I used to watch CHIPS…

Nas, Illmatic, Half-Time

Markets remain rough out there.

And all eyes are on the Nvidia earnings to come on Wednesday, US time

Word on the street is that it’ll be another earnings beat for the monolithic chip-maker.

That might be enough to give a sliding market a brief sugar hit.

Meanwhile US billionaire Peter Thiel has just sold out entirely of the AI chip maker.

The smart money has had their fill.

Filings of the +900 hedge funds in the US reveal a pretty even split: 161 increased their investment positions in the giant chipmaker, while 160 decreased them during the three months to September.

Is the top of this market in?

For now, it looks like it.

When the market is as concentrated as this, the answer is yes (~7-8% of S&P 500 is Nvidia).

And will AI bubble burst fears become a self-fulfilling prophecy?

I don’t think so. I think there’s plenty more to come from the market over the course of 2026.

Given the ASX largely follows the US market, today I’ll lay out two scenarios that are relevant to both countries.

Both scenarios have me watching central bank machinations far more than the earnings of a wildly popular computer chip maker.

It ain’t hard to tell: this

market needs a rate cut…

Even if Nvidia crushes earnings in the next 48 hours, there is nothing sweeter to markets than a rate-cutting cycle.

Trump looks like he’s willing to budge on the tariffs to get US inflation under control.

That could give the Fed room to cut, and one Fed governor is already calling for it.

It’s been an almighty run for stocks so far.

But warning signs are sounding in the US debt market: auto loan and credit card delinquencies are at 3.0% (highest since 2010) and 7.1% (highest in 14 yrs).

In Australia, many mortgage holders are just clinging on at the current rates.

Debt breeds debt though. Things compound in both directions – such is the fractal-like complexity and exponentiality of fractional reserve banking.

In recent years, private credit has emerged as a “creative” financing solution in a world of high rates and increased regulation of the banks post the GFC.

Beware the words “creative” being attached to anything financial.

In my book, private credit (an opaque form of business-to-business lending) is the elephant in the room, and it’s starting to smell.

If Americans are struggling to pay their car loans and credit cards, I hate to think of what’s under the hood and on the books at the big private credit firms.

Private credit could well be the Fannie Mae and Freddie Mac of our generation down the track.

But here’s what the pressure release valve is for that brewing mess…

A Fed rate cut.

Scenario #1: Kick the can down the road

Here’s how I think it could play out in the first scenario.

Politics and central banking dance together and it is a delicate tango. You need both to be stepping to the same tune for an epic bull market to play out.

And boy does Trump love a buoyant stock market.

The music starts with Trump strategically easing off on tariffs..

This would give the US Fed room to cut – before the US Fed Chair Jerome Powell’s term in ends in May next year.

And then, in May, he’ll get what he wants anyway.

Markets largely trend sideways or marginally up for the next few months in this scenario.

Then start to move up again ahead of the new US Fed Chair appointment.

Scenario #2: The market

forces the Fed’s hand

Suppose the market keeps sliding despite a US Fed rate cut and an Nvidia earnings beat?

Even worse, the private credit boom threatens to unwind?

Suppose the market end times actually are upon us.

(I find this thinking remarkable and premature as both the US markets remain well, well above the early 2022 tops)

But still let’s contemplate it.

Well for starters, then the Fed is forced to cut even more aggressively.

Surprise boring fact: the political and central bank decision makers all hold LOTS of shares.

Indeed, many of them use their advanced and often pre-market knowledge to profit:

Source: Bloomberg

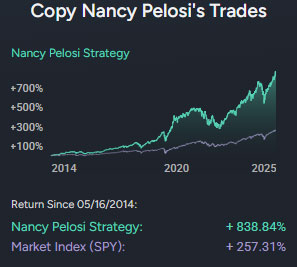

Thankfully, you can now “copytrade” major US political figures, like US House of Representatives “trading genius” Nancy Pelosi:

Source: quiverquant.com

So if markets go down enough to force the US Fed to cut because of fear of market contagion (and damage to their own wallets), then the market should bounce back strongly.

Really strongly.

Why?

Call me a cynic, but it’s because the whole system is rigged to benefit vested, powerful interests.

In both scenarios, the market eventually re-takes these tops and pushes higher than people expect.

And for way longer than they expect too.

The market’s sudden bout of rationality around AI is merely an aberration.

My reasoning is that it will get far more unreasonable (and exuberant) in 2026 because that’s just what happens in every bull market when central bankers have ammo and start to use it.

That’s why I think it’s merely half-time in markets.

Regards,

Lachlann Tierney,

Australian Small-Cap Investigator and Fat Tail Microcaps

Comments