Railroads were one of the largest sectors of the economy from 1870–1930 but were mostly bankrupt by the 1970s. General Motors has been rescued from bankruptcy more than once by the US Government. General Electric was once an industrial giant, and now it is a shell of what it once was. Oil company stock prices have taken a beating from the threats of the Green New Deal. Things change.

Banks and other financial institutions dominate stock market valuations today alongside the tech sector. Central Bank Digital Currencies (CBDCs) may be coming for the banks. Investors should watch developments closely and be nimble when it comes to getting out of financial stocks before the digital dollar eats their lunch.

The endgame for CBDCs would closely resemble George Orwell’s dystopian Nineteen Eighty-Four. It would be a world of negative interest rates, forced tax collection, government confiscation, account freezes, and constant surveillance. If cash is gone, there is only one way to escape digital confiscation of wealth — physical gold.

Bubble behaviour, or worse

Based on the Nikkei and Nasdaq crashes described previously in this series, Bitcoin [BTC] could fall from US$60,000 to US$10,000 or lower before establishing a new base. Still, there’s one important difference between the Nikkei and Nasdaq bubbles and the new bitcoin bubble.

The Nikkei and Nasdaq bubbles were based on a combination of investor mania, leverage, and hyped-up earnings releases from companies in the index. But there was relatively little outright fraud. In contrast, the bitcoin bubble is based almost entirely on fraud. There’s substantial evidence that the price of bitcoin is based on a Ponzi.

More than 50% of bitcoin purchases are made with another cryptocurrency called Tether, a so-called stablecoin. Tether has never accounted for the billions of dollars that buyers have used to acquire Tether. Hard currencies such as dollars go into Tether, while Tether is used to pump bitcoin, and the dollars are possibly skimmed away. That process doesn’t work in reverse.

Bubbles cause real damage when they burst

This isn’t just a spectator sport for prudent investors who don’t own bitcoin. The types of losses arising from a bitcoin collapse would easily spill over into brokerages and banks handling accounts of investors who were selling everything because they were desperate to raise cash and avoid further losses.

Since the shady bitcoin and Tether exchanges are unregulated, there’s perhaps little that can be done to avoid this coming fiasco. Investors should at least be alert to the potential collapse by increasing their cash allocations to help weather the storm.

That said, none of this may matter. Bitcoin has become a belief system. True believers see what they want, hear what they want, and are immune to the arguments of non-believers.

Untethered money

Here’s how the fraud works, as described in a legal notice from the New York State Attorney General. A company called Bitfinex sponsors the cryptocurrency called Tether. This crypto is a so-called stablecoin. This means that the value of one Tether is fixed at US$1. When you buy a Tether for US$1, the money is supposedly held in safe liquid assets. When you cash in your Tether, you should receive US$1 in return (less small transaction costs). The problem is that no one has been able to locate the liquid assets that supposedly back Tether.

There’s been no full audit, and there is no transparency about the whereabouts or composition of the liquid assets backing the coin. Tether claims its dollar reserves are held in a Bahamian bank named Deltec Bank & Trust. But independent research revealed that the assets claimed by Tether exceed the total US dollar assets of the entire Bahamian banking system.

Other research shows that those who buy Tether use them overwhelmingly to buy bitcoin from unregulated crypto exchanges domiciled in Africa and Asia. Of course, these exchanges exist in cyberspace only and are accessed through the internet. These exchanges offer leverage and award free Tether coins for those who bring in new customers. These Tethers have been used to bid up the price of bitcoin and create the bubble. Meanwhile, the dollars supposedly backing Tether are unaccounted for.

If this process were to go in reverse (which it inevitably will), the bitcoin values would collapse quickly (because of leverage), and Tether would be unable to redeem retreating bitcoin investors (because of the unaccounted-for liquid assets). Any Tether crooks could walk away with billions of dollars. The prices of bitcoin and Tether would collapse catastrophically. Bitcoin investors would walk away empty-handed.

