Have you made any big purchases lately? Or browsed the shopping centre with the intention of buying something nice?

If you haven’t, you’re not alone.

Consumers are cutting back…and retailers are feeling it.

In his speech in June, Reserve Bank governor Philip Lowe admitted retail spending on goods ‘has been weak’.

According to the Australian Bureau of Statistics, retail turnover has ‘plateaued over the last six months as consumers spent less on discretionary goods in response to cost-of-living pressures and rising interest rates.’

That’s unsurprising…and something Greg Canavan and I covered in the latest episode of What’s Not Priced In. You can check it out below if you’re interested.

ASX retail stocks downgrade earnings

All retailers are under the pump in 2023 as the Reserve Bank hiked interest rates at the fastest pace in decades.

Some have even folded.

Beauty retailer BWX [ASX:BWX] entered voluntary administration in April this year.

And just today, value apparel retailer Best & Less Group Holdings [ASX:BST] said ‘trading conditions have continued to soften, with sales and foot traffic lagging the prior year’.

In the five trading weeks from 15 May to 18 June, Best & Less saw total sales fall 12% below the prior corresponding period and like-for-like sales fall 13%.

The continued promotional and discount activity to clear stock and ‘right-size’ inventory for softening demand crunched BST’s margins.

The retailer now expects 2H23 net profit after tax of between $3.6 and $4.2 million, down substantially from previous guidance of $10–12 million.

Ouch!

Best & Less isn’t an outlier.

Baby goods retailer Baby Bunting Group [ASX:BBN] cut its guidance earlier this month, too, following Adairs [ASX:ADH], and Universal Store Holdings [ASX:UNI].

The downgrades and euphemisms of ‘softening’ demand have translated to steep share price declines.

ASX retail stocks by the numbers

Falling sales and rising financial unease among the average consumer has spooked investors and analysts alike.

Look at the recent performance of a few retail stocks (Greg Canavan compiled this in his latest monthly edition of Fat Tail Investment Advisory):

Premier Investments [ASX:PMV]: Down 25% since February

Harvey Norman Holdings [ASX:HVN]: 28% since late January

Beacon Lighting Group [ASX:BLX]: 40% since late January

Myer Holdings [ASX:MYR]: 45% since March

Adairs [ASX:ADH]: 50% since early February

Lovisa Holdings [ASX:LOV]: More than 30% since April

Accent Group [ASX:AX1]: Nearly 40% since April

Super Retail Group [ASX:SUL]: 20% since April

Shaver Shop Group [ASX:SHH]: More than 20% since February

Nick Scali [ASX:NCK]: More than 30% since February

JB Hi-Fi [ASX:JBH]: 15% since January

You can throw Best & Less, City Chic Collective [ASX:CCX], and Dusk Group [ASX:DSK] in the mix, too.

City Chic is down by 55% since mid-January.

Best & Less is down by 10% since January (but will fall more after today, I think).

And Dusk is down by 55% since mid-January.

The steep falls coincide with big earnings revisions from analysts.

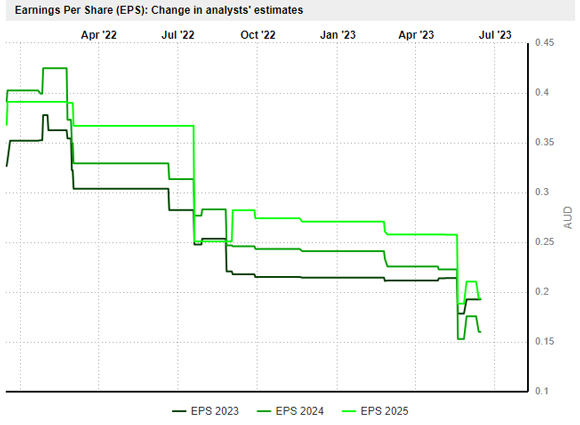

Take Dusk, the home fragrance retailer.

|

|

| Source: Marketscreener |

Huge revisions.

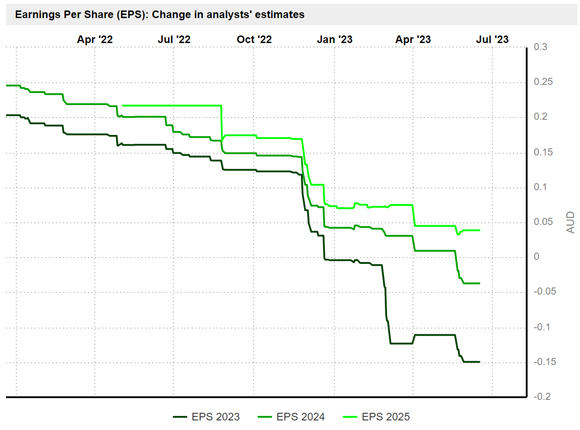

And here’s the same for City Chic.

|

|

| Source: Marketscreener |

Mass rerating from market analysts.

