So the old ‘one trillion-dollar coin’ idea is doing the rounds again.

In case you hadn’t heard, this is the idea of minting a one-off ‘US$1 trillion’ coin.

This coin would then be used to pay down US Government debt and avoid defaulting on their loans as they approach the imminent debt ceiling.

If that sounds nuts, that’s because it is.

But it’s perfectly legal.

You see, it takes advantage of a loophole that allows sitting US presidents to issue commemorative coins at their sole discretion.

Usually, these are collectable coins worth $10 or $20 to mark a special occasion or notable person.

But nothing in the rules says what the maximum value of these commemorative coins can be.

Anyway, part of me hopes they go for it.

It’ll expose the sham that our current monetary system is once and for all.

Think about it…

You slave away for 40-plus years to save what you can, make sacrifices, and try to build wealth for your retirement.

Meanwhile, these jokers can issue virtually unlimited amounts of money at will to benefit whoever they want.

What a con!

This time around, the trillion-dollar coin idea was floated by Nobel Prize economist Paul Krugman.

You know the one.

He’s that guy who said back in the 90s that the internet would have no more impact than the fax machine.

Anyway, he explained why this blatant money printing wouldn’t cause more inflation:

‘The Fed would surely sterilize any impact on the monetary base by selling off some of its huge portfolio of US debt,’

These sleight of hand bookkeeping tricks would even make a shonky backstreet accountant blush.

And they call Bitcoin [BTC] ‘make-believe’ money!

Anyway, the reason that such ‘crazy’ ideas are back in the public arena is the continuing US banking crisis and the fast-approaching government debt ceiling.

Simply put, the powers that be need a new way to create money from thin air. Or, more accurately, a new way to pull the wool over our collective eyes.

Because despite assurances that everything is ‘resilient and safe’, the bond market is saying otherwise…

The end of regional banks is nigh

With First Republic now gone, everyone is looking to see which bank fails next.

There are more than a few contenders.

Check out the stock market action last Thursday:

|

|

| Source: Kobeissi Letter |

The regional banks staged something of a recovery on Friday. Mainly due to rumours the US government would ban short selling of them in an effort to halt the savage share price slides.

So a bunch of traders who were betting on prices going lower had to buy back in to lock in their profits — just in case.

But I expect this move higher to be a short-term thing, because the issues aren’t going away any time soon.

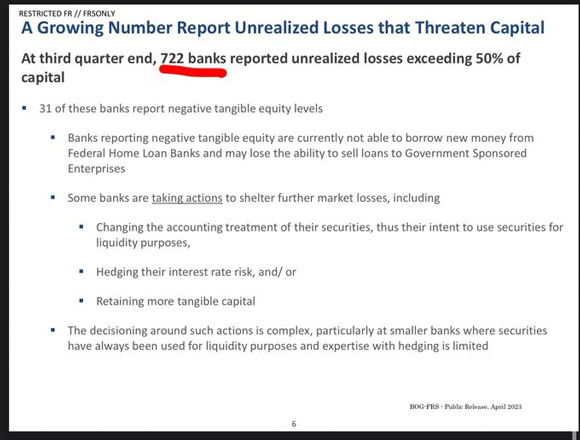

Indeed, one of the Federal Reserve’s own internal reports noted that 722 banks had unrealised losses exceeding 50% of their capital:

|

|

| Source: Federal Reserve |

The potential value destruction coming is enormous.

And PacWest looks odds on to be the next bank to go under. That bank was worth US$5 billion earlier this year and is now worth just US$400 million.

Incidentally, I came across a tweet that once again shows how rigged this game is:

|

|

| Source: Twitter |

As per usual, the connected elite never pay the bill when the financial system crumbles.

Now, some are saying that the failure of small banks is actually part of a wider plan. The idea is that a US banking system with just a few big banks is a lot easier to control.

Here’s the thing…

While they go around pretending to be bastions of capitalism, big banks are usually the biggest political cronies out there.

