Two of the world’s mining giants are circling each other.

Rio Tinto and Glencore confirmed this week that they’re in preliminary talks about merging some or all of their businesses.

If it happens, the deal could potentially create one of the largest mining companies on the planet, worth roughly $207 billion.

The market’s reaction was telling.

Rio’s shares fell almost 10% on the news, while Glencore’s US-listed stock jumped 5%.

The market’s verdict? Glencore could be getting the better deal and Rio shareholders aren’t thrilled about paying up.

The Copper Arms Race

Strip away the corporate jargon, and this deal comes down to a single word. Copper.

Glencore digs up about a million tonnes each year and wants to double that. Rio extracts roughly 800,000 tonnes.

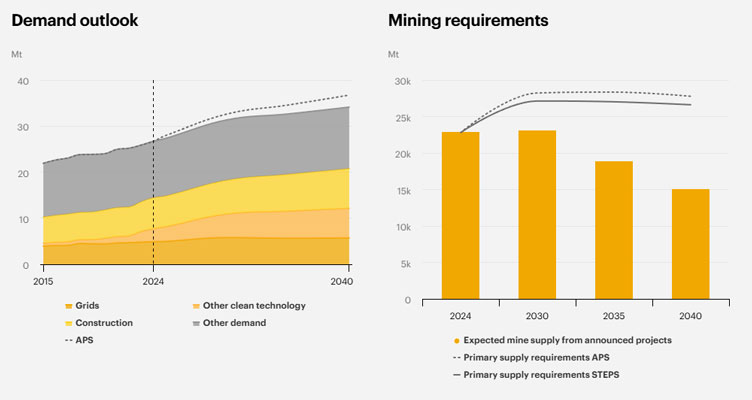

Combined, they’d control roughly 7% of global copper production. That’s a commanding position in a market where demand is surging, and supply is lacking.

The International Energy Agency estimates existing and planned mines will only deliver 70% of what the world needs by the mid-2030s.

Source: IEA

[Click to open in a new window]

Every solar panel, wind turbine, and EV motor needs copper. The AI boom only intensifies that demand.

The world’s biggest miners know this. They’re racing to lock up supply before it becomes genuinely scarce.

A Wave They Almost Missed

This isn’t news for Australia’s mining giants. It’s actually a point of embarrassment. They’ve been talking up the copper boom for a decade while largely sitting on the sidelines.

Former Rio boss Jean-Sebastien Jacques dismissed copper deal prices as overblown a decade ago. His replacement took a similar line, warning about paying too much in a hot market.

BHP’s leadership has echoed similar concerns about stretched valuations.

Meanwhile, copper prices have surged roughly 150% since March 2020. Goldman Sachs is tipping another 30% rise by 2035.

Their caution was understandable. Bad deals have burned both companies in the past. But that discipline may have cost them.

In the catch-up, BHP has attempted to acquire Anglo American twice. First with a $75 billion offer last year, then another crack at $79 billion in November.

Both times, Anglo’s CEO Duncan Wanblad slammed the door with little said.

Now, Anglo is merging with Canada’s Teck Resources in a $92 billion deal. It’s one of the biggest transactions in mining history, and it’s explicitly pitched as a copper play.

BHP and Rio have likely watched that with a mixture of fascination and frustration.

Timing and Fit

This isn’t the first time Rio and Glencore have talked.

Glencore approached Rio in late 2024, but the prior CEO wasn’t interested in mega-deals.

Since then, Rio has changed leadership. Simon Trott took the top job in August last year, reportedly chosen for his willingness to consider bold moves.

And this is certainly a bold move. Under takeover rules, Rio now has until February 5 to make a formal offer or walk away.

A deal won’t be simple. The two operate in very different ways.

Glencore is known as opportunistic, aggressive, and comfortable with risk. Rio is classically conservative. Focused on long-life assets and steady returns.

Then there’s Glencore’s baggage. The company has faced a string of corruption matters in recent years. Plus, its coal business doesn’t fit Rio’s decarbonisation narrative.

Integration risk is real for this potential mega deal.

Deal or No Deal?

Despite their conservative shuffles, neither BHP nor Rio has been standing still.

BHP has boosted copper production 28% in three years. Copper now represents 45% of its earnings, up from 29%.

Rio has pushed ahead with its expansion in Mongolia. Its Oyu Tolgoi mine is on track to become a top-five global copper mine. Copper now accounts for 19% of group earnings, up from 13% in just three years.

Those aren’t insignificant moves. But both companies would dearly love greater exposure.

The question is whether Rio is willing to pay Glencore’s price and whether shareholders will back a deal of this scale.

Watch the February 5 deadline. It will force clarity.

Either Rio steps up with a formal offer, or it walks away. Given the strategic logic, a deal remains possible. But the terms will be muddy and nitpicked to no end.

One thing is certain: bargains in copper are getting harder to find.

Regards,

Charlie Ormond,

ATLAS and Altucher’s Investment Network Australia

Comments