When Iran and the US turned the Strait of Hormuz into a shooting gallery, everyone immediately watched oil.

Fair enough.

But the bigger story for Australia might be gas.

We’ve needed new gas supply in this country for YEARS.

Qatar ships about 20% of the world’s LNG.

And most of it runs through Hormuz and lands in Asia.

Japan, South Korea, China, and India are the core customer base.

Iranian drone strikes are freezing that flow.

In LNG terms, Qatar is gone (for now).

But with oil, the pain at the pump might just be the excuse the RBA needs to finally smash inflation.

Yesterday’s rate rise will hurt, but it might not hurt the market side of things as much as you’d think if you know where to look.

That’s despite the profligate Treasury we have in this country.

Treasury doesn’t even know the difference between net “savings” and gross “savings” — feel free to look into that.

RBA rate rises and gas conundrums

You can already see the damage.

Asian LNG prices have jumped hard, and Europe’s benchmarks have spiked as well.

Everyone is bidding for the same smaller pool of molecules.

Gas is a feedstock for fertiliser, fertiliser flows into food and food flows into CPI.

That pipeline is simple enough even for a central banker to follow.

The RBA came into 2026 hoping the worst of the inflation fight was done.

Now it faces a fresh external price shock it can’t control.

Do they want to hike again? Probably not.

But they probably will.

And do they ignore a renewed energy and food surge? They probably can’t.

That’s how a regional conflict in the Gulf ends up on your mortgage statement in our large coastal cities.

At the same time, buyers are rewriting their contracts on the fly.

They still care about price, of course. But they now care more about flexibility, or more precisely, security of supply.

Australia to take energy

seriously (finally)

Here’s the uncomfortable bit.

Australia went into this crisis on the back foot.

Qatar had already overtaken us as China’s biggest LNG supplier.

Our own export volumes were sliding, and analysts were flagging the impact of rolling off older contracts.

The Hormuz crisis hasn’t magically created new gas.

But what it has created is leverage against a system used to inertia.

Asian buyers now have a 20% hole in their LNG book and a vivid reminder that “cheap but fragile” can blow up overnight.

They’re forced to look at geography in addition to price.

Australia suddenly looks better on that score than it did six months ago.

Which means east coast gas

developers may benefit

This is where things get interesting for investors.

Australia is geographically insulated from the Gulf.

Our tankers sail across the Indian and Pacific oceans, not through Hormuz.

We’re a known political quantity, and thankfully, contract law still usually means something here.

The war changes the conversation.

Put yourself in the shoes of a Japanese or Korean utility.

You’ve watched Russian gas get sanctioned.

You’ve now watched Qatari gas get shut in.

You still need to keep the lights on and back up your renewable fleet.

Do you really want your next 20-year deal tied to the Strait of Hormuz?

Or do you start shifting more volume toward suppliers whose shipping lanes aren’t one drone strike away from closure?

That’s the core opportunity for Australia.

And it should strengthen the hand of existing LNG exporters or future exporters with uncontracted capacity.

It may even finally push east coast gas projects…(the ones that can meet both domestic needs and export demand)…back into serious consideration.

For investors and governments alike.

Of course, Canberra can still botch it.

But zoom out, and the picture is pretty clear.

Iran has reminded the world that chokepoints still matter.

For the first time in a while, Australia is no longer a tired LNG incumbent managing its decline.

We love a managed decline…

But remarkably, it’s a potential safe harbour in a suddenly hostile gas market.

So we NEED to choose to act like one.

As for the government…

Heaven forbid they follow through on an election promise.

Gauntlet is thrown down — prove me wrong.

Manufacturing subsidies for the “thing” economy only work if energy prices come down.

And gas has to be a part of “thing” economy.

Sidebar: in this age of the “thing” economy, there’s nothing more important than chips.

Read my latest presentation on the commodities that go into chips here.

Warm regards,

Lachlann Tierney,

Australian Small-Cap Investigator and Fat Tail Micro-Caps

***

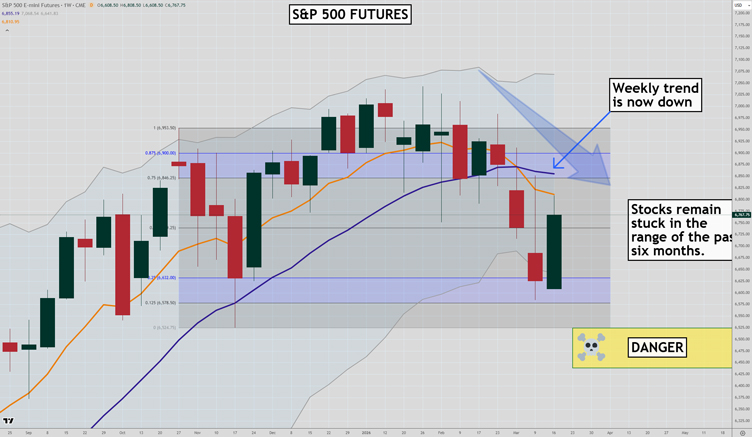

Murray’s Chart of the Day –

S&P 500

Source: TradingView

The S&P 500 remains firmly stuck in its range of the past six months.

Despite ongoing uncertainty from the Iran war, software company meltdowns, and troubles in private credit, the major indices have yet to crumble.

Short positions have been rising with the bearish sentiment, so the risk is rising that good news could spark a short-covering rally.

The 10-week EMA has fallen below the 20-week SMA, indicating a weekly downtrend.

Until that changes, I can remain wary of more downside.

The rally of the last two days hasn’t changed the short-term bearish situation. It has just taken prices up to resistance.

If selling returns around the 6,800-6,900 level, and the low of the past six months at 6,525 can’t hold, I think we will see a rapid decline in the S&P 500 as stop losses are hit.

Regards,

Murray Dawes,

Retirement Trader and International Stock Trader

Comments