Today, I thought we’d continue our look at the Aussie Dollar as a potential marker for understanding our position in the commodity cycle.

A quick recap: a vital influence (or tailwind) on the AUD is the strength of the Australian economy, which relies on commodity exports, which in turn fuel the country’s Terms of Trade.

So what exactly does that mean… Terms of Trade?

Simply put, it indicates how many imports a country can BUY with its exports.

Think of it like this: Country ‘A’ exports corn, and Country ‘B’ exports tractors.

Now, Country A sells 100 tonnes of corn for $100,000; Country B sells 10 tractors for $100,000. Their terms of trade are 1:1.

But now imagine that corn prices RISE.

Country A now gets $120,000 for 100 tonnes of corn.

Meanwhile, in Country B, tractor prices have remained unchanged.

Country A can now buy 12 tractors for the same amount of corn.

And that IMPROVES its terms of trade.

How this fits with the AUD/Commodity Idea

Alrighty, improving terms of trade doesn’t necessarily translate into a one-for-one correlation with a strengthening Aussie Dollar.

Other factors play a role, such as the nation’s overall economic health, including growth and the ability to pay down debt.

Monetary policy is also critical; higher rates tend to attract foreign investment, further strengthening the AUD’s value.

But it all cascades back to the country’s Terms of Trade...

Strong commodity prices boost export revenues, which help drive economic growth and allow the flexibility to pay down public debt (or spend more).

And all this economic activity will prompt central bankers to favour rate hikes over cuts, further attracting foreign investors to the AUD.

That’s why, as commodity prices rise, it creates a positive snowball effect for the Aussie Dollar.

Hence, we can use it as a bellwether currency for understanding the commodity cycle.

Last week, we looked at a key year for the Aussie Dollar: 2001.

That’s when the AUD traded as low as $0.47 against the US greenback, the lowest level ever reached for the AUD since the currency was floated back in 1983.

At the time, Prime Minister John Howard argued that the weakness was simply a reflection of the US dollar’s strength.

Yet, at the time, the AUD was also falling against the euro, yen and pound.

The situation looked dire, painting a bleak picture for Australia’s economic health.

But in hindsight, 2001 was a pivotal moment.

While 2001 was a major low for the Aussie Dollar, it also marked the beginning of a new cycle… A transfer of global wealth.

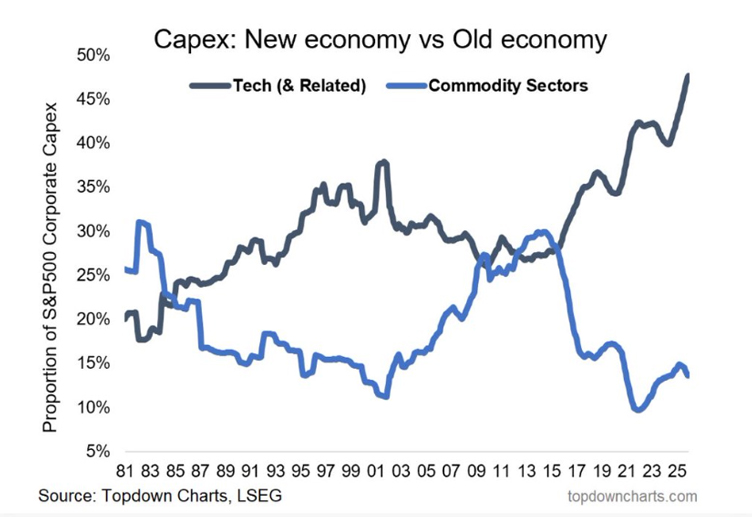

As you can see below, global investment began to shift AWAY from the inflated tech bubble and back into the depressed commodity market:

And significantly, a bottom in mining investment (back then) mirrored the all-time low in the Aussie Dollar.

So, it’s hard to argue against a strong correlation between the Aussie Dollar and commodity prices.

That’s why institutional traders use the AUD to leverage their commodity exposure.

And it’s precisely why we should be paying close attention to this relationship, especially right now.

Why?

Well, for the first time in a very long time, investors are finally favouring commodities over tech investments.

The Once-in-a-Decade Sector Rotation

As you can see on the chart above, capex investment in resources is hovering back around those 2001 lows.

That should get you excited about what could happen next!

There’s a strong historical pretext at play here…

The Aussie Dollar is near its major lows, just as the mining capex cycle bottoms (relative to tech).

Think about it like this: the tech boom has created trillions in new wealth, far in excess of what the Dot-Com bubble of the late 1990s created.

After the Dot-Com bubble, much of the capital flowed into the old economy, the resource market.

If we see that repeated, well, that could deliver an unprecedented opportunity for companies leveraged to higher commodity prices.

To find out more, be sure to check out my latest report here.

Regards,

James Cooper,

Mining: Phase One and Diggers and Drillers

Comments