Today, we continue with our top trends for 2022 as part of our ongoing series, “Our Top Nine Investment Trends to Watch in 2022”

In this series we are going to cover our top 9 investment ideas:

1. The great lithium disconnect

2. Decarbonisation — green switch activated

3. The future of payments

4. Quantum computing and Moore’s Law on steroids

5. Connected devices and memory

6. Decentralised finance — an ‘Amazon-in-1994’ moment

7. The influential Is

8. Watch out for gold

9. Stocks – Mind the lofty valuations

If you’re interested in dowload all 9 Trends in one document to read at your leisure, simply enter your email below and have them sent directly to your inbox.

And this time, we’re talking about…

Trend #9 Mind the lofty valuations

Despite Omicron, rising inflation, and growing talk of interest rates hikes, the stock market continued to rise in 2021.

And on the first trading day of 2022, the Australian share market climbed to fresh peaks, with the All Ordinaries Index reaching a record high of 7,931.

The previous high was passed in August 2021.

The bellwether US market also enjoyed a record year in 2021, riding high despite the wider macroeconomic concerns.

Wall Street’s main indices ended 2021 with monthly, quarterly, and annual gains, recording their biggest three-year advance since all the way back in 1999.

Source: TradingView.com

But have the valuations climbed too high? Should investors be worried about the altitude?

In late December 2021, Morgan Stanley strategists came out and said the US S&P 500 Index could decline 5% in 2022.

The investment bank’s brains trust recommended ‘underweighting US stocks to account for high valuations and more catch-up potential and less volatility elsewhere in the world’.

Morgan Stanley wasn’t the only one wary of the recent stock market highs.

As Bloomberg reported on 3 January 2022:

‘Part of the issue is that valuations are elevated “for all major asset classes relative to history,” according to Goldman Sachs. That feeds into the “less of the same” mantra coined by Pictet Asset Management. When everything already looks expensive, the expected upside is smaller. Single-digit stock returns are the broad consensus. ’

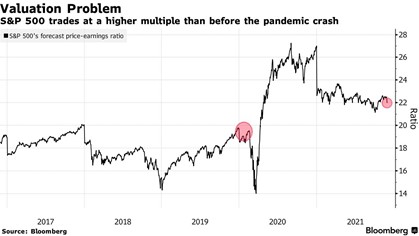

Signs valuations are stretched abound.

Source: Bloomberg

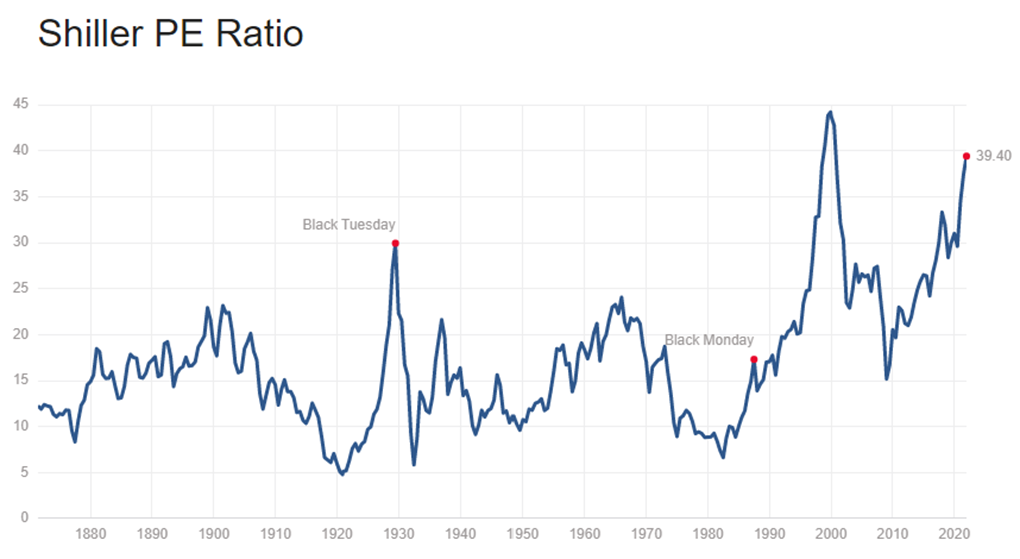

As Robert Shiller, the Nobel Prize laureate economist and author of Irrational Exuberance pointed out, stock valuations are elevated compared to historical averages.

