On Thursday, I walked you through the trap.

A two-punch selloff — Broadcom’s soft AI guidance, then a blowout jobs report — has wiped somewhere north of US$3 trillion from US stocks in a few sessions.

Behind it sits a Federal Reserve that can’t win. Kevin Warsh chairs his first meeting next week with inflation at 3.8% and an economy running hot.

Hike to fight inflation, and America’s US$970 billion interest bill becomes the crisis. Cut rates to please the White House, and inflation expectations slip the leash.

There is no door marked ‘everything is fine’. The long-run trajectory points towards letting inflation run hot, and quietly debasing the currency to cope.

Meanwhile, the punters are lining up for this week’s SpaceX IPO at a US$1.75 trillion valuation, priced beyond perfection.

If you missed Part One, you can catch up here.

Today is the response. How does a long-term investor position for a world where AI spending is real, but the system funding it is under strain?

You own both sides of the trade. And conveniently, both sit under Australian dirt.

The Barbell: One Metal for the Boom…

Copper is the AI trade with the hype stripped out.

Every data centre, every transformer, every kilometre of new transmission is copper. Trump has already invoked the Defense Production Act to fast-track America’s grid buildout, with data centres heading towards 8.5% of total US power demand by 2027.

Meanwhile, supply can’t keep up.

Mining billionaire Robert Friedland recently warned that to sustain even modest global growth, the world must mine as much copper in the next 18 years as it dug up in the previous 10,000 — before you count a single new data centre.

Asking Friedland for his view on copper is like asking a barber if you need a haircut, but the point stands.

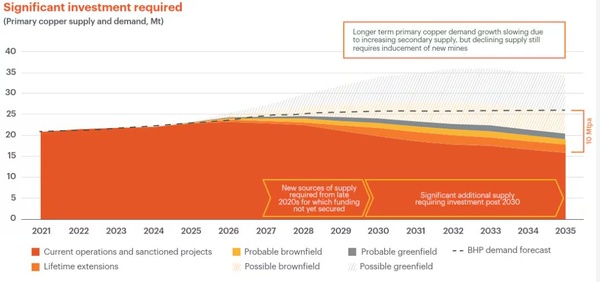

The world’s largest coper miner, BHP, says that roughly 10–15 million tonnes per annum of additional copper is needed over the next decade:

Source: BHP

[Click to open in a new window]

Here’s the thing about that gap in the chart. A chip stock can shed a tenth of its value overnight on a soft forecast, as you saw with Broadcom last week. The copper needed to power that chip has no such problem.

New mines take a decade or more to permit and build. You can’t conjure supply with a press release.

Whether the AI buildout runs hot or merely warm, the metal bottleneck is already locked in and is exposed to many more themes than just data centres.

…And One for the Bill

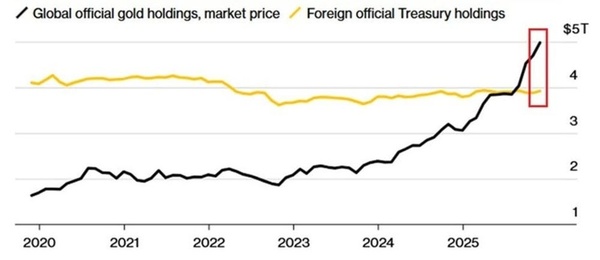

Gold is the hedge on the interest bill arriving.

It’s the one reserve asset that is nobody’s liability, which is exactly why central banks have begun hoovering it up instead of US treasuries.

Source: IMF

[Click to open in a new window]

We’ve seen gold miners sell down amid the Iran crisis and in recent days as well. Almost anyone selling gold right now is doing it for the same reason. The prospect of rising rates in the US.

It’s the golden rule — if you’ll excuse the pun. You don’t want to be holding gold when real rates rise. Gold doesn’t earn interest, so your opportunity cost is high.

That rule works fine in normal times. But these aren’t normal times.

There are many historical examples of this rule breaking. France 1924. The US in 1933. The Eurozone crisis of the 2010s, to name a few.

Namely, when rising real rates hit a sovereign power that’s cracking under pressure to fit its interest bill. In those moments, it’s an extremely bullish setup for gold.

That’s because a country that can’t afford the interest on its growing debt pile has two ways out. Either it defaults, which is wildly bullish for gold. Or it prints money to inflate away the debt, which is bullish for gold.

There’s no door number 3 here unless you think AI is about to usher in the next productivity boom within 12 months… Or there’s a spectacular credit crunch in which gold is often the first thing sold, and then the fastest to recover.

If the Fed’s only real exit is inflation, gold is where that pressure escapes.

The Home Ground Advantage

So, one metal captures the upside of the AI bull case. The other insures you against how it’s being paid for.

Now, I know the mood here. Plenty of Aussies grumble about Canberra, tax tinkering, and our ‘old economy’ market, then shovel their savings into US tech.

But in my opinion, this is one of those rare windows where the boring home market is the right market. We dig many of the metals that the next decade runs on.

None of this means piling in tomorrow. Copper has already run hard, and the sector will see violent shakeouts — we’ve seen some this week.

This theme means thinking in years, not sessions.

Position for the decade’s themes and let the volatility work for you, rather than chasing each rocket on the launchpad.

Money in SpaceX will likely fly in the short term. But eventually that money will go looking for a home with harder foundations.

There’s a good chance that’s right beneath your feet.

Regards,

Charlie Ormond,

ATLAS and Altucher’s Investment Network Australia

Comments