Last weekend, I wrote about the immediate risks in a shutdown of the Strait of Hormuz.

That was Oil, LNG, fertiliser costs, and the inflation shock that follows when a fifth of the world’s seaborne energy disappears overnight.

That was the first-order story. Today, I want to explore the less obvious second-order effects this conflict could have on base-metal commodities.

Think copper, cobalt, nickel, zinc and manganese.

A place where you may have capital parked right now on the ASX.

Here, the law of unintended consequences doesn’t care about military strategy or your portfolio positions.

It doesn’t respect borders. And it has a habit of punishing everyone, including the architects of the conflict.

Is Anyone Prepared?

The baseline assumption is that the Strait of Hormuz will return to normal soon.

But if it doesn’t, we’re facing a cascading series of disruptions that no military planner seems to have modelled.

This week, Trump attempted to calm shipping companies, promising insurance and naval escorts for those brave enough to cross the Strait.

The world’s largest shipping industry association called the promises ‘unrealistic’.

‘Nothing is sure, and we need immediate clarity,’ was the response from one bulk carrier firm.

As I mentioned last week, the risk to shipping has evolved. This isn’t about naval mines and attack boats of the ‘80s. The US already rules the waters of the Gulf.

The real risk lies in the distributed and highly mobile threat of drone strikes.

As they say, a picture is worth a thousand word. These drones can be moved and launched via commercial trucks within a highly mountainous country.

Source: Tasnim | Ima Media

Meaning this is a threat that will take far longer to solve than many assume.

And so, let’s dive back into what an extended shutdown can look like for markets.

The Chemical Nobody Talks About

Oil gets the headlines. But another disruption may come from something you’ve probably never considered: sulphur.

Roughly 45% of global sulphur exports pass through the Strait of Hormuz.

The Gulf is the world’s largest sulphur producer because refining sour crude oil generates elemental sulphur as a by-product.

About 85–90% of the global sulphur supply comes from oil and gas refining.

Qatar’s Ras Laffan complex alone processes roughly 20% of global LNG and 10,000 tonnes of liquid sulphur daily. That was until two Iranian drone strikes forced its closure last week.

Source: Discovery Alert

When that supply disappears, it removes an estimated 3.8 million tonnes of annual capacity from the global market.

Sulphur is the starting material for sulphuric acid, the most widely produced industrial chemical on Earth.

Sulphur is not a glamorous element. But it’s essential to your daily life.

It extracts copper, processes uranium, refines cobalt and nickel, produces phosphate fertilisers, and treats water. There is no modern industrial economy without it

And here’s where the unintended consequences begin to cascade.

Copper’s Hidden Bottleneck

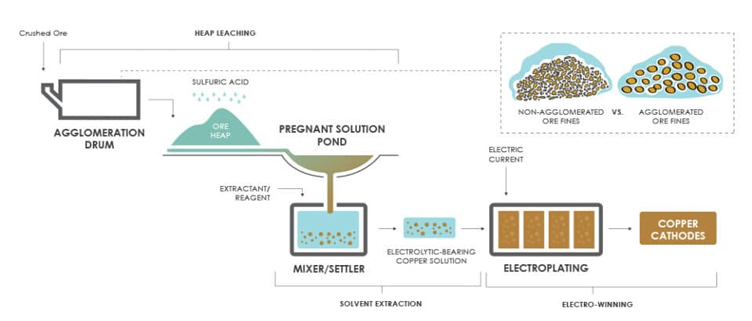

About 25% of global copper production relies on a process called SX-EW, or solvent extraction and electrowinning.

It’s the standard method for processing oxide copper ores in copper hotspots, and it runs on vast quantities of sulphuric acid.

Here’s the process simplified:

- Ore is stacked in heaps and sprayed with sulphuric acid. Copper dissolves into a solution.

- Solvent extraction (SX) concentrates and purifies the copper from that liquid.

- Electrowinning (EW) uses electricity to deposit pure copper metal onto cathode plates.

If you’re a visual person you can see that process here. Starting at the top left, moving to the bottom right.

Source: Feeco International

[Click to open in a new window]

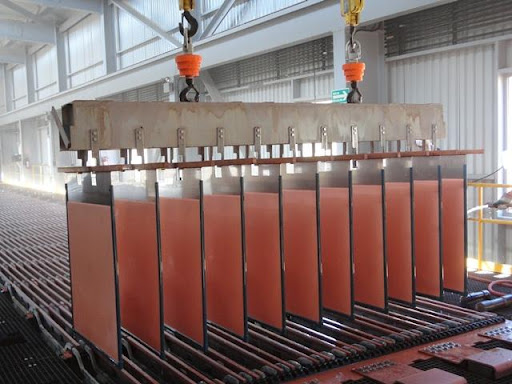

And here is what the copper looks like coming out of that process. Copper plates of over 99.99% purity.

Source: Daily profit cycle

The process is relatively modern, but it’s catching on quickly. Its success has enabled many previously considered low-grade deposits to become economic.

And now the world’s largest copper-producing regions; Chile, Peru, the DRC, and Zambia are all dependent on it.

The DRC alone imports over 500,000 tonnes of elemental sulphur annually to keep its acid plants running for cobalt and copper.

In a prolonged Hormuz shutdown, that imported sulphur vanishes.

Regional acid inventories are measured in days, not months. That’s often because sulphur is bulky, and generally low value per tonne.

This market has been shaped by buyers who’ve avoided the cost of financing, storing, and insuring inventory — preferring ‘just-in-time’ supply chains.

In an extended scenario, that ‘efficiency’ comes back to bite.

African mines would grind to a halt, and many others would curtail output and sit on their hands.

Suddenly, copper becomes constrained — not by the availability of ore — but by a chemical input most investors have never heard of.

But that’s just one side of the shock.

Copper was already near record levels before the conflict, hitting US$6 per pound in late February. Since the conflict began, prices have started to fall.

Source: TradingEconomics

[Click to open in a new window]

Copper prices will continue to face a tug-of-war in the months ahead.

On one side, expectations of higher energy costs and a broader economic slowdown weigh on industrial metals demand. That’s the bet the bears are making right now.

On the other, the physical supply squeeze from acid shortages could tighten the market in ways that demand-side models don’t capture.

And in commodity markets, physical bottlenecks have a way of winning that argument.

Beyond Copper

The acid shortage doesn’t stop there. Uranium extraction via in-situ recovery depends heavily on sulphuric acid.

Kazatomprom, the company that produces over 20% of the world’s uranium, had already cut its 2026 production by 10% amid a sulphuric acid shortage.

And that was before this conflict.

Cobalt faces the same constraint. Over 70% of global cobalt comes from the DRC, where high-pressure acid leaching is the standard method.

If acid is rationed, cobalt output contracts, feeding directly into battery supply chains.

What emerges is a picture of competing industries bidding for the same scarce input.

Fertiliser producers are obviously politically at the top of the priority list and will get first claim.

Miners then become residual buyers, exposed to rationing that could make marginal operations uneconomic.

The Lesson

The law of unintended consequences is not a law at all.

It’s a reminder that complex systems don’t behave the way simple models predict.

You close a shipping lane to punish one country. Only to constrain copper production in Zambia, uranium output in Kazakhstan, and cobalt supply to the global battery industry.

The architects of this war may have planned an oil shock.

It’s not clear they planned for an acid one.

Regards,

Charlie Ormond,

Small-Cap Systems and Altucher’s Investment Network Australia

Comments