Preparation is the key to success.

Answering the complex question of ‘how safe is my money in the bank?’ is all about preparing us to successfully navigate the risks posed to our cash from the next and far more destructive global financial crisis.

The majority of people are either blissfully unaware of or dismiss the prospect of another (and more severe) credit crisis. This thinking (or lack of thinking) baffles me.

Since 2008, the world has managed to go US$200 trillion — yes, trillion — deeper into debt.

Believing you can solve a debt crisis with more debt is an utterly nonsensical proposition. If we’re going to believe in the unbelievable, why not cure emphysema by smoking more?

When the markets and the economy are shaken to their senses, you can expect fairly nasty repercussions.

As outlined in the two previous articles, the world does NOT come to a grinding halt.

However, the global economy is geared toward growth, so a marked slowdown in economic activity will impact the very heart of the system…the banking sector.

In late 2008, to restore confidence in our banking sector, the Australian Government legislated into existence the Financial Claims Scheme.

What APRA and the Budget Papers tell us…something doesn’t quite add up

For those of us who need to get a life, have you ever wondered how much money is on deposit with Australian banks?

The exact figure — as at 31 December 2022 — is $2,824,107,000,000.

For the ease of this exercise, let’s call it $2.8 trillion.

How do I know this?

The Australian Prudential Regulation Authority (APRA) publish a monthly report titled ‘Monthly Banking Statistics’.

The report — for January 2023 — was released on 28 February 2023.

Table 4 from the Excel spreadsheet tallies all the deposits held on the books of Australian banks.

From the list of 125 Authorised Deposit-taking Institutions (ADIs), there are nine holding the ‘lion’s share’ of deposits:

|

|

**NOTE: If the ANZ acquisition of Suncorp is given the green light, then Suncorp Bank will no longer be its own ADI…it’ll be under ANZ Bank’s ADI status.

What this means is if you currently have $200k with Suncorp and $200k with ANZ, the whole $400k at present is covered under the Government’s Deposit Guarantee. However, if the acquisition proceeds, then only $250k of the $400k will be covered. An important detail to be aware of.

OK, back to the table.

With the top nine ADIs holding $2,458 billion, it means 116 ADIs are custodians for the remaining $342 billion.

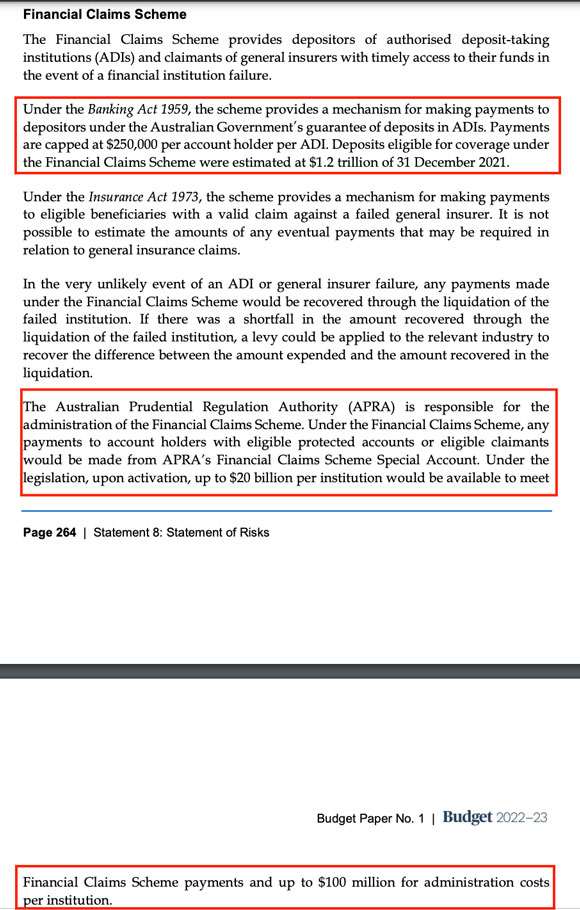

The reason why this is important can be found the Australian Government Budget 2022–23 papers on page 264…in the section titled ‘Statement of Risks’.

Here’s a screenshot, with the relevant paragraphs highlighted:

|

|

| Source: Australian Government |

Concerns over whether the government will honour its guarantee should be laid to rest by the statement contained in the highlighted second paragraph.

