‘A tech correction is coming. The only remaining question marks are when it will happen and how bad it will be.

‘The NASDAQ index is now up around 5,000 points, the culmination of a terrific seven-year run in which it has tripled in value. The only other time it reached this level was just before the dot.com crash in 2000. In comparison, the Dow Jones has only risen by half as much over the same time period.’

This was written at the end of 2015. Since then, the Nasdaq has gained approximately 240% and took three years from that point to show any signs of slowing down.

Predictions are hard, and market sentiment rules the day — fundamentals be damned.

For months, investors have snapped up tech stocks as if the threats from the US Federal Reserve to slow the economy were a lie.

Now that they have finally put their money where their mouth is.

The Federal Reserve today has shifted its outlook for when they will drop rates.

It now forecasts interest rates of 5.1% at the end of 2024, half a percent higher than its previous 4.6% outlook.

Markets have soured as a response, and investors are now divided over how long the big tech rally will last.

Rather than give another wild guess about where this is going, I will instead explore some of the assumptions that bulls are making when they think the tech rally will continue.

As for the pessimists, it’s much of the same story as the quote above.

What the tech rally has looked like

The main driver of the optimism in the current tech rally is around AI.

Most people have experienced ChatGPT or other Large Language Models (LLMs) first-hand and experienced the incredible power of these generative AI.

The level of hope that has been pinned to this one fact alone has seen the Nasdaq and S&P 500 rise double digits this year.

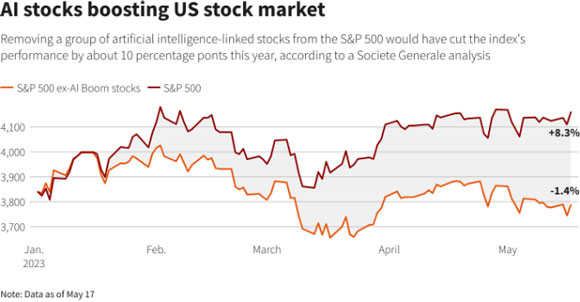

Take a look at this chart from the first half of the year.

|

|

| Source: Societe Generale |

If we removed AI-linked stocks from the performance of the S&P 500, it would have been nearly 10% weaker.

The 10 largest companies in the S&P 500 now comprise 34% of the index with an average P/E ratio of 50x.

This is the highest percentage since 2001, during the Dot-com bubble.

Even in the 2008 bubble, this percentage peaked at around 26%.

These same 10 companies have accounted for nearly 80% of the Nasdaq’s entire rally this year.

The Nasdaq has seen an incredible 25% gain this year, but began to slow in August, a seasonally slow time for stocks.

As the old Wall Street adage goes, ‘Sell in May, go away’, as trading in the summer months in the US is historically poor as traders go on holiday.

Now that markets are increasingly held up by a few stocks, particularly in the technology sector, it should be worth exploring what these few stocks promise for the future.

What are the bulls expecting from AI?

The key word here is productivity.

Much of the hopes of these new generative AI and their future impact on markets are pinned on the hopes of vast gains of productivity for everyday workers in offices and jobs around the world.

But until very recently, there has been no proof of this progress in anything but the promises and anecdotes from the Zuckerbergs of this world.

But the trickle of evidence has finally begun.

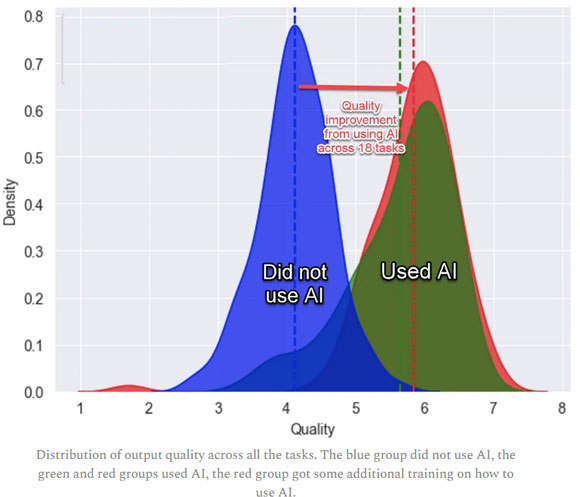

In the latest paper, published on the 15th of September, we finally have concrete data showing evidence for the productivity effects of AI on worker productivity and quality.

|

|

| Source: (Dell’Acqua, 2023) |

Consultants using AI finished 12.2% more tasks on average, completed tasks 25.1% more quickly, and produced 40% higher quality results than those without.

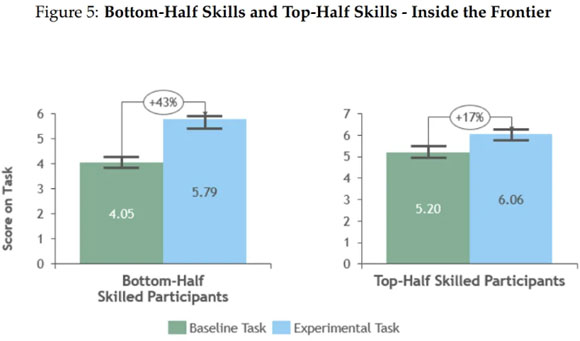

The other important takeaway from the results was that AI became a significant skill leveller between experienced/high-skill workers and new entrant/low-skill workers.

The biggest jump in performance was seen in the bottom half of users in terms of skills, who saw a 43% increase in performance.

|

|

| Source: (Dell’Acqua, 2023) |

Another study published in July also found that employee productivity increased by up to 66% in everyday business tasks.

With actual evidence in hand, it points to an exciting future of AI assisting humans in everyday jobs and possibly becoming our modern-day steam engine moment.

These gains in productivity could spell the future that the bulls are expecting, one in which a new age of productivity sees markets continue their bull run.

However, with obvious risks on the horizon, such as persistent inflation and an anaemic global economy, it’s certainly a time to be cautious.

Now that we move into a ‘higher for longer’ interest rate environment in the US, more investors could shift into defensive positions around energy and healthcare and leave the tech rally out of gas.

Whichever way the conversation moves, the next question will be, will any of this matter as sentiment inevitably shifts again?

Good investing,

|

Charlie Ormond,

Guest contributor, Money Morning