In 1987, the brilliant economist Robert Solow made an observation that haunts markets right now.

He wrote: ‘You can see the computer age everywhere but in the productivity statistics.’

That was nearly 40 years ago. The personal computer had arrived, and corporations were pouring money into hardware, software, and IT departments.

The promise was transformational productivity gains that would reshape the economy.

The Paradox Returns

The reality back then was nearly a decade of stalled productivity.

We can ill afford a re-run of that era now.

Before modern AI entered the picture in 2022, the world was facing a near-universal productivity crisis. But where are we now?

The numbers from a new international study are striking. Not because they’re shocking, but because they rhyme so perfectly with Solow’s original observation.

Researchers surveyed nearly 6,000 CEOs, CFOs, and senior executives across the US, UK, Germany, and Australia. Around 70% of firms say they actively use AI.

Nearly 90% said AI had no measurable impact on employment or productivity over the past three years.

None.

Another study found AI adoption accelerating, but confidence in the technology plummeted 18% as many said they received little to no training.

Recently, Apollo’s chief economist, Torsten Slok, resurrected Solow’s quip, saying: ‘AI is everywhere except in the incoming macroeconomic data.’

He’s right. After three years of ChatGPT, there are limited signs of AI in official employment data, productivity figures, or inflation readings.

Outside of the Magnificent Seven, there’s precious little sign of it in corporate profit margins either.

Surveying the most recent macro academic studies also hints at a Solow-style lag effect. So is this more hype than reality?

Other side of the Coin

The story is never that simple. Productivity may already be improving.

If we dig deeper into the micro studies, we can see the impact of AI across various roles. Spotty, but clearly an impact today.

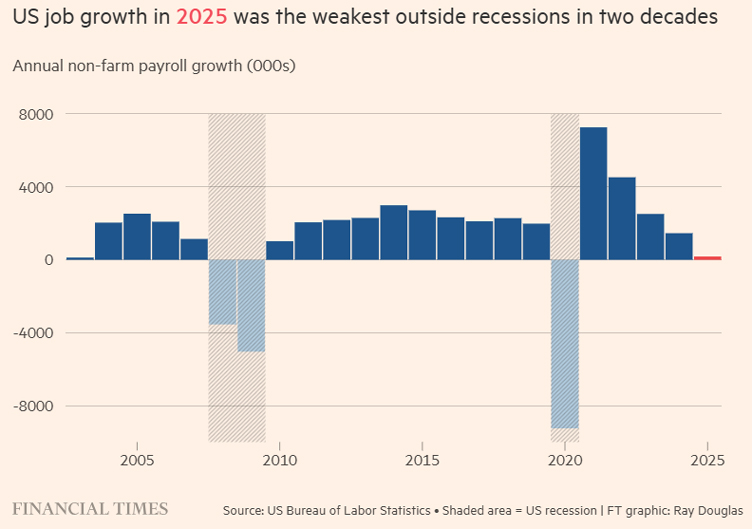

And then there are the latest job figures, which have sparked debate.

The latest US Bureau of Labor Statistics revisions show that 2025 job creation was revised down by roughly 403,000.

That made it the weakest year of job growth outside a recession in two decades, as you can see in the chart below:

Source: Financial Times

[Click to open in a new window]

And yet GDP grew at 3.7% in Q4.

Output growing. Headcount shrinking. That’s what productivity looks like.

Based on these figures, researchers at Stanford estimated that US productivity grew by roughly 2.7% in 2025. Nearly double the decade average.

In a series of papers, they argue we’re already moving from ‘investment phase’, where businesses are learning and reorganising, into a ‘harvest phase’.

That’s where gains finally become measurable.

This is known as the ‘J-curve’. Things look bad before they look good.

That’s because organisations spend time and resources adopting the technology, redesigning workflows, and cutting staff.

It’s a seductive argument. It makes sense that we’d expect the diffusion of AI to be much faster than computers in the 80s.

PC’s required physical installation, networking infrastructure, software development, retraining — the works.

AI’s centralisation means that the changes needed at any one organisation pale in comparison.

But here’s the investor’s dilemma: we still can’t tell yet whether we’re at the bottom of the J, about to launch upward. Or whether we’re simply rationalising expensive technology that isn’t delivering.

Real productivity breakthroughs come from tools that allow people to do things they couldn’t do before, not tools that simply do the same things at lower cost.

Yes, replacing humans with AI in things like call centres is a short-term productivity boost. But are we structurally better off as an economy?

History eventually vindicated the computing revolution. The productivity gains from the IT boom finally showed up in 1995, almost a decade after Solow first noticed the paradox.

That doesn’t mean AI won’t deliver. It almost certainly will, eventually. Some would argue the ‘harvest phase’ has already begun.

But investors are pricing AI stocks at historic multiples and betting that this time, the J-curve is short and sharp, not long and gradual.

What we do know is that the last time the world confidently declared a technology would transform productivity overnight, it took a generation to prove it.

Solow is smiling somewhere.

Regards,

Charlie Ormond,

ATLAS and Altucher’s Investment Network Australia

Comments