Over the last few weeks, I’ve given iron ore plenty of coverage.

And I’m not the only one…

Australia’s most important commodity has been trashed across the media.

As I’ll explain shortly, I think this coverage has been a bit unfair…

But first, it’s worth understanding what’s driving this bout of pessimism in 2024.

You see, iron ore is battling two fronts right now:

First, you have Simandou, affectionately known as the ‘Pilbara Killer.’

This major development recently gained final approvals.

This means that after decades of setbacks and delays, all systems are go for Simandou…maidan production is expected in 2025.

This ‘mega-iron ore’ project is set to be a major boost to global supply.

And that’s bad news for iron ore prices, according to the China bears. According to them, this couldn’t come at a worse time!

Expectations of weaker manufacturing and construction growth in China have led the country’s largest steel firms to cut back production.

Chinese steel is the key driver for Australia’s iron ore demand.

The fear is that we’ll be drowning in iron ore just when our biggest customer doesn’t need it.

For these reasons, the iron ore market is sailing in troubled waters—a perfect storm of bearish forecasts.

Not surprisingly, Australia’s premier iron ore producer, Fortescue Metals [ASX:FMG], has tanked almost 40% over 2024:

| |

| Source: TradingView |

But that’s the past…

The question now is: Are we at the beginning of a long-term bear market in iron ore stocks and other commodities reliant on China’s growth?

That’s certainly a logical conclusion to make as an investor.

However, this logic could be wrong.

Let me explain…

My research suggests that this overwhelmingly bearish narrative is overblown.

To understand why, let’s kick off our investigation by digging into the supply threat…

Simandou, the Pilbara ‘rival’

According to some sources, Simandou in Guinea, West Africa, will flood the iron ore market with excess supply when it is up and running.

And the ‘go live’ date is fast approaching…

Rio Tinto, the principal investor in the region, expects the first production from the Simfer mine to hit the market in 2025.

Production is expected to ramp up after 30 months to an annualised capacity of 60 million tonnes.

So, how does that look against global output for iron ore supply?

In 2023, Australia, the world’s largest supplier, accounted for around 960 million tonnes.

Brazil came in second place with 440 million tonnes, China with 280 million tonnes, and India at 270 million tonnes.

So, how much will Simandou alter this supply balance?

Rio Tinto and other development partners are expected to generate annual output of around 90 million tonnes by 2028.

Now, compare that figure to the 2023 global production of 2,500 million tonnes.

By my calculations, Simandou will contribute around 3.6% of global supply once it reaches full production.

It’s significant but hardly warrants the headline-grabbing ‘Pilbara Killer’ label!

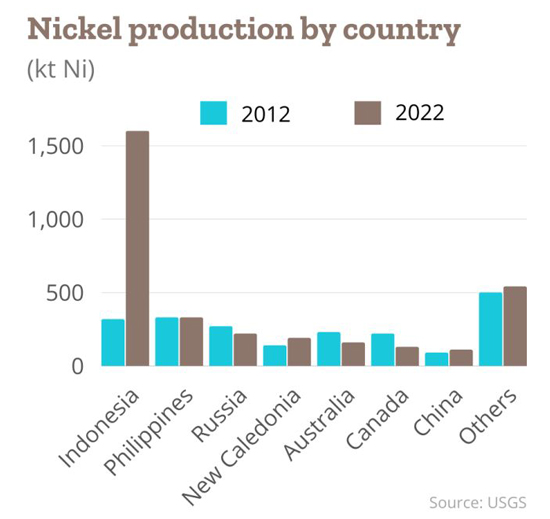

To gain a sense of what does constitutes a major supply disruption, look no further than nickel!

In recent years, Indonesia has flooded this market with new supply.

Assisted by China, new processing technologies have allowed the country to tap into its vast nickel laterite deposits.

In 2012, the country supplied approximately 300,000 tonnes of global output.

10 years later, that grew to more than 1.5 million tonnes…a four-fold increase!

Rapidly positioning Indonesia as the world’s largest supplier by a very wide margin, as you can see below:

| |

| Source: USGS |

In terms of iron ore, Simandou’s entry onto the global stage will pale in comparison to Indonesia’s dramatic impact on the nickel market in recent years.

Furthermore, operations in Guinea are still at least four years away from full production.

Of course, all this is irrelevant if demand for iron ore collapses, as most commentators tend to expect.

Which brings us back to…

The China problem

As I pointed out, ongoing weakness in China’s economy has painted a bleak outlook for the iron ore market.

But here again, I believe the bearish overtones appear one-sided.

