Building product manufacturer CSR [ASX:CSR] has announced today that it has entered into an agreement to acquire its long-standing customer Woven Image for $43 million.

Shares were flat this morning on the news and down slightly this afternoon, trading at $5.26 per share, which is a 0.66% drop today.

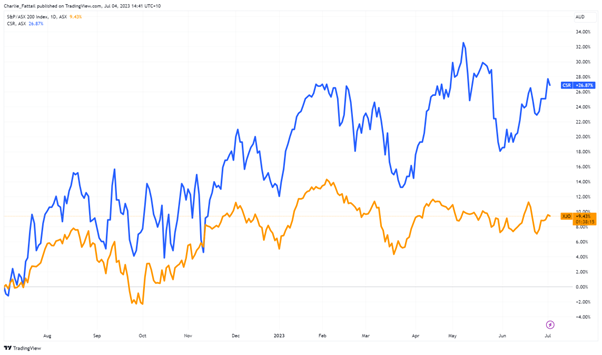

CSR’s share price has bucked the trend of the wider industry in the past 12 months, with shares up 27% — 8.6% better performance than the wider sector. Construction manufacturing has struggled with the explosion of input and labour costs from inflationary pressures, as well as a wider construction slowdown.

What does this latest potential acquisition mean for the company moving forward?

Source: TradingView

CSR acquisition broadens commercial range

CSR today announced that it penned a deal with Woven Image to buy the acoustic finishes and textile company for $43 million. The acquisition is subject to conditions and will be earnings accretive if completed in the coming months.

Woven Image has operated since 1987, supplying sustainable, design-led acoustic finishes and textiles. Woven Image products are extensively used in global commercial projects across workplace, hospitality, education, and healthcare sectors — ensuring spaces have aesthetically pleasing surfaces that dampen sound.

CSR has a long-standing customer relationship with Woven Image and has manufactured some of its product range for 20 years.

CSR Managing Director and CEO Julie Coates commented on today’s deal, remarking:

‘The acquisition of Woven Image positions our interior systems business for further growth both domestically and in export markets and follows the move to full ownership of Martini in 2020. The commercial interior finishes segment is a highly attractive market and provides further opportunity for growth and diversification across product, building sector and geography.’

The external positivity is slightly undercut by bearish signals internally.

In the last three months, we’ve seen notably more insider selling than insider buying at CSR.

In total, CEO, MD & Executive Director Julie Coates sold AU$556,000 worth of shares in that time. In contrast, insiders spent AU$159,000 on purchasing shares.

Generally, this level of selling might be considered a bit bearish. Also announced because of the agreement, CSR’s on-market share buyback announced in June 2022 will conclude in July 2023.

What this means for CSR

The deal may be the first positive news from the company since its disappointing earnings for FY22 reported net income was down approximately $52 million year-on-year at $218.5 million.

With inflation leaning on input costs for the building manufacturing company, it’s no great surprise that revenues have lagged as they pass that onto the construction industry, which has taken the brunt of the pain — with construction industry revenues down $5.4 billion (9.3%) in the 2021/22 financial year.

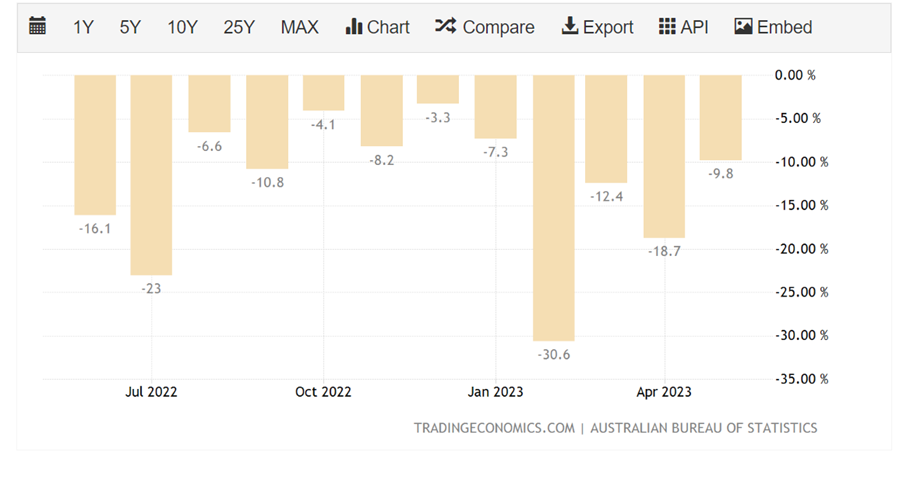

More recent data, shown below, also highlights the scale of the problem with a steep drop-off of new building permits often seen as a leading indicator for pain in construction manufacturing and the economy more widely.

Source: Trading Economics

On a more micro-focused lens, the deal is a great match for CSRs current commercial range and will play into the successful strategy CSR has often employed in widening its product base to remain relevant.

Woven Image is highly complementary to CSR’s existing commercial interior ranges, and the acquisition will enhance CSR’s commercial interior finishes offering in the Australian market and exports to Europe and Asia.

The combined product range, with a renewed focus on sustainability and new design-led manufacturing capability, positions the business to better serve shareholders and deliver further growth in Australia and export markets.

The acquisition is still subject to regulatory approval, but it is expected to close later this year. Once the acquisition is complete, CSR will begin integrating Woven Image into its operations.

This will include combining the two companies’ product ranges, sales and distribution channels, and manufacturing capabilities. CSR expects the acquisition to be earnings accretive in the first full year of ownership.

For investors, the dividend yield is currently at a healthy 6.9% but is expected to drop in the near future as market uncertainty grows.

So where can investors look for dividends in today’s markets?

The great yield chase

Investors are flocking to income stocks as inflation soars and stock prices fall.

But not all income stocks are created equal.

In our latest report, Greg Canavan reveals his ‘Royal Dividend Portfolio’ of six stocks that offer the potential for both high yields and capital growth.

Greg thinks that these stocks are undervalued and could bounce back in price soon.

He also believes that they offer a better income strategy than pure growth stocks or cash in the bank.

If you’re looking for a way to protect your wealth from inflation and generate income, Greg’s Royal Dividend Portfolio is worth considering.

Regards,

Charles Ormond,

For Money Morning