Shiller’s widely used measure of stock valuations, the cyclically-adjusted price earnings (CAPE) ratio, has been hovering in rare territory.

Only once, during the late 1990s dotcom bubble, has the S&P 500 traded on a CAPE ratio of 40 or above.

Source: Multpl.com

Shiller’s index can’t predict short-term market movements, of course.

But like other valuation measures, it suggests stock market returns are ripe for a mean reversion in the next decade.

One of the world’s largest investment companies, Vanguard, projects that the US stock market will produce annualised returns of only 2.4–4.4% for the next decade, with current high prices likely contributing.

And what moves US equities is likely to spill over to local markets like the ASX.

The heady state of equities has one of our long-standing editors worried.

Vern Gowdie is a veteran of the finance industry and heads The Gowdie Letter.

Over the course of 2021, Vern has seen a systemic risk building that could swallow the financial world.

As he wrote in a recent detailed report:

‘Markets move in cycles.

‘Yet we tend to look at them, as we do life, in linear fashion.

‘We think the immediate future will be the same as our recent past.

‘And our past has been up, up, up.

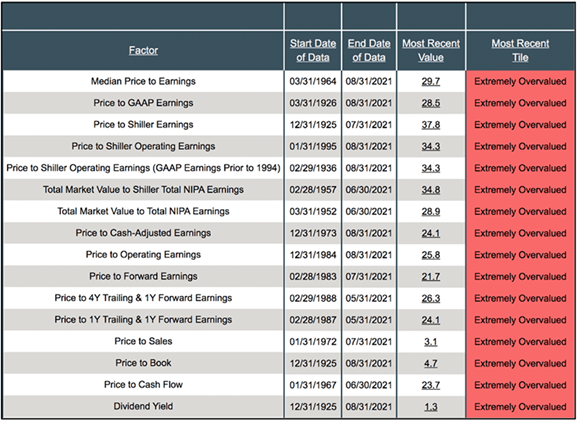

‘This is the stock market right now…

Source: Ned Davis Research

‘Every valuation metric flashing red.

‘But, unlike other bubbles, this is not just a stock phenomenon.

‘It’s ALL assets.

‘And very few people think it will end any time soon…or in any meaningful or harmful way.

‘I think these people are gravely mistaken

‘A “Code Red” is a term used by the military, medical professionals, emergency services, and even climate scientists.

‘When a situation escalates to a Code Red, the public is alerted to the dangers we face. And told how to prepare for the probable eventuality.

‘Yet, when it comes to markets, no such alarms are being raised.

‘Not by government. Not by mainstream media. And not by financial advisors.’

But Vern is.

If you want to read his ‘Code Red’ report to find out more about the alarms Vern thinks the markets are sending, you can access it here.

But Vern isn’t the only one sounding the alarm.

In November 2021, respected market analyst Alasdair Nairn published his latest book, The Everything Bubble.

Nairn isn’t a permabear or a curmudgeon.

His other book, Engines That Move Markets, was hailed by well-known Tiger Cub Philippe Laffont, founder of US$45 billion tech hedge fund Coatue Management, as the best book on growth investing he’d ever read.

It’s always insightful to read what the hedge fund movers and shakers are reading and learning.

So what did Nairn say in The Everything Bubble?

Here’s a choice snippet:

‘What is distinctive, indeed unique, this time round is that we are witnessing an explosive growth of debt and excessive speculation across almost the entire universe of investable assets, not just in some particular sectors.

‘The traditional defensive asset to which investors flee during rises is government bonds, but the bond market is at the epicentre of the looming crisis. With government borrowing at record peacetime levels and bond yields not far above zero, that traditional safety net is no longer there.

‘The root causes of periods of financial market excess are clearly many and varied, but in most instances low interest rates are one of the key factors underpinning asset-price inflation. Low interest rates are a common denominator in market bubbles and all too often cheap money, as we have seen, is the result of deliberate, but misguided and short-sighted, policymaking.

‘Is it the same this time? The answer is clearly yes. At the heart of the problem today is not just the fact that money has never been so cheap, but that policymakers, in both governments and central banks, have left themselves with little or no room to manoeuvre out of the trap they have set themselves by deliberately keeping the cost of money so low for so long.’

And there’s also Michael Burry, the investor immortalised in The Big Short for betting against the housing bubble during the 2008 financial crisis.

What’s Michael Burry’s assessment of current market conditions? Here’s a recent series of tweets Burry published in 2021.

