Today, I thought we’d dive into the Aussie Dollar as a potential long-term bellwether for understanding our position in the resource market.

So, how do commodities have a bearing on a nation’s currency?

Simply put, the Australian economy derives a significant portion of its income from commodity exports, which fuel what’s known as its Terms of Trade.

Rising exports provide a tailwind for the Australian dollar’s strength.

But it’s not a one-for-one correlation.

You see, other factors also influence the rise and fall of a currency, such as a nation’s overall economic health, including its growth versus debt levels.

Monetary policy is also critical in driving currencies; relatively higher rates tend to attract foreign investment into that currency.

With its low relative rates, Japanese capital has traditionally been attracted to foreign currencies offering higher returns on cash, including the AUD.

This further strengthens its value.

But as you can see, it tends to all cascade back to one central driver: the country’s Terms of Trade.

If commodity exports are strong, this ‘should’ boost national growth, increase capacity to pay down debt, and spur central bankers towards hiking rates.

That’s how rising commodity prices can have a positive snowball effect in increasing the Aussie Dollar.

That’s the theory anyway, so does it actually play out like that in the real world?

Stepping back to the days

of the Aussie ‘Peso’

2001: the Aussie dollar traded as low as $0.47 against the US greenback.

That was the lowest level ever reached for the AUD since the currency was floated back in 1983.

That was a terrible time to be travelling in the States or buying anything from overseas!

One market analyst noted at the time:

“This is a nervous level, and everybody is watching. It is the only currency in the world breaking through its lows, US48 cents is possible—and there is even a risk of a dip to US45 cents.”

Prime Minister John Howard argued that the fall was simply a reflection of the strength of the US dollar.

Except the AUD was also falling against the euro, yen and pound.

The situation looked dire and hinted at something amiss with the Australian economy.

Back then, some observers linked the massive falls in the AUD to selling by Japanese banks, who were liquidating Aussie-denominated assets to avoid collapse.

Throughout the 1990s, Japan was a major buyer of Australia’s commodities, taking in around one-fifth of our exports.

Its deep financial problems were having a significant impact on the Aussie Dollar.

Drawing from that experience could one day be essential, given today’s even heavier reliance on the Chinese market.

But I don’t think we need to be concerned about that, not yet anyway.

For now, the Australian Dollar is trading closer to its all-time lows compared to its highs.

Another factor why we could be

close to a rebound in the AUD

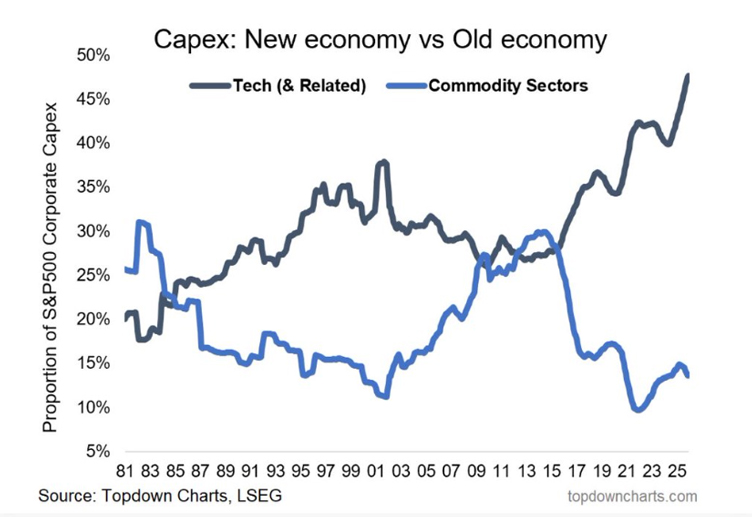

Note the chart below that my colleague, Nick Hubble, shared with me over the holiday break…

It shows the capital expenditure (capex) on tech-related investments versus commodities.

[Click to open in a new window]

Why is it important?

We could be at a critical inflection point in global markets right now…

Capital could be about to rebalance away from tech and back into commodities.

As I’ve pointed out, that could be very positive for the Aussie Dollar.

Also, note on the chart the last time capex in commodities was this low relative to the new economy… 2001.

The very year that the Aussie dollar recorded its historic low!

From there, mining capex accelerated rapidly as international markets poured into resource investments throughout the early 2000s.

That’s the playbook investors should be looking at right now.

We’ll dig into this idea further in our next edition.

Stay tuned!

Regards,

James Cooper,

Mining: Phase One and Diggers and Drillers

Comments