It’s 1852, and a ship called the Flying Cloud has just travelled from New York to San Francisco in 89 days.

That was a record…and it would stand for another 138 years.

Travelling to California by sea meant leaving the East Coast of the US, sailing down the Atlantic to round Cape Horn at the bottom of the Americas, and then back up the Pacific.

Sailors would spend months on the ocean in difficult and cramped conditions.

But there was good money to be made!

The Flying Cloud was a type of ship called a ‘clipper’. The clippers had three masts, lots of sail, and a narrow hull. These design features were for one purpose — speed.

The Flying Cloud couldn’t hold as much cargo as a traditional ship. But in 1852, she didn’t need to.

All her owners wanted was to get her to California as fast as possible.

Why was that?

The California Gold Rush, of course!

In 1848, the American West was a remote frontier far from the manufacturing cities of the original US states on the East Coast.

The discovery of gold sent migrants pouring across the continent.

They found plenty of gold (that is, money).

But there was little to buy in the Californian hills and deserts.

Picks, boots, tents, scissors, booze, you name it — all of them cost a fortune because they were so scarce, and the demand was so high.

That’s what the Flying Cloud was doing, shipping manufactured goods from the East Coast to the West Coast to capture the outrageous margins.

But there was a catch…

California gold produced a torrent of money for businesses and workers in the goldfields, but the gold rush wouldn’t last forever.

Whoever got there the fastest had the best chance of capturing the big money on offer…before the gold depleted.

Hence, the speedy clippers were the best ships to use!

Go to the sign that says: ‘The money is here!’

It’s from this period that investors often cite the wisdom of selling blue jeans and shovels to gold prospectors…rather than running the risk of exploring for gold.

However, investment writer and author Richard Maybury takes this insight to a deeper level.

His book, The Clipper Ship Strategy, describes a way of turning the story of the Flying Cloud into a comprehensive business cycle management tool for today’s economy.

What on Earth does a ship built more than 200 years ago have to do with managing your business, career, and investments today?

Keep reading to find out!

Victoria developed along similar lines to California.

The Victorian goldfields turned Melbourne from a colonial backwater to one of the richest cities in the British Empire by the 1890s.

Get it?

In the 19th century, gold was money.

The money — and best investment opportunities — was where the gold was!

Today, the situation is different. Our money supply is not based on gold.

It’s based on ‘fiat’ government decree.

Today, money enters the economy via private banks or government spending and central bank monetary policy.

2020–21 was an example of a short-term boom based off an expansion in money — like California gold in 1852.

How so?

In 2020, the Reserve Bank of Australia dropped interest rates, financed government spending (‘QE’), and guided that rates wouldn’t rise until 2024.

Money poured into the stock and cryptos markets, plus real estate, as investors rushed to capture where the money was flowing.

Online retailers soared as sales boomed from consumers trapped at home.

It was a gold rush, 2020 style.

Then the government cut off the free money!

But like California gold, these boom times couldn’t last forever…because it was based on an expansion of money and a myriad of government restrictions, not a ‘normal’ economy.

These booms have withered since the RBA and other central banks ended QE, raised rates, and slowed growth in the money supply.

Some naïve consumers and investors are now nursing losses or difficult circumstances.

Consider the following report from this home buyer:

‘Sarah Ibrahim is worried about what will happen when her fixed rate ends in January.

‘Ms Ibrahim and her partner took on a home loan of more than $1.5 million in Sydney, with a deposit of 10 per cent.

‘They are among almost 40 per cent of Australians with mortgages who have locked in ultra-low fixed rates and will roll off them as soon as next year, and potentially face a world of financial pain.

‘“We fixed the majority of our mortgage for two years, and we assumed that in the next few years, they wouldn’t really go up much,” Ms Ibrahim told ABC News…’

On the stock market, analysts are now worried about retailers loaded with excess inventory they will need to discount to sell.

And any company exposed to discretionary spending is under pressure to maintain its former sales and growth as regular Aussie incomes are crimped.

But you can still flourish as an investor in this dynamic.

Richard Maybury’s Clipper Ship Strategy asks:

Who’s getting the money now…and is least likely to lose it?

Right now, investors are wondering if we are in, or going into, a recession.

Spending falls in a recession.

But it doesn’t disappear completely!

