|

Lithium’s tracking really well right now…

After years in the wilderness, lithium is finally showing signs of life.

The sector has been absolutely decimated since its 2022 peak, with prices still about ~85% below those highs.

But the narrative is shifting in a profound way, and I firmly believe early positioning in quality lithium companies could pay off handsomely over the next 12 to 24 months.

The new demand driver:

Battery Energy Storage Systems (ESS)

Chinese lithium prices are getting a big boost thanks to growing confidence in the demand for large-scale battery storage.

Battery Energy Storage Systems (BESS) have suddenly become popular.

In China, supportive government policies have created tailwinds for BESS.

Globally, there is also growing momentum for equipment that can stabilise electricity grids and support the surging power demand from AI data centres.

And this…

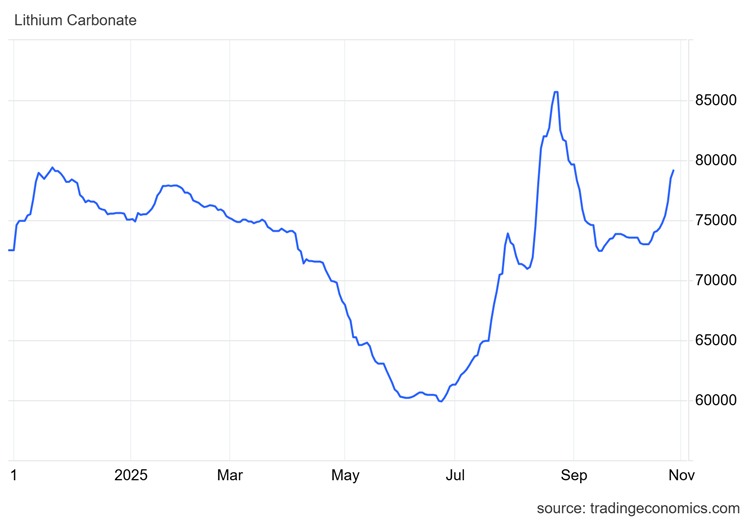

The spot lithium market in China has rebounded to a two-month high.

Prices are still depressed compared to the 2022 boom, but the trend has now reversed.

And right on cue, lithium prices have started to rise over the last couple of weeks:

Source: TradingEconomics

We hope to see that momentum continue.

I still believe that a major lithium price rally will come in the medium term, since the market will likely have a supply deficit next year.

Now, let’s talk specifically about our lithium positions…

China’s industrial strategy

Batteries have become a new driving force in China’s industrial growth strategy, along with solar panels and electric vehicles.

Last month, the Chinese government unveiled measures to scale up BESS capacity and investment. These include compensation mechanisms to ensure that sufficient storage capacity is built to meet peak demand.

This plan relies on batteries and particularly lithium-ion batteries.

The plan is to more than double storage capacity to 180 gigawatts by 2027.

This expansion will help support the rapidly increasing and often intermittent flows of wind and solar power to the grid.

This pushes key battery ingredients, especially lithium, into high demand. It also helps ease concerns about the massive oversupply that crashed prices at the end of 2022.

Global players echo the optimism

It’s not just China.

South Korea’s Samsung SDI has been converting some EV battery production lines to increase BESS output in the United States.

Australian miner Pilbara Minerals said last week that the sector is growing in ’leaps and bounds’.

According to BloombergNEF, energy storage installations worldwide are on track to hit record highs every year through 2035. This trend will cement China and the US as the largest markets.

Demand for EV batteries is expected to grow in the mid-20% range this year. In contrast, demand for BESS is projected to grow in the mid-50% range, according to Chris Williams, an analyst at Adamas Intelligence.

Adamas are usually quite bullish, but they are often right.

This difference in growth rates is critical.

This means lithium demand is diversifying beyond just electric vehicle adoption.

Market dynamics favour higher prices

Beyond demand, lithium’s market dynamics are also starting to favour higher prices.

‘We are entering a seasonally strong period on the demand side,’ Williams noted, adding that port inventories for the raw material have started to diminish.

As of July, China had about 140,000 tonnes of lithium in inventory.

But once that stockpile is used up, nothing will be holding prices back.

Furthermore, China’s supply outlook has become murky after the government’s attempt to control capacity left producers at the mercy of regulators.

For example, in the lithium hub of Yichun, the fate of a mine run by the world’s biggest EV battery maker (Contemporary Amperex Technology Co., or CATL) is still undecided.

The project was halted in August because its permit was not renewed.

This regulatory uncertainty is limiting supply, which should support prices.

Overall, positive signs for lithium.

Regards,

Lachlann Tierney,

Australian Small-Cap Investigator and Fat Tail Microcaps

***

Murray’s Chart of the Day – Australian 10-year bond yield

Source: TradingView

With Aussie inflation numbers surprising the market recently, bond yields have been jumping higher.

Australian 10-year bonds have seen a sharp spike in yields from 4.10% to 4.70% in the last couple of months.

That is definitely an unexpected development that will have analysts revisiting their predictions for markets over the next year.

The 10-year bond yield hasn’t been above 5% since 2011. You can see in the chart above it tested that level in late 2023.

We are now just 30bps below that level.

A breakout above there would certainly place some downward pressure on Aussie stock valuations.

So it is something to keep your eye on as we head towards 2026.

Regards,

Murray Dawes,

Retirement Trader, International Stock Trader and

Murray’s Trading Room

Comments