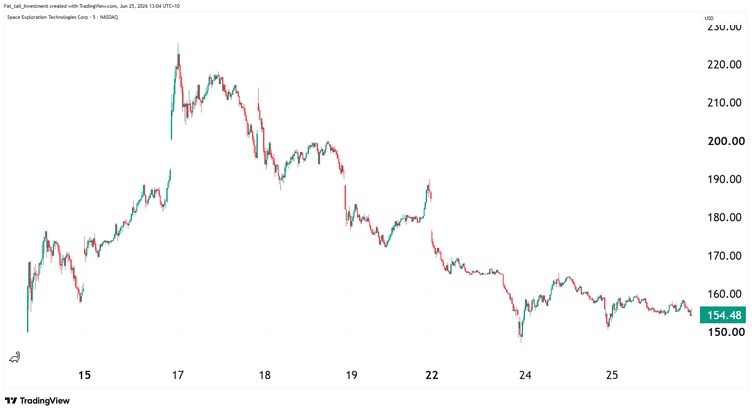

This month SpaceX became the largest company ever to list on a public market.

It priced at a valuation near US$1.77 trillion, then climbed past US$2 trillion once trading opened. The float briefly made Elon Musk the world’s first trillionaire.

As the metaphorical rocket lifted, and the stock soared 40% in days after its IPO, Musk’s net worth peaked at a record US$1.45 trillion.

But now things are returning to earth, and the stock is down 31% from those highs to near where it left off.

Source: TradingView

[Click to open in a new window]

I would make some pithy remark about ‘what must go up…’ or gravity but it’s still too early to guess the company’s future.

Looking ahead, behind it sit two more giants. Anthropic, the maker of Claude, filed confidentially this month at a valuation around US$965 billion. OpenAI followed days later, valued somewhere between US$850 billion and US$1 trillion.

Together, the three are asking markets for more than US$200 billion in fresh capital.

The combined price tag approaches US$3.6 trillion. That is roughly the size of the French economy, packed into three businesses that have yet to turn a profit.

Wall Street has welcomed them warmly, and not without reason. The market today is far larger and deeper than in past cycles and company earnings are still very positive.

But as an unreformed pessimist, I’m always looking for the other half of the glass.

Why the Biggest Floats Worry Me

The largest offerings in market history have a habit of arriving near important turns.

The pattern is no accident. Founders and early backers tend to sell when buyers are most willing to pay, and that willingness peaks when confidence runs hottest.

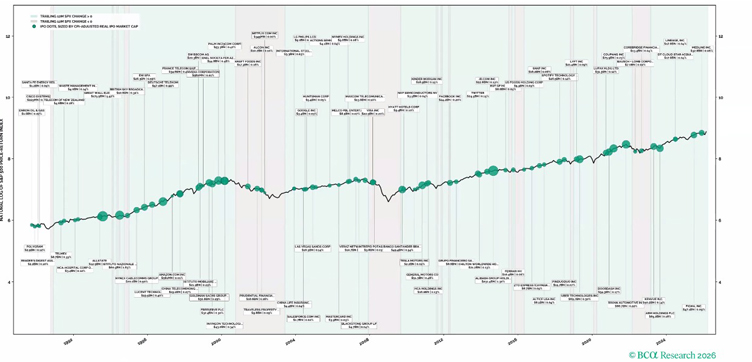

Looking below we can see some of the largest IPOs by the size of green circles, on a log-scale S&P500. You can see that many of the biggest IPOs coincide with either the beginning, or the end of a recession (in red).

Source: BCA Research

[Click to open in a new window]

Considering where we are in the cycle, that’s room for concern.

Here are some historical examples that underscore my point.

In 1901 J.P. Morgan floated US Steel as the first billion-dollar company in history, the SpaceX of its day. Within two years the Dow had fallen by half.

A similar story for Radio Corporation of America who IPOd in 1919 before the 1920s crash. Through the roaring 20s it became one of the central speculative punts of the decade. It didn’t survive the great crash of 1929.

Ford came to market in 1956, right as the Dow pushed above 500 for the first time. Sentiment was about as buoyant as it had been since the roaring ‘20s.

Its IPO was at scale previously unfathomable. In fact, the deal was so large that nearly every stock on Wall Street was part of the underwriting, over 200 in all.

Within 18-months came the so-called ‘Eisenhower recession’ a period where new car sales fell 30%, their sharpest since the war.

Blackstone floated in mid-2007, just as the credit boom that built it began to crack.

Glencore followed in 2011, at the high-water mark of the commodity cycle. Coinbase and Rivian both listed in 2021, within months of the peak that gave way to the 2022 bear market.

An Echo of 2000

You’ve probably already caught on to the pattern, but there’s one last example.

The late 1990s offer the clearest parallel to now. IPOs poured into the market as the dot-com mania built, and insiders rushed to cash in.

Palm went public in early 2000, just as the Nasdaq topped. You probably don’t remember Palm, but at one point it was worth more than Apple, Nvidia, Amazon and Starbucks combined.

Its early consumer electronics were essentially the early smartphone, but its impact is not one of products, but of lessons.

Source: Ebay

Palm’s legacy is now in lecture theatres at universities, where the company’s IPO is taught as a cautionary tale of easy money chasing questionable returns and market mania.

Palm lost 90% of its value within a year and ten years later HP bought the stock for 2% of its day-one peak.

The drop that came after its lock-up period ended (the time after you can sell your stock) is the stuff of legends. Some even point to it as a catalyst for the crash.

But it wasn’t alone, the lock-up periods for many of those final IPO listings expired between October 1999 and April 2000, almost exactly as the bubble peaked.

Now SpaceX has smartly staggered its lock-up so there is no one single cliff for us to point to. But around 20–30% will be unlocked after its earnings in early August.

Now as this week’s shown, valuation concerns are creeping in.

The Era of Mega-Floats

The deeper problem is arithmetic. Most new listings disappoint.

In most years since 1980, the typical newly floated firm has trailed the wider market over the following three years.

Those winners grow harder to find at this size. Amazon has risen more than 26,000% since its 1997 debut.

For SpaceX to deliver the same from here, its value would need to swell beyond six times every listed company in America combined.

The bigger the float, the less room remains for legendary returns.

None of this is a forecast of collapse.

By deal count, this year’s roughly fifty US listings are close to average. A long way from the hype-era 250 floats of 2021, or the 400 of 1999.

Broadly the market can keep climbing from here, and it probably will for a while yet. Earnings are still growing, and none of this means you need to panic sell.

But history is offering a warning worth heeding. When the largest and most celebrated names rush to sell to the public at once, the wiser course is caution rather than chase.

The Boring Trade

Right now, the ASX barely rates a mention. People are unhappy with the government’s economic direction and things slowly chug along in our market.

But we may be the turtle in the race.

Steady dividend payers, established miners and unglamorous industrials seldom make headlines. But they also seldom make the violent losses that follow a popped mania either.

When the dot-com darlings unwound in 2000, it was the dull old-economy names that held their ground while the hot stocks halved and halved again. That pattern has a habit of repeating.

So the unfashionable, slightly dull domestic position deserves a second look.

It will not light up a dinner party. But with so much priced for perfection overseas, quietly owning the steady trades closer to home is a long way from the dumbest play you can make.

Regards,

Charlie Ormond,

ATLAS and Altucher’s Investment Network Australia

Comments