It seems like Groundhog Day for Trump’s tariffs. Over the weekend, the US Supreme Court struck down Trump’s tariffs.

Trump fired back with new ones, and the financial press cycled through the story in about 48 hours.

But this isn’t over. If anything, it’s going to get worse for many.

Whatever changes come, there’s one obvious trade that still holds weight.

First, some context…

On Friday, the US Supreme Court ruled 6–3 that Trump’s sweeping tariffs under the International Emergency Economic Powers Act (IEEPA) were unlawful.

It was the first real check on his trade powers this term.

Trump responded within hours, announced a new 10% global tariff under a never-used 1970s trade act.

A day later, he said he’d raise it to 15%. But when the tariff actually kicked in this week, it was collected at 10%.

The White House said the 15% rate would come ‘later’, without specifying when.

Confused? So is everyone else. And that’s precisely the problem.

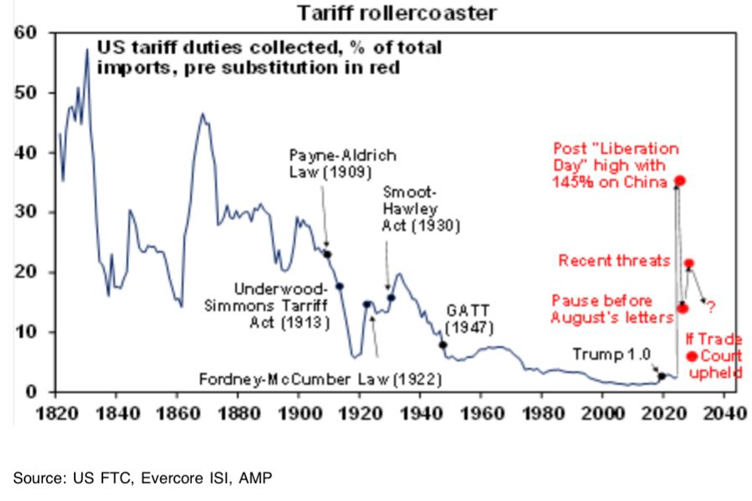

Looking at the US tariff history, you can see how disruptive this moment is for trade.

Source: AMP | Shane Oliver

[Click to open in a new window]

German Chancellor Friedrich Merz put it bluntly, calling tariff uncertainty the ‘biggest poison’ for both European and American economies.

But the blight won’t end there.

The EU has frozen ratification of its deal. India has postponed a delegation visit so they aren’t pressured to sign for a photo op.

Malaysia, Indonesia, Mexico and a host of other countries had not yet ratified their deals. Many are walking back their prior promises. Back to the drawing board.

In the end, many of these deals will likely go ahead.

But in the interim, we’re likely to see a bellicose Trump threaten all manner of escalation to browbeat countries in line. That creates uncertainty.

Markets hate uncertainty more than bad news.

And what we have now is the worst kind: a tariff regime that’s legally fragile, politically unstable, and operationally incoherent.

The Messy Fine Print

The details matter. Trump’s fallback authority, Section 122, is far more constrained than the emergency powers he lost.

It caps tariffs at 15% and runs for just 150 days unless Congress extends it.

No investigation is required to impose them, which is why the president could move quickly. But it’s a stopgap.

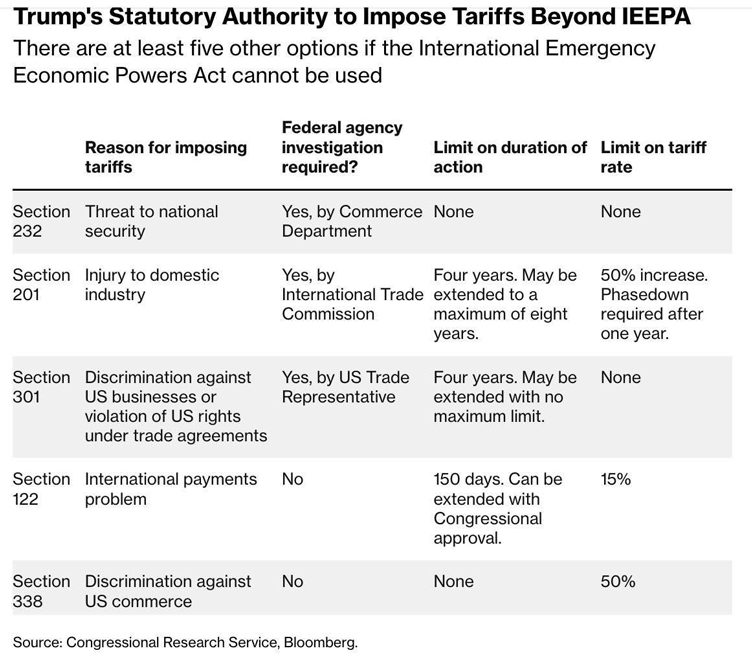

The chart below shows the other tools at Trump’s disposal. Each comes with its own set of constraints. Those range from requiring federal agency investigations to caps on duration and tariff rates.

