Ageing populations are one of the biggest threats to the developed world. People are living longer. The younger generation are having fewer children. And the average age is rising. This leads to an imbalance between people who are net producers and net consumers.

Affluence has its perks. People own more, have access to better lifestyles, and therefore live longer. However, when this affluence is built on debt, this becomes a problem because someone must pay the debt. With less people who can do so in the future, that could be disastrous.

We’re watching this happen now in slow motion.

The fertility rate in most developed nations has dropped dramatically in the last three decades. Back in the 1990s, Australia’s average household had 2.3-2.5 children. Today, it’s barely above one.

The average age of marriage for men and women has increased. The latest data from 2023 show men are marrying on average at 32.9 years and women at 31.2 years. Back in the 1980s, the average age was around 25-27.

How did we get to this?

People are delaying marriage for several reasons:

- Higher expectations on post-marriage life,

- Changing laws on marriages, divorces, and sexual norms,

- Societal perceptions on the roles of men and women in family, career, and child-rearing, and

- Rising property prices and living costs raise the hurdle for financial security.

Many of these problems go back to money. We like to say love can overcome all troubles. But we live in a pragmatic society. Moreover, affluent societies are materialistic societies. They flourished because people dedicated their energy building material wealth.

Our monetary system stands on a bad foundation that contributes to what I believe is a hidden cause that undermines our demographics. Our younger generation faces a greater threat because they are aware that the deck is stacked against them. They stand to bear the cost rather than the benefits of the charade of fake money, government deficits, and loose lending policies.

Many know this threat, but few have the faintest idea of how to overcome it. Well, it’s time to help them…

Forget the RBA, it is the problem

On Tuesday, the Reserve Bank of Australia Governor, Mary Bullock, announced a decision that surprised and disappointed many Australians.

The rate cut that many expected and predicted did not happen. Interest rates remain at 3.85%.

Many were hoping for the rate cut as a small relief on rising living costs. Utility prices increased again at the start of the month, with many expected to pay almost 10% more than last year. It’s quite a hike, especially during this brutal winter.

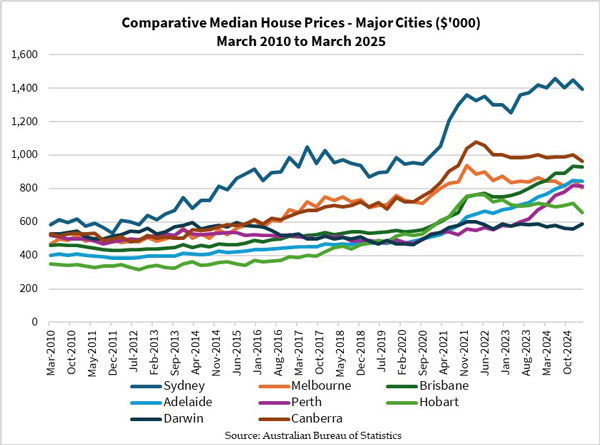

Property prices have eased a little in almost all the major cities in the most recent quarter, as you can see below:

| |

Prices in Melbourne, Canberra, and Hobart may be trending down since 2021, but they’re rising in Brisbane, Perth, and Adelaide. However, this is hardly something encouraging. These price levels remain out of reach for many first-home buyers.

Existing mortgage borrowers rode the rising property prices in recent years. However, many still have a substantial loan outstanding to pay down. Rising living costs and stagnant wages haven’t eased the burden, with many who couldn’t wait for a rate cut to come sooner.

The legacy of the RBA hasn’t been particularly good. We could say the same for central banks worldwide. The central banks are meant to facilitate economic growth by lending to the government to fund its fiscal policy. It also seeks to regulate the government against excesses through the interest rate. The government borrows but needs to pay back the debt with interest.

Accountability, separation of lending and spending, and restraint. It all sounds good except we’ve seen how the last two decades with governments around the world pressuring central banks to keep interest rates low to pump the economy and win votes. Government deficits accumulate, lending goes out of control in the public and private sectors. The key is to keep prices rising and trade to continue. This led to the central banks becoming akin to a drug dealer that fuels an orgy of spending with little thought on the consequences after.

The argument for perpetuating such irresponsible policies is that the financial system puts governments and central banks in a bind. On one hand, there are concerns about weakening business and consumer confidence when prices don’t rise enough to encourage investments. On the other, prices rising rapidly lead to more wealth inequality and increase a reliance on debt. A growing debt exacerbates the problem and perpetuates the problems mentioned.

All these make it more difficult for Australians and many developed nations. The outcome is a minority that owns a lot of assets who benefit from this debt-driven bubble, while the majority have less wealth after deducting their loans and adjusting it for inflation.

It’s the latter who have delayed marriage, have fewer children, and stay longer in the workforce. Affordable housing and cost of living are the hurdles standing in the way of a life that we’ve taken for granted.

While longevity is normally a good thing, a debt-driven economy plus longevity are ingredients to create a lopsided society that threatens to divide generations.

A hope for the future generation

I may be painting a bleak picture about our future, but let me change my tone.

Yes, there is hope. Better yet, you have a part in it.

In the recent Gold Coast Gold Conference in April, I was pleased to see a handful of attendees who were in their late teens and early twenties. They accompanied their parents and relatives for the two-day event that would have set them on a solid path in life, especially given the uncertainty and challenges under our current financial system.

I had the opportunity to chat with one of them at the conference. His name is Cameron. He’s 20 years old and working in the construction industry, so he should know a few things about building a foundation on solid ground!

But I’m not just talking about his profession. He knows what money is, and it’s not what we carry in our wallet, but gold and silver. A family friend revealed this truth to him, leading him to delve further and develop a plan to safeguard his wealth.

You can watch the video of our conversation at the conference below. I was pleasantly surprised that this one attracted almost 4,000 views:

Moreover, Cameron is on the ball about how gold is a great way to help people in his generation. Have a look at the performance of gold in the last 35 years relative to the best property market in Australia, Sydney:

| |

The best part about gold is you don’t need to take out a big loan to get started. You can buy something for as little as $100!

I know most of you reading this article are enjoying the good life. You benefited from the economic and market cycles working in your favour.

Perhaps you have already set your children and grandchildren on the same path as young Cameron. Good on you if you have! Many of us perhaps wished we had someone who shared these insights on our monetary system, precious metals, and property investing when we were younger.

Why not share this video with someone who’s around Cameron’s age? Help increase their awareness that their future is brighter if they make the right decision.

And you can even go one step further, let them know that they can learn about how to build a precious metals portfolio. Check out The Australian Gold Report.

There’s no need for grand plans and taking wild risks to build your wealth. Nor do you need to wait anxiously for economists and bureaucrats to dictate your future. It takes building a good foundation to help you withstand the challenges of our crumbling system.

That’s a gift you can give to those who will steer our country’s future.

God bless,

|

Brian Chu,

Editor, Gold Stock Pro and The Australian Gold Report

Comments