‘People always ask me what is going on in the markets. It is simple. Greatest Speculative Bubble of All Time in All Things. By two orders of magnitude. #FlyingPigs360.’

‘All hype/speculation is doing is drawing in retail before the mother of all crashes. #FOMO Parabolas don’t resolve sideways; When crypto falls from trillions, or meme stocks fall from tens of billions, #MainStreet losses will approach the size of countries. History ain’t changed.’

‘The problem with #Crypto, as in most things, is the leverage. If you don’t know how much leverage is in crypto, you don’t know anything about crypto, no matter how much else you think you know.’ Greatest speculative bubble of all time in all things.’

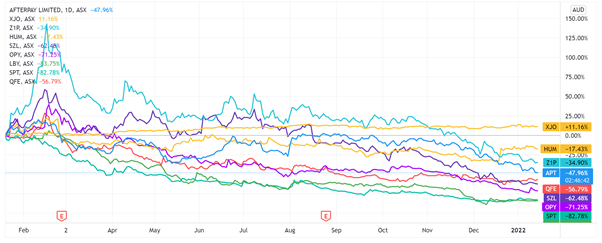

ASX BNPL — the first bubble to pop?

If you had to pick a sector likely to have fundamentals removed from valuation, the ASX buy now, pay later (BNPL) sector would be a prime candidate.

At the end of 2020 and beginning of 2021, the local BNPL sector was booming. And market leader Afterpay hit an all-time high of $160 a share on a FY20 net loss of $22.8 million.

But the shine wore off…

Source: TradingView

All the major ASX BNPL stocks like Afterpay, Zip, Sezzle, and Splitit have well underperformed the ASX 200 benchmark in 2021.

In the middle of January 2022, Afterpay — once the ASX darling — was down over 55% from its all-time peak.

Zip, Afterpay’s closest rival, was down 75% from its all-time high.

***

So are we entering the mother of all bubbles? Should we run for the exits? Or are the fears overblown?

Of course, you’ll have to make up your own mind (nonetheless, I recommend reading Vern’s ‘Code Red’ report as part of your background research).

But bubble or not, I think the points raised by the likes of Vern and Alasdair Nairn serve as useful reminders to take stock, zoom out, and reflect.

It never hurts to ask yourself questions like ‘Are valuations too high?’, ‘Am I comfortable with the risks?’, and ‘Should I reassess my strategy and positions?’.

Conclusion: the more things change…

In 2010, famed Australian value investor Roger Montgomery published a book on the craft of investing called Value.able.

Montgomery argued that uncertainty was a feature of markets, not an aberration:

‘At the time of writing there is uncertainty about Europe, interest rates, unemployment, Chinese property prices, the future of global commodity demand and there is the looming threat of climate change and higher resource taxes.

‘Whether you read this book in its year of publication or in some distant future decade, I can guarantee you will find the future has a distinct opaqueness to it.

‘Uncertainty is the one constant in investing. Yet it is precisely this uncertainty that provides the potential for reward.

‘For the investor who has adopted a long-term framework for thinking about opportunities, it is the uncertainty, and the reactions it causes, that is the very source of potential gains.’

A little over a decade since those prescient words were written and journalists and analysts are still opining about the distinct opaqueness…even as the occluded subjects remain eerily similar.

Interest rates, China’s property market, climate change, commodity prices.

Plus ça change, plus c’est la même chose, as the French say.

Investing is a prospective business. Uncertainty is both the hazard and the opportunity. Great investors realise and learn to live with the fact.

But that’s not to say it’s easy.

The world of yesterday clashing with the world of tomorrow creates a mighty clamour. Where’s the signal amid all the noise?

Cogent analysis and sound information are the investor’s weapon against the murky future.

Speaking of analysis and information…

A bit about us — Fat Tail Investment Research

While themes and trends can come and go, one thing that doesn’t go out of fashion in the investing world is insightful analysis.

Information is the crucial ingredient in markets.

But information alone isn’t enough.

It’s the rational analysis of the information that separates a sound idea from a weak one.

Here at Fat Tail, our editors pride themselves on providing valuable insight by applying their industry experience and knowledge.

At Fat Tail, we value differences.

Disagreement isn’t censured but encouraged.

And we find our readers appreciate the range of thought and ideas of our editors.

At Fat Tail, we have bulls, we have bears, we have crypto advocates, and gold bugs.

At the heart of it, though, we have a team dedicated to the free exchange of ideas. Reason trumps agenda here.