I ran across this headline the other day…

| |

| Source: AFR |

The story focuses on the recent change in market conditions.

It’s resulted in a vendor at the top end of the market achieving their $2.35 million wish price after their property passed in for $50,000 less six months ago at auction.

That’s not surprising.

Market conditions have improved.

Punters are still budgeting for rate increases and are holding back some in reserve.

However, clearance rates are now pushing above 70% — and that is a sure indicator that median prices will keep increasing in the short term.

There just isn’t enough stock to meet demand.

In fact, I know quite a few vendors that have been holding off and waiting for higher prices before selling.

Likely we’ll see that surplus hit the market as we head into the spring months later this year – especially if conditions continue to improve, as I expect they will.

However, the headline of the article ‘House gains more than $50,000 in six months — by owners doing nothing’ reminded me of the well-known quip penned by 19th-century political economist John Stuart Mill.

They ‘grow richer as it were in their sleep without, working, risking or economising’.

Born in London in 1806, John Stuart Mill is remembered as ‘the most influential English-speaking philosopher of the nineteenth century.’

Inspired by his father, James Mill, who tutored his nine children with daily lessons in Latin, Greek, French, history, philosophy, and politics, John Stuart Mill was a leading economist and prolific logician. He dedicated his life to championing the causes of liberty and equality while advocating radical ideas, such as the abolishment of slavery and equal rights for women.

The above quote is perhaps better contextualised with the rest of the paragraph.

Writing on the moralities of taxation in Book V, Chapter II of Principles of a Political Economy, Mill comments:

‘The ordinary progress of a society which increases in wealth, is at all times tending to augment the incomes of landlords; to give them both a greater amount and a greater proportion of the wealth of the community, independently of any trouble or outlay incurred by themselves.’

(i.e., Land absorbs the gains of economic progress.)

‘They grow richer, as it were in their sleep, without working, risking, or economizing.

‘What claim have they, on the general principle of social justice, to this accession of riches?

‘In what would they have been wronged if society had, from the beginning, reserved the right of taxing the spontaneous increase of rent, to the highest amount required by financial exigencies?’

From this, Mill concluded that the government should collect society’s economic rents instead of taxes that impede productive labour and industry.

Including taxes on the improvement and the transfer of property (stamp duty), which he said should rather be: ‘distributed over the land generally, in the form of a land-tax.’

He was not the first or last to do so.

He followed a long line of influential activists, from Thomas Paine, who, in his 1797 book Agrarian Justice, stressed:

‘Men did not make the earth…. It is the value of the improvement only, and not the earth itself, that is individual property…. Every proprietor owes to the community a ground rent for the land, which he holds.’

To most recently, Dr Ken Henry, who chaired Australia’s Future Tax System Review in 2010, noted:

‘… economic growth would be higher if governments raised more revenue from land and less revenue from other tax bases.’

The classical economists recognised that unless profits from the ‘enclosure of the commons’ — land, water rights, minerals, etc. — were effectively collected and shared for the benefit of the community. Then all productive gains, every improvement in society and the economy would be capitalised into rising locational land values.

It would enrich those that owned the assets but more so for those who created the credit and traded on the debt — the financial sector.

The late great economist Mason Gaffney expanded on the theory, coining the acronym ATCOR — All Taxes Come Out of Rent.

This showed that whether renting or buying, total tax liabilities from whatever area carried by the consumer deduct from the cost of a site to the extent they limit the amount a buyer is both prepared and able to pay.

What does this mean?

Well-facilitated land (rich in amenities) essential for every activity and sustenance of life is limited by accessible supply.

In developing economies, it falls under consistent demand.

Therefore, removing stamp duty (without replacing it with adequate land taxation) leaves more in the pocket to bid up the price of land.

Reduce construction costs or income taxation, and the same is effectively true.

Thus, it follows that the removal of all taxes would naturally wash up into higher prices for real estate, which in theory, leaves the resulting rise in the economic rent of land ‘just’ enough to replace the forgone revenue.

(For more, see Fitzgerald 2013, ‘Resource Rents of Australia’)

As it is, it’s the tax system that influences how punters invest.

