As predicted last week, stocks began trading yesterday with the Dow at less than 30,000. Next target: 20,000.

One headline at Bloomberg tells us that both ‘Goldman and BlackRock sour on stocks’.

Another tells us there are ‘98% Recession Odds’.

Meanwhile, the Dow ‘officially’ fell into a bear market…and is headed lower.

Do we know that the Dow will trade at less than 20,000? No, of course not.

But what we think we know is that the Fed will surprise investors twice. First, on the way down. Second, on the way up.

Many investors are already surprised by the Powell Fed’s steadfast pursuit of lower inflation levels. CNBC caught up with Wharton Professor Jeremy Siegel, who thinks the Fed as ‘gone too far’:

‘“The Fed’s tightening and their talk of super-tightening has just pushed markets way too extreme,” the top economist said in an interview with CNBC on Monday. “[It’s] so extreme I think the risk of recession is so much higher than waffling on inflation.”

‘The central bank has shown no sign of easing its rate hike campaign since inflation reached 9.1% this summer, with Fed Chair Powell vowing to keep hiking rates until the “job is done”.’

‘Gone too far’, was what analysts said after the Fed’s rate hike in July. ‘Gone too far’, was repeated after last week’s 0.75% Fed funds increase. And ‘gone too far’ will be the refrain for the next one too.

But today, we take the other side: we explain why the Fed won’t go far enough.

Crushing optimism

For the moment, the Fed has no choice. It is way behind the curve…behind the eight-ball…and behind the times. It has to make a Volcker-like gesture — bold, resolute — to regain its credibility.

Like a torturer, the Fed must administer enough pain so the victim knows it can get a lot worse. But the Fed has no intention of killing the stock market. Instead, it is merely waterboarding it…

…and yes, investors will cough and sputter; they will think they are dying. Elizabeth Warren and other feeble-minded opportunists will complain that the Fed is murdering ‘America’s hardworking families’.

But it won’t matter. The Fed has a job to do. Mr Powell says he aims to ‘keep at it’ until the job is done.

Will that be at 25,000 on the Dow? Or 20,000? We don’t know. It’s obvious that it can’t go on forever. The first surprise will be how far it goes on before it comes to an end.

In that regard, every bounce in the stock market…and every ‘buy the dip’ forecast…calls for another dunk. The Fed has to crush optimism…it has to convince investors that their only hope is to ‘give up’, and cut their losses. Sell everything — the stocks, the houses, the kids…everything.

That is when the second surprise comes.

Going all the way

The Fed will never really ‘get the job done’. For that would mean going all the way — squeezing out the excess debt…getting inflation down to 2%…and bringing stock prices down to more normal levels. Warren Buffett calculates that the stock market is historically worth from 70–80% of GDP.

Currently, it is about two times that much…which implies a 50% haircut still to come…or a Dow of about 15,000 and a loss to investors of about US$20 trillion — from the stock market alone.

Additional sell-offs in the bond and real estate markets would mean staggering losses for the asset-owning class, totalling as much as US$50 trillion.

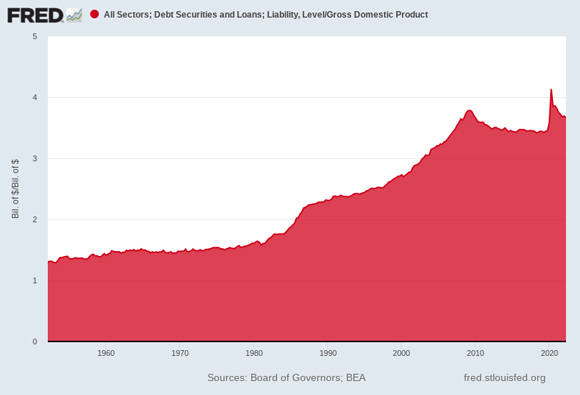

And thanks to the Fed’s zany zero interest rate policy the nation has about US$47 trillion in debt it wouldn’t otherwise have. Just as there is a longstanding relationship between the stock market and GDP, so is there a time-tested connection between debt and output. From 1870–2011 — 141 years — the average was about 180% — debt/GDP.

Now, the ratio is off the charts at 375% — more than twice as high. That puts excess debt at about US$47 trillion. The feds were counting on the ‘inflation tax’ to get rid of it.

Colleague Dan Denning sent over this chart as we were going to press the other morning. It shows ‘all sectors debt’, that is, households, businesses, and governments (state/local/federal):

|

|

| Source: Board of Governors; BEA |

‘Makes you wonder’, mused Dan. ‘We didn’t really get any GDP bang for all those debt bucks. What did we get? A huge bond bubble, a huge stock market bubble, and a huge real estate bubble. Massive distortion in the business cycle and capital formation. More wars and bombs. And a massive wealth transfer from the poor and the Middle Class to the bi-partisan Nomenklatura.’

And yet, Jerome Powell has barely started. If he raises the key rate by more than 4% in December, as advertised, it will still be only half of the inflation rate. And his quantitative tightening program has so far gone nowhere. Fed holdings are still up for the year.

But if he keeps at it, the pain and fear will intensify. Stocks will crash, along with corporate and household-sector bonds. Businesses and households will go broke. Real estate prices will sink.

Homeowners will be turned out into the cold, unable to refinance their mortgages…or they’ll lose their jobs in the general depression. The federal government will have to make dramatic cuts — approximately equal to its entire military budget — to avoid defaulting on its debt. And ‘the people’ will rise, begging for handouts from their penniless rulers…and threatening revolution.

The ‘pivot’ can’t come too soon, but it mustn’t come too late. Then, the Fed will react to the ‘emergency’ — it will switch from saving the nation from inflation to saving it from deflation!

Pride before fall

What a great and glorious day that will be. Chairman Powell will be the hero of the day; he will have vanquished inflation. He will have ‘kept at it’ until the pips squeaked, and the deciders howled.

Then, his moment of glory come…an entire nation will be at his feet…eternally grateful…dipping their fingers in holy water so they might press them to his lips.

Inflation will be on the decline. But it won’t be beaten; it won’t be dead. For that would mean suffering much too great for Powell…or for the elite. They own most of the US’s financial assets. And were the Fed to insist on going all the way — and unwinding the huge ball of debt, delusion, and delinquency that it created — it would be the elite who paid most of the price. It would also mean an end to their unbridled power. Inflation has been a policy choice of the federal government for many years; it is what permits the feds to spend so much money.

And some time in the months ahead…all of them — the great and the good…economists and lobbyists…Wall Street, academia and the defence industry…Republican and Democrat — will come together to thank Powell for his victory over inflation…and insist that he stop fighting tout de suite.

Inflation on the run, it will be time to face the new threat — the collapse of the US economy. How?

With more money printing, of course.

Regards,

|

Bill Bonner,

For The Daily Reckoning Australia