.

My point here is that you do NOT need to be pinned to the centre of town to get the best capital growth.

The type of property you buy is JUST as important as the location you buy it in (as well as the position within the suburb that you purchase).

Let me give you another example of this because many property advocates (buyer advocates, sales agents included) have pumped the myth in recent times that you must invest close to the city to get the best capital growth.

That changed a little during COVID, but now migrants are flowing into the capital cities, likely the same will be preached in the years ahead.

Valuer general data in Victoria provides property statistics for Victoria’s 79 municipalities showing yearly medians by suburb over a 10-year period (2011–2021.)

You can access the Victorian data freely here.

(Note: There is similar data on the sum of the other states’ Valuer General websites, but you have to fish around to find it. Some of the relevant links are as follows NSW, QLD, WA, SA, and TAS.)

The VIC data shows that Bentleigh (a popular suburb 13km from the CBD) has seen its median house price appreciate 7.1% annually over the last 10 years (2011–2021).

Compare that to Seaford, which us much further out (36km from Melbourne’s CBD). Its median house price has appreciated 7.4% over the same period.

That’s only a marginal difference between the two suburbs. There’s not much in it at all. Seaford, an outer suburb, has seen bigger gains in its median over the 10-year holding period.

There are numerous examples of this.

The data shows that if a buyer purchasing in 2011 had assumed they would get better capital growth closer to the CBD and purchased a unit in Bentleigh rather than a house in Seaford, they would have only achieved a piddly 4.4% median gain per annum over the same period.

So, I stress again the type of property you buy is as important as the location you buy it in.

Now there are always examples that can be found to break the rule. But understanding this basic concept is important.

The lesson for buyers is — if you want to benefit from land price inflation (capital growth), shift your focus to an area that sits well inside your budget.

An area that is falling under increased demand from gentrification.

Buy a suburban house on a sub-dividable block in a prime street within that suburb, and it’s much harder to go wrong (i.e., see the price stagnate or trend backwards).

Have a great Christmas and best wishes for the new year!

Best wishes,

|

Catherine Cashmore,

Editor, Land Cycle Investor

Comments