Source: Bloomberg

[Click to open in a new window]

The critical point here is that the alternatives are slower and more legally vulnerable.

Many take months, not days, to put in place. And the current 10% tariff expires in roughly five months.

The administration hasn’t even initiated the investigations needed to replace it.

Meanwhile, there’s the small matter of roughly US$175 billion in IEEPA tariff revenue that was collected before the Court ruled it all unlawful.

Companies are already lining up for refunds. FedEx has filed suit. Senate Democrats have introduced a bill to require repayment within 180 days.

The dissenting Supreme Court justices called the refund process a potential ‘mess’.

This is all happening against the backdrop of November’s midterm elections.

Trump already had to remove tariffs on hundreds of categories of fresh food last year after affordability concerns threatened Republican candidates in state and local elections.

Any further inflationary pulse from new levies would be political poison heading into November.

The Dog That Bites

What’s really rattled trading partners isn’t the tariff level. It’s the behaviour.

On Tuesday, Trump warned that any country ‘playing games’ with existing trade deals would face ‘much higher’ tariffs under different laws.

China is already poking the bear, urging Washington to abandon its tariffs. They know they now have a favourable position.

China has diversified its export markets. Beijing can afford to wait. Trump, facing midterms, cannot.

South Korea is the clearest example of what happens when Trump feels a partner is dragging its feet.

Back in January, he threatened to hike tariffs on South Korean goods from 15% to 25% because Seoul’s legislature hadn’t ratified its trade deal fast enough.

The threat sent shares tumbling and forced the ruling party to fast-track legislation.

Now, post-Supreme Court, every deal struck under the old authority is in legal limbo.

Trade negotiations that took months to finalise are stalling.

Countries that made major investment commitments in exchange for lower tariff rates are reassessing whether those commitments still make sense.

The Golden Hedge

If you’ve followed Fat Tail Daily for long, my suggestion here won’t surprise you.

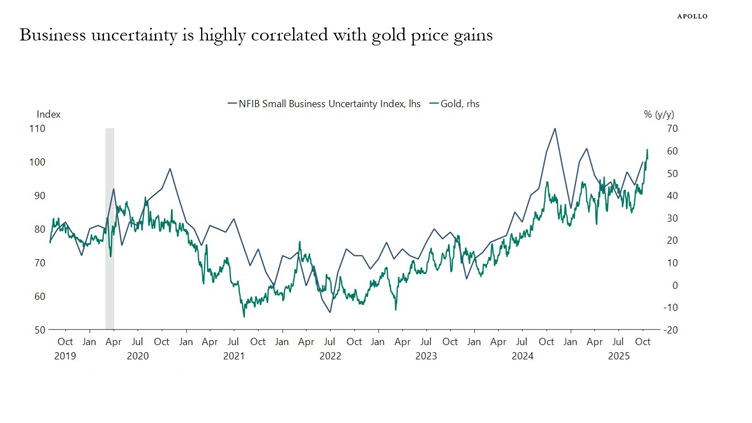

We’ve long argued that policy uncertainty is structurally bullish for gold. And the data keeps proving it.

Apollo’s chief economist Torsten Slok has long argued this point. Take a look at how closely gold tracks business uncertainty. As policy uncertainty spikes, gold follows.

Source: Apollo

[Click to open in a new window]

Gold is currently trading around US$5,190 per ounce. It hit an all-time high above US$5,500 in January. But I don’t think its story ends there.

Central banks bought 863 tonnes of it in 2025. Global investment demand hit a record 2,175 tonnes last year… so the gold trade definitely isn’t over.

Whether you’re new to gold, or an old hand — I’ve got something for you.

From someone who literally wrote the book on gold.

My colleague Brian Chu recently finished a book on gold, called Gold’s True Message.

He lives and breathes the sector.

Recently, he’s been saying that gold is about to enter its Third Act.

One where an entirely different cohort of gold-related companies are about to prosper.

To find out who, click here.

The message is clear. When the rules of global trade are being rewritten every other weekend, gold thrives.

This tariff saga is far from over.

And even if the tariff rules change, the uncertainty isn’t going away anytime soon.

That’s the trade.

Regards,

Charlie Ormond,

Small-Cap Systems and Altucher’s Investment Network Australia

Comments