Real estate continues to be used as a hedge against the disproportionately destructive taxes that fall heavily on income and productivity. Pushing people to speculate on land as a way to avoid this and build wealth.

After all, no matter how high your gross income may be, you can reduce your taxable income as much as you like simply by buying enough negatively-geared property.

It’s this artificially reduced taxable income used by ATO statistics on negative gearing to support the property lobby’s claim that most negative gear-ers are not wealthy — but rather average ‘mum and dad’ battlers.

Still, you have to understand how tax policies impact the cycle in order to know how to game it.

The underpinner of it all is that no one wants to work for a living.

Why would you when you can speculate your way to wealth in a country that’s economy is choreographed around the FIRE industry (finance, insurance, and real estate)?

As it is, gains in the property sector continue to outweigh other investments.

We’ve all heard the real estate promoter’s cliché that property doubles in value every 7–10 years, right?

It’s a somewhat disputable stat.

Yet it is absolutely applicable to the most populous cities at least.

Principally, Melbourne and Sydney.

The claim comes from median price data.

Take the bayside suburb of Ormond in Melbourne as an example.

Some 12km southeast of Melbourne city.

In 2011, the median price of houses was $912,500.

By the first quarter of 2021, it had more than doubled to $1,895,000.

The median is merely the middle figure of a bunch of sales. So, it can cloud the data slightly.

In other words, not each and every house in the suburb may have doubled in value over that 10-year period.

You have to know what to buy.

The truth is, though, there are many examples where properties have tripled in value in the same period of time.

The key here is having the knowledge to know what and where to buy to get those gains.

Here is a recent sale that gives a stunning example of what can be achieved if you know what you’re looking for:

| |

| Source: Realestate.com.au |

| |

| Source: Realestate.com.au |

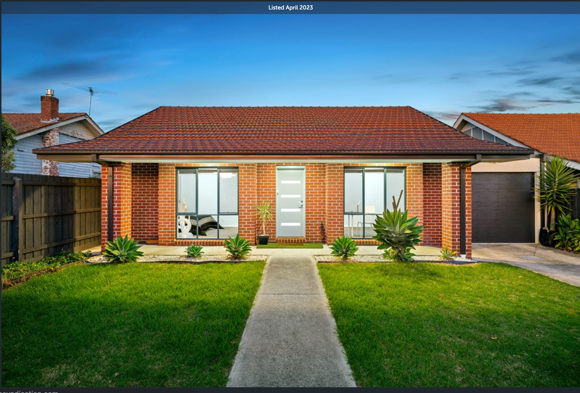

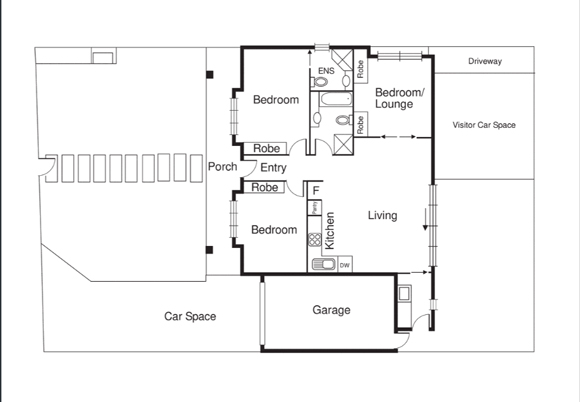

A three-bedroom, two-bathroom front unit in a sub-division of six in Ormond, Melbourne.

Purchased new in 2017 for $305,000. Sold a few weeks ago for $1,095,000.

It’s more than tripled in price in six years!

That’s a pretty good return — considering the owner did nothing to produce the increase.

By subscribing to Cycles, Trends & Forecasts, readers can gain exclusive access to crucial insights that will guide them in making investment decisions for maximum wealth accumulation across all stages of the real estate cycle. This valuable information applies to both stocks and property investments. Discover more about the benefits of subscribing here.

Best Wishes,

|

Catherine Cashmore,

Editor, Land Cycle Investor

Comments