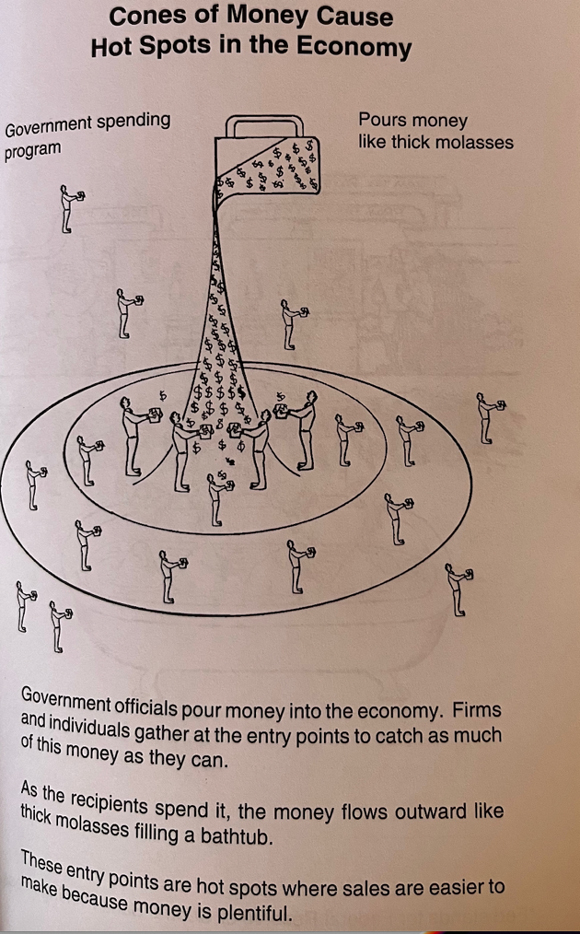

The Clipper Ship Strategy looks for industries that have a resilient flow of money…often because government decree directs it there.

We’re not looking for a short-term gold rush.

We want our clipper ship to sail to industries that have a secure flow of money, regardless of what happens in the economy over a long period.

Richard Maybury calls these industries ‘cones’, based off this metaphorical image from the book:

|

|

| Source: The Clipper Ship Strategy |

Consider…

The Australian Government raises billions in taxes every year. It then spends this back into the economy, plus extra, via the budget deficit.

Thousands of consumers and firms are on the receiving end of this.

A government program like the National Disability Insurance Scheme (NDIS) is a perfect example.

A torrent of money flows from Canberra to pay for this.

The money pouring into this ‘cone’ is huge and likely to keep going up…and up.

A recent report projected the rise to go from $29 billion a year to $60 billion by 2029–30.

It’s nice to think every cent of this goes to those that need it.

I’ve no doubt most of it does, but I’m also sure that plenty is squandered along the way too.

I’ve had a glimpse of this…

Government-mandated profits and high wages

My best friend, Brett, has a severely disabled brother named Stuart who needs 24/7 care.

Brett is allocated a substantial NDIS annual allowance to pay for Stuart’s needs, including paying his daily carers.

The NDIS scheme mandates wages.

A carer earns $55 an hour on weekdays, $70 on Saturdays, and $113 on Sundays.

These are very good wages, considering the position requires no formal tertiary — or any other — qualifications.

I just lost my favourite CrossFit coach to this. She left the gym to work under the NDIS, and probably doubled her wage. A small business can’t compete with those payments.

Specialist medical professionals also service those in need under the NDIS.

Participants in the industry know perfectly well that taxpayers bear these costs, and many charge accordingly.

One physiotherapist tried to bill Brett $700 for a travel fee to go from one Melbourne suburb to another. It was to deliver a report on a replacement wheelchair for Stuart.

Brett didn’t even need the report. NDIS guidelines demand one be produced before he could purchase a wheelchair for his brother.

It cost $5,000.

I’m talking about the report…NOT the wheelchair!

This is how government money can pour into a sector, with high profits for workers, firms, and investors under its flow.

I’m not criticising the NDIS.

Even accounting for this type of excess charge, the government may even save money keeping disabled people at home in family care relative to full-time in government care.

Either way, many disabilities are a terrible, intolerable burden on families.

There was nothing like this before the NDIS.

Brett sacrificed 10 years of his life to care for his brother.

The NDIS has been a Godsend for him and his mother and countless thousands across the country.

I use the NDIS only to illustrate the following point: the flow of government spending here is highly likely to be impervious to the business cycle…and probably politics too.

Who wants to be the politician that takes money away from the disabled?

Not me and not you…and no one else.

Workers and firms in this industry are highly secure and will likely maintain high wages and great margins…unlike gold miners in 1852 California.

I don’t know a great ASX stock to tap into this NDIS spending.

But…

The same dynamic lies behind the entire health and aged care sectors for the foreseeable future…

Baby boomers got da money…and the votes!

There are around 5.4 million baby boomers in Australia, according to the 2021 census. The oldest are now turning 76.

That population figure is about the same number as millennials.

However, baby boomers control at least 50% of the wealth.

We saw their political muscle too, in the 2019 election, when Labor threatened benefits such as franking credits and negative gearing.

Australian Treasurer Jim Chalmers has a mighty challenge in trying to balance the federal budget.

The sheer size of the baby boomers means we can expect health and aged care to become a huge expense on the government finances.

They’ll most likely continue to vote for their own benefits, and not just in Australia but across the world, including — vitally — the US.

As above, it’s a brave government, whether in Canberra or Washington, DC, that tries to go anywhere near these entitlements for such a key constituency.

That puts health stocks at the top of our ‘Clipper Ship Strategy’!

Best wishes,

|

Callum Newman,

For The Daily Reckoning Australia