Logistics software business WiseTech Global [ASX:WTC] released its FY22 results, revealing profits rose 80%, with CargoWise revenue up 37% and total revenue up 26%.

EBITDA also rose 54% and free cash flow 71%.

While up 60% over the past 12 months, WTC shares are flat year-to-date.

Source: tradingview.com

WiseTech’s ‘strong’ performance and ‘standout’ results

The logistics software company gave a snapshot of its FY22 results:

- ‘FY22 Total Revenue of $632.2 million, up 25% (26% ex FX) on FY21 – at top end of guidance range

- ‘CargoWise revenue of $447.9 million, up 35% (37% ex FX) on FY21, driven by Large Global Freight Forwarder (LGFF) rollouts, new customer wins and increased usage from existing customers

- ‘Market penetration momentum continues with the notable win of UPS and four additional new LGFF rollouts in FY22

- ‘EBITDA of $319.0 million up 54% on FY21

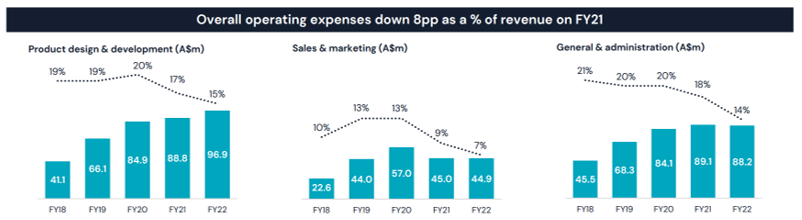

- ‘EBITDA margin of 50% up 9 percentage points (pp) on FY21, reflecting enhanced operating leverage, the benefits of exceeding cost reduction program targets and pricing offsetting inflation

- ‘Underlying NPAT of $181.8 million, up 72% on FY21; statutory NPAT of $194.6 million, up 80% on FY21

- ‘Strong free cash flow of $237.3 million, up 71% on FY21; cash at 30 June of $483.4 million

- ‘Final dividend of 6.40 cents per share (cps), up 66% on FY21 and taking full year dividend to 11.15cps, up 71% on FY21’

Source: WTC

Like other companies operating under present market conditions, WiseTech did report COVID-19-related capacity limitations, port blockages, supply chain disruptions, and a squeezed labour force.

However, WTC said it managed to increase its revenue and profit, nonetheless.

10 new global customers signed for CargoWise in 2022, including Access World, UPS, and FedEx.

WiseTech’s CEO, Richard White, commented:

‘This standout performance demonstrates the increasing resilience of our business model. In an environment of persistent supply chain constraints, inflationary pressures and COVID-related business disruption, to have delivered these outcomes is a real testament to the strength of our business, the dedication of our people, and the effectiveness of our 3P strategy.

‘We are taking advantage of the current environment by increasing the pace of our investment in R&D and high-quality talent to drive future revenue growth.

‘We remain firmly focused on achieving our vision of being the operating system for global logistics, and we have the product, strategy and resources to achieve it.’

WiseTech’s growth outlook

Mr White then offered his thoughts on where WiseTech is heading, providing a business outlook:

‘We are well-placed to benefit from continuing M&A consolidation activity amongst global logistics operators, and their increasing investment in replacing legacy systems with digital solutions, as well as pursuing our own M&A opportunities. Looking ahead we also remain focused on R&D and accelerating our investments to deliver breakthrough products that enable and empower those that own and operate the supply chains of the world.’

WiseTech spoke of a ‘strong outlook’ for FY23, setting a guidance range of 20–23% revenue growth ($755–780 million) and 21–30% EBITDA growth ($385–415million), with continuing strong demand:

‘Demand for goods continues to outpace pre-COVID-19 levels, 4.9% above pre-COVID trendlines.

‘Global freight forwarders and logistics organizations continue to accelerate their adoption of technology in the pursuit of improved productivity, and our new Large Global Freight Forwarder wins with leaders like UPS and FedEx demonstrate how CargoWise is rapidly becoming the industry standard.’

While logistics organisations accelerate their adoption of freight tech, so too is the world in a different type of tech: battery tech.

EVs will require huge quantities of lithium, copper, graphite, and nickel…presenting certain opportunities.

Lithium stocks were immensely popular last year, and even though the money came easy with the peak — the boat hasn’t necessarily been missed.

Our small-cap expert, Callum Newman, knows of three battery material stocks that have been, and still are, overlooked.

Regards,

Kiryll Prakapenka