The bitcoin price is not the only bitcoin bubble

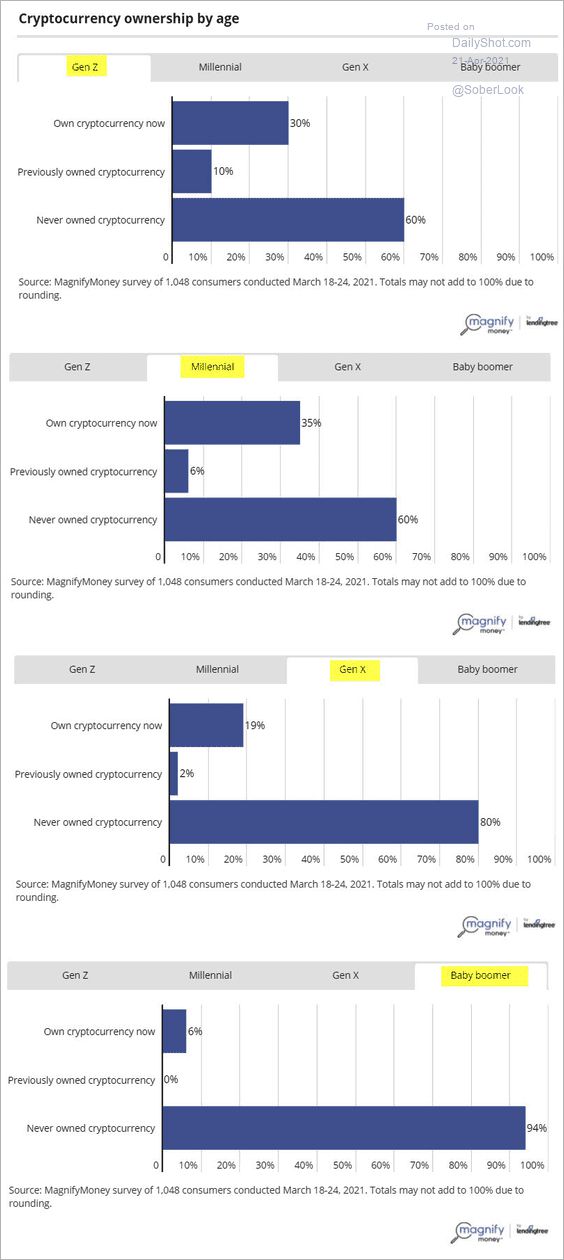

The chart below is a revealing study of the adherents to the bitcoin belief system by age cohort. It shows that 41% of millennials and 40% of gen Z are either current or former owners of cryptocurrencies, with the vast majority in both cases being current owners. In sharp contrast, 94% of baby boomers have never owned any cryptocurrency.

On the one hand, this disparity could reflect the fact that younger people are more tech-savvy, less involved in traditional stock and bond markets, and are more open to the new environment created by bitcoin and other cryptocurrencies — even if they cannot see or understand that environment. They could be on the cutting edge of a phenomenon that will soon affect everyone, whether they realise it or not.

On the other hand, it could be the case that baby boomers have far more experience with asset bubbles and market crashes, including the 22% one-day stock market flash crash on 19 October 1987, the 75% crash in the Nasdaq beginning in 2000, and the mortgage market crash of 2007–08. Those who have lived through crashes of that magnitude may see bitcoin as just another instance in a long line of bubbles waiting to burst. Time will tell.

|

|

|

| Source: MagnifyMoney |

So, what is the future of money?

Gold, bitcoin, CBDCs, and Special Drawing Rights (SDRs) may all play a role in the future of money.

Gold has never lost its role as a store of wealth, but it may need a digital facelift to resume its role as a convenient currency or medium of exchange. That can easily be done with existing technology, and the digital interface will be even easier in the future.

Bitcoin isn’t a reliable store of value and is not a widely accepted currency. It suffers from a deflationary bias, absence of a rule of law regime, and an uncertain provenance due to its permissionless blockchain that is validated by a consensus of unvetted miners.

Still, bitcoin isn’t going away. It will continue as an object of fascination, a vehicle for speculation, and the cause of hallucination relative to real money. The end result will not be to displace money but rather to destroy money as a linear concept. The ensuing chaos will be cured only by gold, a hot medium, which requires little engagement by the user to reimpose the reality of money.

Central bank digital currencies are already being used in China, and more are on the way from the European Central Bank and the Bank of England. The Federal Reserve may be the last to join the party, but a digital Fed dollar can be expected by 2023, if not sooner.

CBDCs will not displace the currencies they represent (dollars, euros, yuan, etc.), but they will increase transaction speeds, lower costs, and could disintermediate most existing commercial bank functions.

SDRs or World Money will emerge not as an everyday currency but as a kind of super-currency used exclusively by Sovereign States. It may be required to settle any balance of payments, maintain books and records of global corporations, and act as a numeraire for sovereign reserves.

As the sole issuer of SDRs, the International Monetary Fund will emerge as a world central bank. Dollars, euros, and yen will remain as local currencies, not much different than Mexican pesos today. The business of the world will be conducted in SDRs with currencies such as the dollar useful for local transactions but not otherwise. The SDR will be digitised, not unlike the CBDCs.

All that remains is a linkage between the digital SDR and gold, perhaps in response to some future financial crisis that cannot be truncated without recourse to the once and future money — gold.

All the best,

|

Jim Rickards,

Strategist, The Daily Reckoning Australia

This content was originally published by Jim Rickards’ Strategic Intelligence Australia, a financial advisory newsletter designed to help you protect your wealth and potentially profit from unseen world events. Learn more here.