n December, I wrote a wire saying the most important thing for investors to focus on right now was the lagged effect of monetary policy.

Two and a half months later, its just another reminder (for me, anyway) that trying to predict the timing of macro forces on the stock market is a tricky, if not impossible, task.

The market went on to rally into the second half of December and all of January. That was partly due to better weather (and lower energy prices) in the northern hemisphere, as well as an assumption that inflation was coming down and the Fed would soon be done raising rates.

As you know, that assumption fell apart in February. The Fed is set to raise rates further than previously expected, and any prospect of rate cuts later this year or into 2024 have now been priced out of the market.

The yield on 2-year Treasury bonds hit 5% this week for the first time since 2007.

Yet the S&P500 still trades on a forward PE of 18.8 times. This represents an earnings yield of 5.5%.

In other words, you can get a ‘risk-free’ 5% yield for two years from a US government bond or a 5.5% earnings yield from the stock market. Your risk premium in this example is terribly thin.

Yet the market doesn’t seem to care. Stocks fell earlier in the week when Powell ‘surprised’ with his hawkish testimony to Congress but the recovery that began from the lows of October 2022 is still intact. It seems nothing can knock this market down to lower levels where some real value might emerge.

It’s a similar picture in Australia

On Tuesday, the RBA raised rates. Somehow, while saying further rate rises would be necessary, the market sniffed out a tweak in the language and decided the RBA could soon be done hiking.

And why not, the cash rate has increased a whopping 350 basis points in less than 12 months. As I said earlier, monetary policy operates with a lag. The effect of those interest rate rises are only just starting to be felt in the broader economy.

But what did the market do when it decided the RBA might be nearly done raising rates? It surged! Talk about a Pavlovian response!

Now, I’ll show you why a central bank on going on hold is not at all bullish for the stock market. But first, traders tripping over themselves to buy might be better looking at the effects of the interest rate rises so far…and then wonder what is to come.

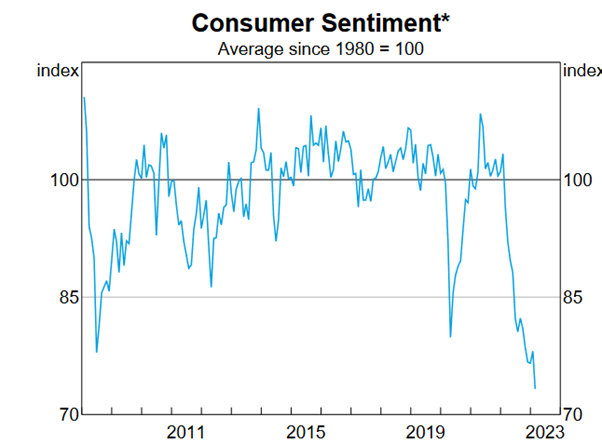

Let’s start with consumer sentiment, courtesy of the RBA’s latest chart pack.

For reference, sentiment is worse than in the GFC yet household spending is strong!

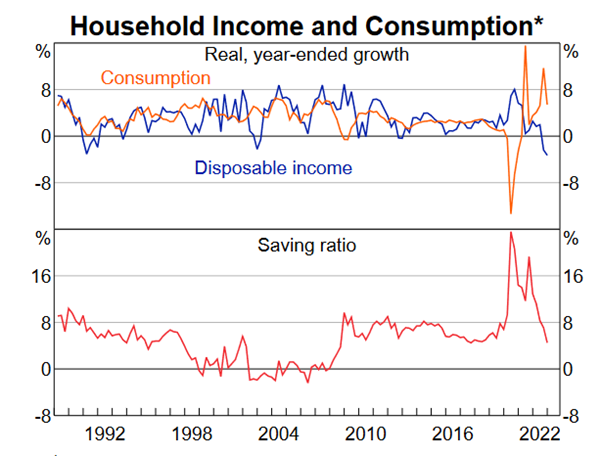

Household consumption was the primary contributor to GDP growth over the past year, growing at a very robust 5.4% in real terms.

Yet as you can see in the chart below, disposable income is running at a decently negative clip. It’s only because households are running down their savings (to 4.5%, the lowest level in five-and-a-half years) that consumption remained strong.

But with the lagged impact of most of the 350 basis points of tightening to hit the economy as we head into 2023, consumption will have much less of an impact on GDP this year.

That’s not the real issue for investors though. It’s the RBA going on hold that should be the worry.

