We’ve said it before in Mining Memo: higher energy prices aren’t a passing trend. They’re the new backdrop investors need to get used to.

Sure, they’ll be pull-backs and sell-offs, but overall, the long-term trend for traditional energy remains up, as far as I can tell.

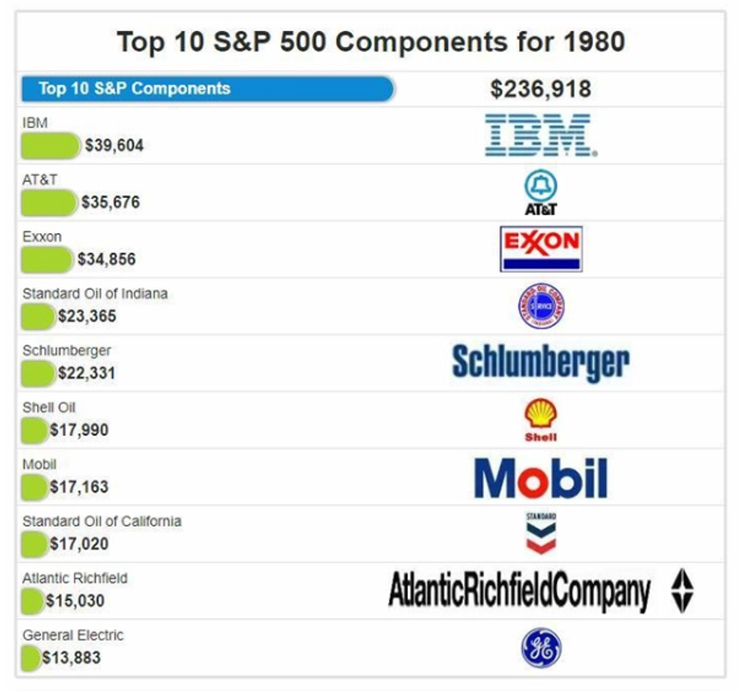

One point in favour of that idea is that oil and gas currently make up just 3.2% of the S&P 500. That’s the lowest weighting in the sector’s history. Back in 1980, that share was around 30% of the index!

Here are ten of the largest S&P 500 companies from 1980 with a combined market cap of $236,918 Billion:

Source: Seeking Alpha

[Click to open in a new window]

Seven of those ten were oil and gas companies.

So, what happened? Why have oil and gas companies gradually faded as a major asset class? Was there a massive drop in oil and gas consumption since 1980?

Not by a long shot…

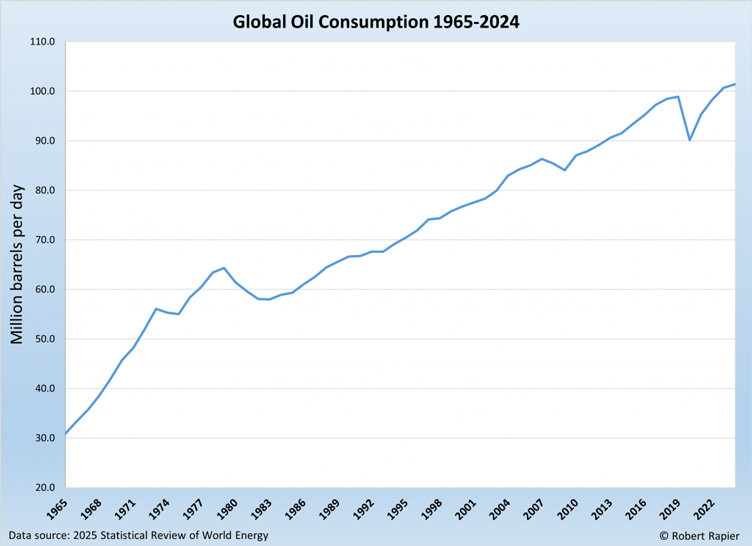

In 1980, global oil consumption was approximately 63.1 million barrels per day. By 2022, consumption broke through 100 million barrels per day for the first time ever:

[Click to open in a new window]

Demand hasn’t receded; it has surged since 1980.

So, again, why have oil stocks faded as the world’s most important asset class on the S&P500?

The forgotten sector

For over a decade, the market bought into the idea that renewables would swiftly replace oil and gas.

Capital poured into growth stocks and clean-energy promises instead of pipelines, rigs and processing plants.

Upstream investment in oil and gas has fallen roughly 35% in real terms since 2015. In fact, nearly 90% of what is still spent in the O&G sector goes toward offsetting the natural decline of existing fields, not developing new supply.

Meanwhile, the International Energy Agency has pushed back its projection for peak oil demand. It was once expected around 2030. The IEA’s latest outlook has the peak arriving closer to 2050.

Two decades of assumed demand, and next to no new supply being built to meet it.

The conflict disrupting the Strait of Hormuz, the corridor that carries roughly a third of the world’s traded oil, has been described by the International Energy Agency as the largest disruption in the history of the global oil market.

But as I’ve pointed out in several editions in the past, the oil market was already a slow-moving train wreck given the lack of investment into what is perhaps the world’s most important industry.

Time to Prepare for Oil’s Final Act

As always, the smart money moved first…

Warren Buffett steadily trimmed his stake in Apple heading into 2026, redirecting more than fifty billion dollars into energy names.

Ray Dalio and Stanley Druckenmiller, two of the most closely watched investors alive, have also been building exposure to real-economy assets, citing the same themes: government debt, a weakening currency, and the end of the ultra-low-rate era.

These are some of the most successful capital allocators in history, so it’s worth watching what they do.

We’ve flagged before in Mining Memo that higher energy prices are here to stay, not because of a single war or a single headline, but because the underlying supply story has been falling apart over the past two decades.

If you’re looking to understand this idea in more detail, I suggest you check out our latest presentation here. Time may not be on the investor’s side.

Until next time.

Regards,

James Cooper,

Mining: Phase One and Diggers and Drillers

Comments