However, I can understand why there are doubts because the numbers quoted in the Budget Papers DO NOT add up (emphasis added):

‘Deposits eligible for coverage under the Financial Claims Scheme were estimated to be $1.2 trillion as of 31 December 2021.

‘Under the legislation, upon activation, up to $20 billion per institution would be available to meet Financial Claims Scheme payments and up to $100 million for administration costs per institution.’

OK, here’s what we know.

Total deposits held by ADIs is $2.8 trillion.

Due to the Financial Claims Scheme limiting the guarantee to $250k per tax paying entity per ADI, the government is not on the ‘hook’ for the whole $2.8 trillion.

By its budget estimate, the deposits eligible for coverage under the Financial Claims Scheme were estimated to be $1.2 trillion.

However, the budget papers state ‘upon activation, up to $20 billion per institution would be available to meet Financial Claims Scheme payments’.

Let’s do some simple maths:

According to APRA, there are 125 ADIs covered by the Financial Claims Scheme:

- 116 of these have deposits totaling around $342 billion.

- With regards to the remaining nine, the guarantee is limited to $20 billion per institution. Which means a total potential liability of $180 billion (nine x $20 bn).

When you do the maths, the government liability should be no greater than $522 billion (and, in practice, should be a little lower because there are bound to be deposits in excess of $250k in some of the smaller ADIs).

Yet, the budget papers state there’s $1.2 trillion in deposits covered by the guarantee.

Is this a bureaucratic error OR is the government (in the fine print) signalling that, if required, it’s prepared to legislate an increase to the $20 billion cap per institution?

My guess is, it’s the latter.

Why?

Society functions on public confidence.

Without it, the economy will suffer an even greater slowdown…as we saw in the US prior to the introduction of the Federal Deposit Insurance Corporation (FDIC) in 1933.

The 7/87 rule

We’ve all heard of the 80/20 rule, but in the case of the Australian financial system, it’s the 7/87 rule.

7% of the institutions have 87% of the deposits.

The concentration of deposits in so few institutions means the government — in practical terms — has no choice other than to backstop the nine larger banks.

Allowing one or more of these nine banks to fail is not an option. Public confidence would be shattered. People would start second-guessing which major bank is next. A run on the banks would become a self-fulfilling prophecy.

What if one of the smaller ADIs runs into trouble?

After exhausting all avenues to recapitalise the bank, would they confiscate (some or all) of the deposits in excess of the $250k limit?

According to the letter of the legislation, yes they could.

But what signal would that send to deposit-holders in other banks?

Watch out…you could be next.

Imagine the frantic switching of accounts out of the banking minnows into the Big 9? The loss of deposits in smaller ADIs would almost certainly trigger further bank failures.

Before acting, authorities would need to seriously consider Merton’s Law of Unintended Consequences…making a bad situation worse would be a really dumb move in a time of heightened anxiety. My guess is APRA would work behind the scenes to orchestrate merger/s.

Should one of the Big 9 fail, authorities might start with bail-ins from shareholders and investors in hybrids.

Confiscating investor capital — either fully or partially — to recapitalise the ailing bank/s would be perfectly acceptable to the general public.

If that’s not sufficient, then prior to APRA seizing deposits greater than $250k, other options might be:

Facilitating mergers between the Big 9.

Capital controls could be invoked (to stop bank runs).

Or, thanks to the precedent established during the pandemic, the government could roll out a ‘Bank Keeper’ program and have the RBA print sufficient funds to finance an expanded deposit guarantee scheme.

There are a variety of measures the authorities have at their disposal to (potentially) quell public anxiety and unrest.

With 87% of deposits held in nine banks, it’s unlikely the government would allow any of them to fail. The risk of contagion would be far too great.

Before taking any action, the government needs to act very, very carefully…public confidence is a brittle commodity. Easily broken, but not so easily restored.

While, when push comes to shove, I’m of the opinion bail-ins are unlikely, the fact is you can only make decisions on the known public facts.

Government WILL honour its guarantee promise…up to $250k per tax paying entity per ADI.

If you invest your cash/term deposit holdings according to the government’s stated guarantee criteria, then 100% of your capital will be secure AND if the RBA keeps cranking up rates, you’ll be paid 4–5% for your trouble-free efforts.

To me, this sounds like the best Risk versus Reward proposition on offer in the current hazardous market conditions.

Regards,

|

Vern Gowdie,

Editor, The Daily Reckoning Australia