Why a rate cutting cycle is bad news for the market

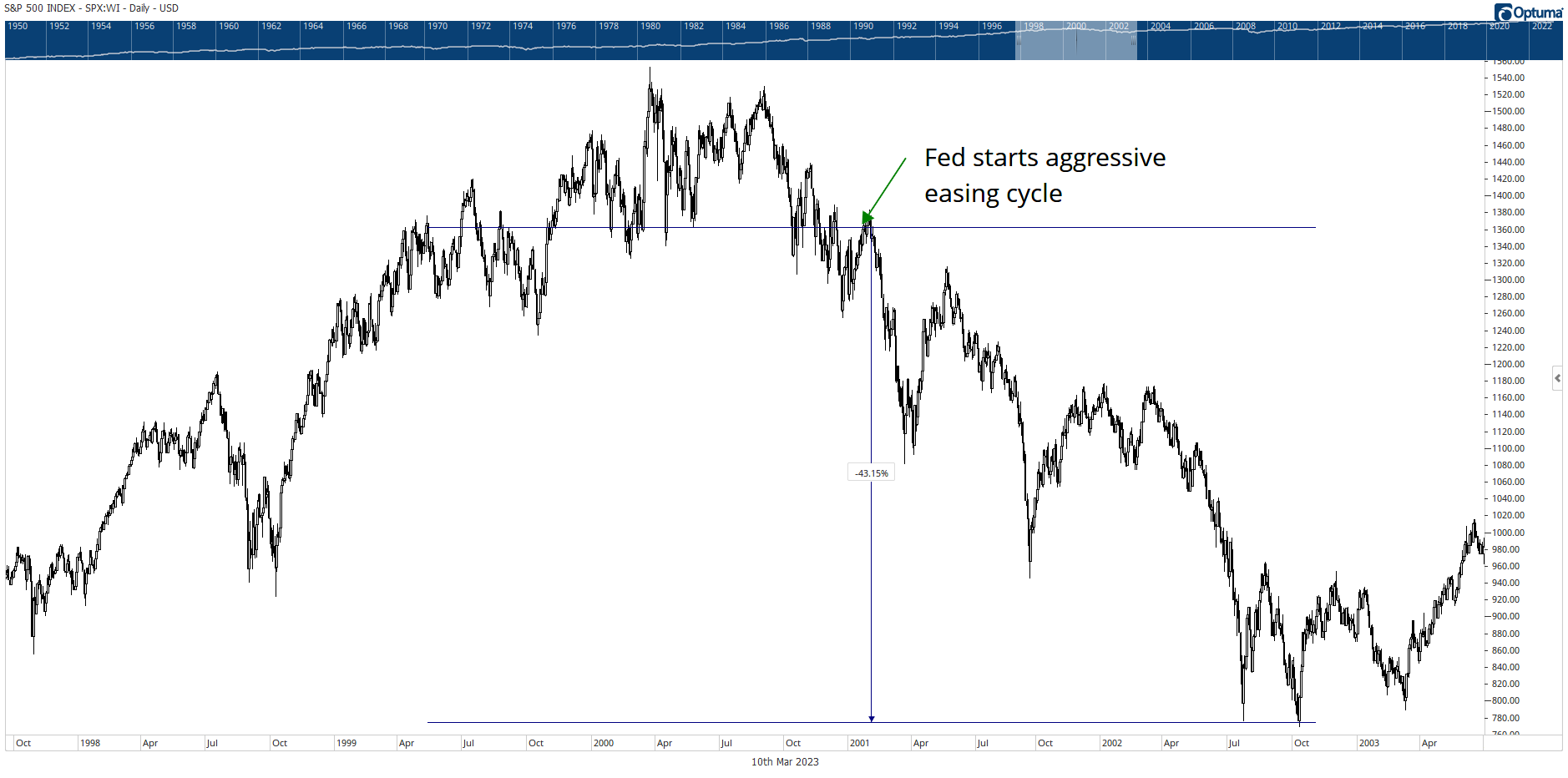

No two cycles are the same. But for a rough analogue, I think the early 2000 bear market is a decent comparison.

Back then, the Fed Funds Rate peaked at 6.5% in May 2000. At the time, the market wasn’t far off its all-time highs. Yay, the Fed’s on hold…time to buy!

The Fed went on hold for the rest of the year. It didn’t start cutting rates until January 2001.

And it continued to cut rates all that year…right down to 1.75% in December. It held them there for nearly a year until it cut again in November 2002 to 1.25%. That is a very aggressive rate cutting cycle.

What did the stock market do?

See for yourself…

It fell. And it continued falling until it made a major low in October 2002.

Let me repeat that for the youngsters. The S&P 500 declined over 40% during one of the most aggressive rate cutting cycles in history.

Why?

Because the economy was in recession (from March to November 2001 we were later informed) which was a result of the lagged impact of the 1999-2000 tightening cycle.

The 2001 rate cutting cycle eventually saw the market recover and boom again. But it took time. This is the key takeaway here.

The Fed and the RBA have tightened significantly over the past 12 months. Next step is for them to go on hold and leave rates there for a while. How long they leave them will depend on the data. But the rate rises are already in the system. It’s just a question of how long they take to work their way though it.

And when the Fed (or the RBA) starts cutting rates, it will be because the pain of the tightening cycle is becoming apparent.

Rate cuts will be a sign that recession is here, and with a recession comes falling corporate profits and falling stock prices.

Yet the market is living in some fantasy land that a pause in the tightening cycle is bullish?

As the old saying goes, those that ignore history are doomed to repeat it.

Put simply, the equity market today is ignoring history. Don’t make the same mistake.

Lest you think I’m being all doom and gloomy, let me leave you with this…

In the early 2000s bear market, the S&P500 dropped around 50% from top to bottom over a period of 2.5 years. The Aussie market, on the other hand, fell just 23%. So not too bad at all!

The broader market could be tough this year. But use any panic selling to your advantage, buy quality stocks on the cheap, and you’ll come out the other side very well placed indeed.

Enjoyed this piece? Check out my publication for more

If you’re interested in staying up-to-date with Greg’s latest analysis on the Australian market, click this link now to get access to Greg’s publication The Fat Tail Investment Advisory.

Regards,

Greg Canavan

For Money Morning