The question is, do the revisions herald a bottom or can these stocks surprise further to the downside?

Best & Less serves as a cautionary tale.

It was only in mid-May that the retailer made the now downgraded 2H23 profit guidance of between $10–12 million.

BST executive chair said in the May update:

‘While trading conditions have remained inconsistent as consumer confidence has been at historic lows, we had a strong Mother’s Day. With the Federal budget expected to provide some much-needed relief for our core customers and a further four new stores due to open before the end of the calendar year, we are optimistic about the outlook for sales growth. We expect to see the benefits of lower product and shipping costs begin to flow through in the first half of FY24 and we will remain focused on tightly controlling our cost base to preserve profitability.’

Clearly, management was surprised by how quickly conditions deteriorated.

The worry is other retailers may have similarly underestimated the hit to sales and, consequently, analyst earnings revisions can fall further.

After all, things will only get worse for the Aussie consumer in the coming weeks.

As Greg pointed out in the podcast, a huge swathe of fixed mortgages will reset in the September quarter (only a few weeks away).

|

|

| Source: Australian Financial Review |

So, has the worst been priced in? Or is there more pain yet for retail stocks?

Retail stocks seem attractive at current prices.

For instance, Dusk is trading at a trailing P/E of just 3.5, Best & Less at 7.9, and Shaver Shop at 7.2.

But are these bargains or traps?

Well, usually when a stock is trading at low multiples, the market judges the quality and sustainability of those earnings.

A low trailing P/E ratio indicates the market thinks future earnings will take a hit.

But it could also suggest the market is missing something.

In his great book on valuation, Greg wrote:

‘When the market isn’t prepared to pay much for future earnings (reflected in a low P/E), it either tells you those earnings are unachievable, or that the market is simply missing the opportunity.

‘The market often misses opportunities when a stock has been through a tough period. In this situation, investors get frustrated and impatient. They sell and look elsewhere. This is where psychology comes into play. A stock in this scenario simply falls off the radar. If you can get into these situations early, you stand to make good returns before the crowd notices and gets on the bandwagon again. As I discussed earlier, it is investor psychology that creates underand over-valuation. If you can get in during the undervaluation phase and sell during the overvaluation phase, you’ll go a long way towards outperforming the market.’

So, what’s Greg thinking about retail stocks?

In a recent note, he wrote that value is emerging in the sector, but one must be patient:

‘Value is starting to emerge in the sector. But there are likely to be profit downgrades ahead. So it’s too early to move in and buy, and share prices are in clear downtrends.

‘Hanging over the sector’s head is the fact that there is a significant number of fixed rate mortgages due to reset this year.

‘But just keep in mind there will be plenty of bargains on offer later this year.’

Luxury retailers to fare better?

What about luxury retailers? Can they buck the trend?

In late May, RBA’s Lowe fronted the Senate to field questions on a range of topics. In one of his answers, he admitted low-income earners were retrenching the most (emphasis added):

‘But it’s pretty clear from the transaction account spending data that for people who borrowed a lot and borrowed a lot recently—that is, in the last three years—their spending is growing much more slowly than for the rest of us. And in areas where there are a lot of low-income renters those people are having to cut back more. That assessment from the banks is corroborated from our liaison with the retailers, who say that in their shops in locations where there’s lower income or a lot of first home owners spending is slowing more.’

Those on lower income are slowing their purchases. But are those with a high net-worth still splurging?

Consider the luxury retailer Cettire [ASX:CTT].

The stock is up ~70% year to date and up by more than 400% in the past year!

In its latest trading update for the four-month period ending 30 April, Cettire said sales grew 122% to $141.3 million.

It reminds me of what Ryan Dinse wrote about yesterday, when he said:

‘Even in recessions, people still spend money.

‘Working out who is relatively immune from any economic downturn and where they will spend is a great strategy to keep you focused on what really matters in investing.’

We’ll see whether luxury retailers continue to grow sales in these tougher economic times, but Ryan’s point stands regardless.

Best,

|

Kiryll Prakapenka,

Editor, Money Morning