Two weeks ago, Western media was in a frenzy after China’s steel makers announced cuts to future production.

Predictably, China bears came out in force… the decline of new housing starts was rolled out as the logical cause for these cuts.

And by that reasoning, China bears doubled down on their conviction that Australia’s iron ore sector was doomed in 2024.

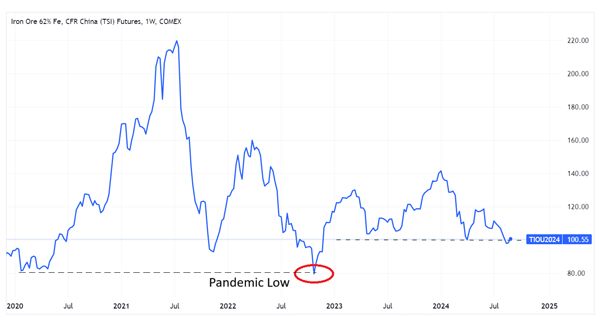

Overnight, iron ore crashed through the key psychological level of US$100/tonne:

| |

| Source: TradingView |

So, is iron ore close to bottoming out around these levels?

That’s not something I can answer.

But breaking below US$100/tonne, could see a sharp correction to around US$80/tonne (red circle above), the pandemic low from 2022.

Whether they continue to hold depends on this one critically important metric…

Iron ore imports: the key thing to watch

Last month, I detailed why investors should watch China’s iron ore imports carefully.

This is what I said (emphasis added):

‘The West holds a very superficial view of China’s economy… The narrative is overwhelmingly bearish and usually defaults to weakness in the country’s real estate market.

‘But consider this: China holds a long track record of manipulating commodity prices to its advantage. It’s hard to criticise that strategy. If you’re a major buyer, why not do all you can to limit the price you pay?

‘As the world’s biggest consumer, China has the capacity to manipulate iron ore prices and fulfil longer-term objectives.

‘And how might it achieve that?

‘Given this authoritarian state’s broad reach across Chinese-owned entities, including steelmakers, it can easily collude with them to drive down iron ore prices whenever it is strategic to do so.

‘Curbing steel production is one strategy. These latest announcements on steel output cuts “could” be part of a coordinated plan by authorities and subservient steel makers to undermine the price of iron ore.

‘Once the CCP deems prices sufficiently depressed, it might shift gears and ramp up stockpiling efforts, just as it did throughout the pandemic years.

‘And that was despite minimal demand for steel at the time.’

And this:

‘Nothing happens in China by chance, which extends to its access to raw materials… That’s why you should be observing iron ore imports carefully.

‘Strong numbers (in the face of falling steel production) will add weight to the theory that China is perhaps cutting steel production in a bid to drive down iron ore prices.’

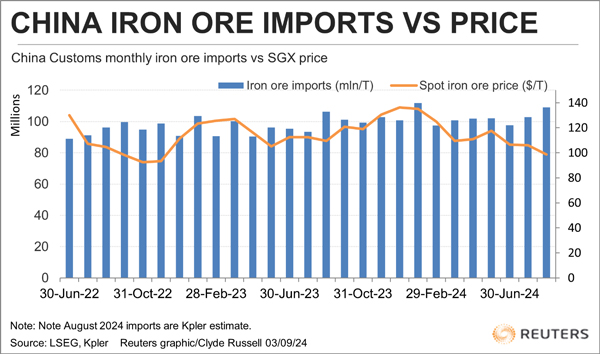

So, what’s the latest import data telling us?

Official customs data for August won’t be released until next week…given the pressure in the iron ore market, this will be one of the most anticipated releases in years.

However, early signals look positive.

Data from commodity analysts Kpler points to imports being the strongest since January 2024!

Kpler estimates August imports at 109.1 million tons, the most since January’s 111.9 million:

| |

| Source: Reuters |

If official data confirms these estimates next week, it will counter the narrative held by China bears.

After all, why would the world’s second-largest economy increase imports for this key industrial commodity against the backdrop of severe economic weakness?

Well, I gave you my take above, but of course, only the CCP knows the true reason.

As market commentators speculate on China’s economic woes and the demise of Australia’s iron ore industry, all you need to know is this:

The volume of iron ore imports into China.

If the authorities anticipate higher future demand, expect them to stockpile more ore!

Simple.

With so much market confusion, there’s no need to muddle things further.

Sit back and watch the show!

Until next time,

Regards,

|

James Cooper,

Editor, Mining: Phase One and Diggers and Drillers

Comments