If you’re like me, you’re probably wondering where to invest.

You might suspect (correctly) that most assets are reaching historically high levels of valuation.

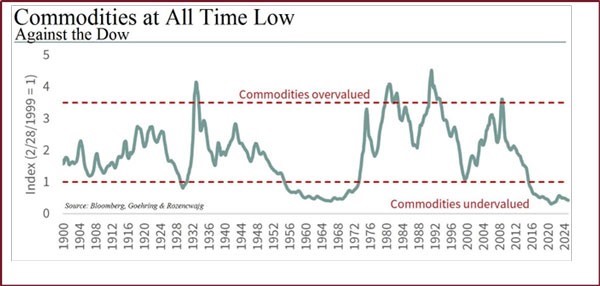

There’s a lot of risk in this market and not much upside.

At best, you might be chasing the last culminating highs in stocks already stretched, hanging onto rate cut expectations or overextended AI mania.

Resources remain the exception to this rule.

The following graph perfectly illustrates what I mean:

| |

| Source: Goehring & Rozencwajg |

The valuation for commodities is at a historical low relative to US equities.

And when you reach these levels of historic undervaluation, remarkable things happen, like the 400% increase in oil prices from 1973 to 1974.

That was the last time commodities reached today’s levels of deep undervaluation.

Most undervalued in 120 years

You don’t need to be a genius to determine what will happen here.

Either equities worldwide need to fall precipitously or hard assets need to rise dramatically so that this historic abnormality can be restored.

Either way, commodities are a safer bet for investors.

That’s why, at my paid advisory service, we’re shifting our focus to one of the market’s most hated sectors: oil and gas producers.

Stocks here often trade at a price-to-earnings (P/E) ratio of around 6, a simple but effective valuation metric.

The lower the ratio, the greater the perceived value.

For perspective, the average P/E of stocks in the Nasdaq 100 sits at around 32!

A 10-year-old could tell you something’s out of whack here.

It’s only a matter of time before market forces begin to stabilise. Make sure you’re prepared when they do!

Why make the shift into commodities

right now?

Well, here’s a slice of a recent report written by Goehring & Rozencwajg that perfectly illustrates why you need to be taking action (emphasis added):

In both 1966 and 1971, monetary policy took a conspicuous turn toward accommodation—not because the economic data demanded it, but because the men in the Oval Office did.

Faced with mounting inflationary pressures, the Fed, under Martin and later Burns, relented. The result? Inflation took off like a shot. Equities struggled and natural resource stocks were one of the only bright spots in the market.

It is our firm belief that Jerome Powell stands at the same fateful crossroads. And if history is any guide—as it so often is—the road ahead leads not to price stability, but to another inflationary surge, just as potent as those that came before.

The main point here, inflation remains a very real threat, despite what the headlines might say.

As G&R point out, this will place enormous pressure on virtually every asset class, except commodities.

Inflation could be the key catalyst that drives commodities higher and US equities lower—stabilising the steep valuation gap.

No one can predict exactly when this event will happen, but it will.

The time to prepare is now.

Until next time,

Regards,

James Cooper,

Mining: Phase One and Diggers and Drillers

Comments