And it was none other than the Godfather of communism, Soviet leader Vladimir Lenin who said:

‘Without big banks, socialism would be impossible. The big banks are the “state apparatus” which we need to bring about socialism.’

Maybe this is ‘conspiracy’ thinking.

But whether it’s the intention or just an unexpected outcome, it’s a dangerous situation nonetheless.

Anyway, as this regional banking bloodbath plays out, the big question is if the Fed steps in before it becomes a rout?

The bond market thinks they will have to.

And very soon…

Rate cuts this year

Check out this chart:

|

|

| Source: Eurodollar University |

Despite the fact central banks in the US, Europe, and Australia all raised rates this week, markets are starting to price cuts by as early as June!

This chart shows it more clearly:

|

|

| Source: Eurodollar University |

The black line shows bond markets expect interest rate cuts to be drastic over the next two years, falling in rapid order.

This is a strong signal of imminent economic calamity.

And yet…

Stock markets continue to hold up fairly well right now.

Indeed, the benchmark US index, the S&P 500, rose 1.4% over April, building on the 7% gains from the first quarter.

Is this just the calm before the storm then?

It could be…

And I think there’s a slim chance we see a 1987-esque rug pull situation.

A swift and rapid decline in markets, like what happened on Black Monday.

On that infamous Monday, 19 October 1987, stock markets around the world unexpectedly crashed.

Eight major markets, including the US and the UK, fell by between 20% and 29% in just one day.

The Aussie market fell by more than 40%!

But as I said before, despite all this negativity, stock markets are holding up very well.

Right now, I think the stock market is reading cues from the bond market and assuming interest rate cuts and liquidity will come back in before the economy collapses.

We know that liquidity is the single-biggest driver of stock market returns, so in a way this makes sense.

But what if central bankers don’t play ball?

What if they’re willing to sacrifice markets and the economy in the short term to kill inflation?

The next big short

99-year-old Charlie Munger said last week that US banks are packed with ‘bad loans’ that will be vulnerable as ‘bad times come’ and property prices fall.

Commercial real estate is the big worry.

As reported in CNN, Blackstone’s recent results are causing investor angst:

‘The ongoing commercial real estate slowdown has a new victim: Blackstone, the largest owner of commercial real estate globally. The company saw its distributable earnings — the profit distributed to shareholders after expenses — plunge 36% since last year.’

And an article in the AFR last week called commercial real estate the next ‘Big Short’.

‘…there’s a bit of a Big Short moment in the US commercial mortgage-backed securities market. In 2008 contrarian traders shorted a newly created ABX index of leveraged securitised mortgages to bet on doom in the housing market.

‘In 2023, the CMBX index of 25 bonds tied to commercial real estate is the contract of speculation.

‘The BBB tranche has collapsed in price from 82 cents in the dollar at the start of the year to the low 60s. That is implying that a large swath of office assets will be impaired, and that cost and access of real estate debt must rise.’

While the current crisis isn’t a credit crisis yet, it could turn into one very quickly.

Right now, the markets are saying central banks blink first. If they do, then the stock market could indeed have bottomed out.

But if they hold the line on fighting inflation and keep rates higher for longer, as they’re saying they will, even as the financial system falls apart…then look out below!

It’s going to be an interesting few months ahead.

Make sure you have a plan for any scenario, and keep risk management front of mind.

Good investing,

|

Ryan Dinse,

Editor, Money Morning

The price of bitcoin is on the rise. Indeed, along with gold — which is close to record highs — it’s acting as something of a safe haven from the banking crisis.

On that note, I’ll be writing a special guest piece in the Daily Reckoning tomorrow. It will counter some of the common criticisms you might’ve heard. I’ll also lay down the positive case for including an allocation to bitcoin as part of your overall portfolio. If I’m right, we’re close to a breakout moment for bitcoin. Make sure you catch that by clicking here.