Dear Reader,

We have a new Reserve Bank governor! But don’t let that distract you from what matters.

As my What’s Not Priced In co-host Greg Canavan said, whether it’s Philip Lowe or Michele Bullock, ‘they’re all life-long bureaucrats; expect more of the same’.

And, in any case, we shouldn’t mistake news for research.

Investors speak of the harsh impacts of a rapid hiking cycle. But let’s not underestimate the blunting effect of the news cycle.

News can help make sense of the world, but that’s not the same as understanding it.

Investor James Valentine made the point well (emphasis added):

‘While the news may be interesting and provide new data points, it doesn’t forecast the future, which is the job of an equity analyst. You can waste a lot of time reading stories that don’t help pick stocks.

‘The financial press will often follow a herd mentality by having a party when the Dow Jones Industrial Average hits new levels and predicting the next Great Depression when the market hits a near-term low. Don’t look for the press to take an out-of-consensus money-making stance…’

Humbly, if you can’t look for the press to assume an out-of-consensus stance, you can look for Fat Tail to.

That’s what our podcast is all about! So what did Greg and I cover this week?

This episode, we pondered the implications of the positive inflation data in the US. The key question is, is the cause behind the disinflation falling aggregate demand or normalising supply?

The former doesn’t bode well for markets.

We then discussed the divergence between market fundamentals and stock valuations with real yields still high but stocks rising. The market always looks ahead, but how far is too much?

Greg then looked at some gold stocks, ending on a general discussion of his valuation approach. The takeaway? Remember, it’s not a stock market, but a market of stocks.

Disinflation — but why?

We’ve all seen the numbers.

US headline inflation rose 0.2% in June and ‘only’ 3% over the last 12 months, down from 4% year-on-year in May, the lowest inflation level in over two years.

Consensus forecasts expected 3.1%, so inflation surprised to the downside (hooray!).

That said, core inflation remained elevated, falling from 5.3% YoY in May to 4.8% in June.

That’s the numbers. But what do they mean?

The key question for Greg was whether the rate of inflation was slowing because of waning aggregate demand or the normalisation of supply.

The former is not nearly as propitious for markets as the latter.

In any case, disinflation doesn’t mean the quick end of high interest rates. As we elaborate in the episode, this sober fact remains underpriced by the market.

Core inflation is still running at 4.8%, well above the target range of 2%. And now economists are warning of the ‘last mile’ inflation challenge — getting inflation down from 3% to 2%.

Late last month, the Bank for International Settlements released its annual economic report, stating (emphasis added):

‘Inflation could well turn out to be more stubborn than currently anticipated. True, it has been declining, and most forecasters see it moving within target ranges over the next couple of years. Moreover, inflation expectations, albeit hard to measure reliably, have not rung alarm bells. Even so, the last mile could prove harder to travel.

The surprising inflation surge has substantially eroded the purchasing power of wages. It would be unreasonable to expect that wage earners would not try to catch up, not least since labour markets remain very tight. In a number of countries, wage demands have been rising, indexation clauses have been gaining ground and signs of more forceful bargaining, including strikes, have emerged. If wages do catch up, the key question will be whether firms absorb the higher costs or pass them on. With firms having rediscovered pricing power, this second possibility should not be underestimated.’

Who knew central banks and retailers are dealing with similar problems?

Valuations adrift from fundamentals

It’s not just Twiggy and Nicola Forrest separating. Valuations and market fundamentals are uncoupling too.

We canvassed this last week, but the split between market fundamentals and stock valuations remains.

And it’s been picked up by the bigwigs in Morgan Stanley. Earlier this week, the investment bank’s Lisa Shalett released a note, warning valuations are unmoored from fundamentals:

‘Experienced investors know that in the short run, valuations are poor predictors of return. When we look ahead to periods of one year or more, however, they matter a lot.

‘Notably, current price/earnings (P/E) ratios have decoupled from one of their most fundamental drivers — the 10-year US Treasury real yield. This rate is the basic building block for discounting future cash flows, especially for long-duration growth stocks.

‘The current 10-year real rate is in line with last October’s cycle high, which correlated with a stock market trough and P/E ratios below 17.3. Today’s forward P/E ratio of 20 thus looks completely unjustified.’

It almost sounds like Shalett tuned in to last week’s episode.

As Greg pointed out, the tight relationship between the S&P 500 and real yields (below, represented by the price of TIPS) has broken down in recent months:

Source: Optuma

Greg and Shalett weren’t the only ones to notice the divergence.

Another Fat Tail colleague — Peter Bakker — picked up on the trend by looking at the copper-gold ratio’s correlation with the S&P 500.

The pair correlated well…until recent months.

Source: TradingView

The jaws of death

What do these ‘jaws of death’ mean?

It seems the market is pricing in a ‘soft landing’, where inflation comes down without too much of a fuss.

The market is seeing past current high real rates.

Simplistically, for the tight relationship between real yields and valuations to resume, either stocks correct, or real yields collapse.

The market is clearly pricing in the latter (and Greg sees an outcome where real yields and valuations meet in the middle).

The market is betting on high interest rates working their way through the system to rid it of inflation without adverse effects.

How reasonable is that bet?

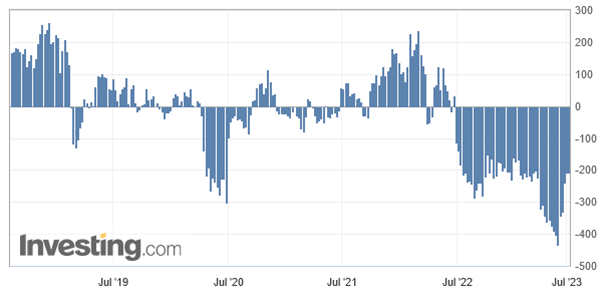

Short positions unwind…and stoke rally?

Greg and I then also canvassed whether the recent bull run in US stocks is being partly driven by short sellers covering their positions.

Greg noted that short positions peaked last month and have steadily unwound since.

How much of recent market performance is attributable to positioning and how much to fundamentals?

Source: Investing

Golden stocks of the week

Gold miners took out this week’s top spot.

Out of the 20 best-performing stocks on the ASX 300 this week, 11 were gold stocks, hence the spotlight this episode.

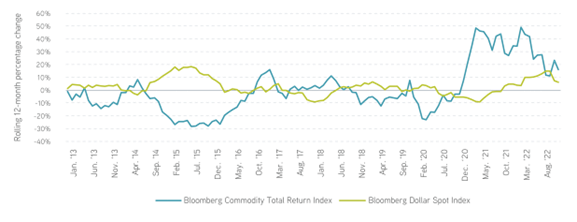

Greg pointed to the weakening US dollar as a contributing factor. In fact, Greg thinks investors should keep an eye on the greenback.

If the dollar continues to soften against other major currencies, it bodes well for commodities, like gold.

Source: Parametric

Battle of the valuation models: return on equity versus dividends

Half-jokingly, Greg and I ended the episode with a call-out.

If viewers were so inclined, we would stage a valuation contest.

I’ve been writing about the handiness of the dividend discount model to value stocks in recent weeks, much to Greg’s indifference, even outright consternation!

Greg doesn’t buy the model’s logic.

His preferred approach uses return on equity.

He actually sets out the ROE methodology in his book You, Your Brain & the Stock Market.

But I don’t want to talk up his method too much if we ever do host that episode.

Anyway, if you’re interested in something like that, let us know in the comments.

Hope you enjoy this week’s episode!

Kiryll Prakapenka