Gold’s raging bull market has finally mainstream.

It just hit yet another milestone – US$4,000 and AU$6,000 an ounce.

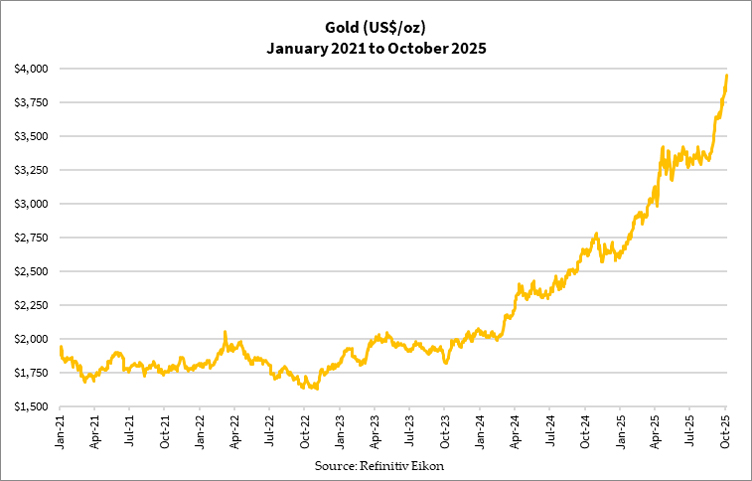

Less than a year ago gold broke above AU$4,000 for the first time. I still remember I was in Singapore at that time. Coincidentally I went to visit BullionStar to pick up some bullion that I had pre-ordered.

I’m sure the staff would have preferred I hadn’t done that since the price moved a bit since I put in my order!

Let me show you how last year’s rally in gold and silver looks:

Notice how the move last year pales in significance to what we’ve seen since this August.

Make no mistake, this bull market has gone parabolic. It even feels a little overstretched.

For a gold bull to call gold and silver overstretched is saying something! I’ve been on record talking about this. Like in my appearance on Ausbiz on Tuesday morning, just as gold broke that critical US$4,000 barrier:

As I said in that conversation, I remain bullish in the long-term on gold and precious metals mining stocks. However, I’m bearish in the short-term.

That’s what I want to unpack further in today’s update.

What happens next

In the past, gold’s rise coincided with the movement of the US dollar and long-term inflation expectations in the US. You can see how gold and the US long-term real yield tend to move in opposite directions:

This trend seems to have fizzled out in the recent months. Gold’s been rising quickly despite the real yield sitting at 2009-10 levels.

There’s a reason for this: we’re in the midst of a tectonic transition worldwide. Not just financially, but geopolitically and ideologically.

Yes, something big is heading our way…

Curtain calls for the petrodollar system

For over 50 years, the US dollar and gold shared the throne of being money in our global financial system. This slowly began to break down in the 70s. It started with US President Richard Nixon ordering the temporary (so he said) halt to the exchange of US dollars into gold. He wanted to prevent gold from leaving the US. That ended the Gold Standard.

To elevate the status of the US dollar after the decoupling, the then-Secretary of State Henry Kissinger engineered an arrangement with the Kingdom of Saudi Arabia to force all transactions of crude oil to proceed using US dollars. Every country had to hold US dollars as reserves to get oil, securing a continuous demand for the dollar.

This allowed the US to continue to run deficits and create more US dollars, with other countries bearing the burden through the oil trade. It was an ingenious plan given that oil powered the world and technological advances increased its demand over time.

However, as you know, this arrangement isn’t bulletproof. Debt and deficits can’t continue ad infinitum. At some stage, they would stifle productivity.

We saw signs of the system in serious flux since the turn of the millennium. The subprime crisis of 2007-09 merely brought it out into the open.

The subprime crisis nearly caused the financial system to implode as the flow of credit stopped. The solution was for central banks and governments to step in to spur business activity by providing liquidity. At the same time, attempts to rein in spending to control debt were meant to prevent debt from spiralling out of control.

As you’d expect, they didn’t work. Governments reining in spending had to reverse course as the leaders feared popular backlash. It didn’t help when institutions and wealthy individuals who invest in the markets got richer through asset prices rallying when interest rates dropped.

The grand experiment of creating unlimited currency to revive market confidence caused society’s rich and poor to diverge further. When central banks attempted to reverse this experiment by raising interest rates from 2015 onwards, they realised it was futile. Once the liquidity flowed, there was no viable way to remove it without destabilising the system.

The Wuhan virus pandemic, the subsequent mass stimulus and tightening of the markets wasn’t a new scenario or strategy. It was merely repeating the same thing in a shorter timeframe. It confirmed failure to those who hadn’t realised it a few years before.

A global ideological and geopolitical shift

While cracks are now multiplying and causing the petrodollar system to crumble further, a bigger shift is accelerating its demise. That’s why we’ve seen gold rise so quickly even though the US long-term real yield and the US Dollar Index [DXY] are holding up.

It goes beyond the financial markets. We’re talking about a change in government policies on trade, foreign relations and national security.

Until recently, liberal and conservative governments were distinguishable by their social, economic and cultural policies. They also have a distinct motivation on whether to create a bigger or smaller government from their spending policies.

However, the world has experienced over 15 years of a zero interest rate environment. Voters now believe money does grow on trees after all. The backlash in cutting spending has made both sides of the aisle realise that doing so would guarantee a political suicide.

The pantomime show of changing governments every few years and toggling with deficits and surpluses has failed. Deficit spending is here to stay for most countries now, irrespective of which party gets control.

Just this weekend, Japan appointed its first female Prime Minister Sanae Takaichi. This will send shockwaves not just on the Asia-Pacific markets and the geopolitical scene, but her policies will reverberate through to the global financial markets. She viewed the late Former PM Shinzo Abe as her mentor and seeks to repeat his economic policies to try to revive the country’s zombified economy.

Forget about austerity, let the liquidity flow and debt to rise.

Nowadays, the policies of governments on opposite sides of the spectrum differ in particulars, but the implications on debt levels are almost indistinguishable. They’re all mortgaging the future to try to fix the past and present mistakes. The unintended consequences will dig a deeper hole in their balance of trade and national wealth.

Now comes the important question: who will plug that hole? Liquidity conjured up magically becomes debt in the future that is repaid by productivity, taxes or more borrowing.

Is there no wonder why gold is rising so quickly? No one is plugging up that yawning hole. The opposite is occurring.

Steer clear of the financial quicksand by doing this

Gold didn’t become more valuable. Our currencies are disintegrating in front of our eyes.

To be fair, I don’t believe it’s simply a slippery dip all the way to oblivion. The system will splutter and appear to jolt back to life. There are signs of a temporary improvement in some countries, industries, and for the general populace. The market might respond to that, causing gold to correct given how far it has run.

But this will be temporary at best. The only way that this system won’t march to its destruction is if countries stop fighting each other, people spend within their means, and voters don’t push their government to give them free stuff so they put the obligation on the future generation to repay.

Yet old habits die hard. Zero interest rate environment conditioned everyone to easy credit. That allowed them to enjoy now, pay later. And they will kick the can down the road… with the can getting bigger and the wall being closer.

For that reason, gold only has one direction to go in the long-term… up.

If you want guidance to build your wealth and protect your purchasing power through the ups and downs of the gold price cycle, I invite you to check out The Australian Gold Report. Here I provide you with regular updates on what’s happening with the economy and its effects on the precious metals market. You can also build a portfolio of precious metals assets including bullion bars, ETFs, and selected gold stocks.

That’s it from me for now. Have a good weekend ahead!

God Bless,

Brian Chu,

Gold Stock Pro and The Australian Gold Report

Comments