Specialty retailer of youth casual apparel Universal Store Holdings [ASX:UNI] declared that it would be upgrading its guidance on group sales expected to reach the range of $258 million to $261 million for the full financial year.

This was up from the previous report of the sales range in FY22 when the total had hit $208 million in group sales.

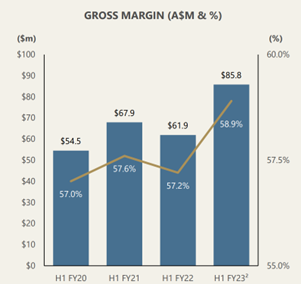

Underlying EBIT was also reportedly expected to be in the range of $39–41 million, compared to the $32.6 million earned last year.

However, the clothing retailer experienced a share price slump by the early afternoon, mere hours after posting its increased expectations.

UNI was down a significant 27.5% drop in share price after lunch time, trading for $3 a share, not helping its 42% deficit in the year so far:

Source: TradingView

Universal Store upgrades guidance yet youth sentiment is low

Reporting from its headquarters in Brisbane, Universal Store, specialty retailer of youth casual apparel, posted a trading health and guidance report for the full year ending 30 June 2023.

Only yesterday the group put out its first half 2023 highlights, speaking of total group sales reaching $145.7 million, a 34.5% increase versus prior corresponding period.

Underlying EBITDA (earnings before interest and tax, amortisation, and depreciation) had grown 43.2% on the same time last year to $28.5 million.

Statutory net profit after tax reached $17.8 million, another 31.7% climb versus the prior period and net cash was posted as $14.3 million as at the end of the calendar year.

Today, the retail group said that it is on track to deliver record sales in FY23 and material growth in EBIT compared to FY22 even despite a deteriorating macro environment and increasing signs of pressures on youth customer discretionary spending levels.

Universal Store has nevertheless decided it would upgrade its guidance, with group sales to be in the range of $258 million to $261 million for FY23.

Previously, the company had reported $208 million in group sales, in FY22.

Universal also says that its underlying EBIT is expected to be in the range of $39–41 million, which compares to $32.6 million in FY22.

The group said that although its margins and business unit inventory levels have been well managed, this was against a backdrop of increased promotional discounting activity from its peers and some evidence of overstocking in the market.

On top of this, Universal also observed trading conditions throughout April and May have further tightened, with signs of customers reducing their spending in the high-inflationary environment.

On that note, the group expects this subdued environment to continue for the balance of FY23 and into FY24.

UNI commented:

‘We are comfortable with the current inventory position across the Group. Inventory at 30 June 2023 is expected to be higher than the prior year, primarily due to the CTC acquisition, incremental new store openings, and the higher inventory holding supported by the upgraded distribution centre.

‘The Group remains committed to delivering superior in-store customer service and outstanding on-trend product, deepening relationships and reputation with customers.

‘The Group will continue to make the right long-term decisions despite the challenges of near-term sales volatility and a difficult macro environment.’

Universal’s full-year results for the 12 months ending 30 June will be released towards the end of August:

Source: UNI

Australia’s evolving economy

The global supply chain is twisting.

Australian trade isn’t what it once was.

The change is all around us, but what is it all pointing to?

Jim Rickards, financial and geopolitical analyst, has pieced certain puzzle pieces together.

He says ‘no one is talking about how this could end the Australian economy as we know it’ as soon as within the next 12 months.

Learning the patterns and getting ready for change could put you ahead of the curve.

If you want to know more about the biggest geoeconomic shift of our lifetime click here.

Regards,

Mahlia Stewart

For Money Morning