1) Mr Market is up to his old tricks again. Nothing we all expected to happen…is happening!

Case in point is the big sell off we’re due, according to some, thanks to the Trump tariffs. So far it lasted one day.

Crash? Unlikely.

There’s a known problem with this line of thinking.

We all knew about the potential for tariffs. It was obvious.

The market has already, always, priced in what is obvious. It’s the thing you don’t know that can get you into trouble.

I’ve tabled the opportunity to go long on iron ore with the current dynamic in mind over the last few weeks.

Thus far iron ore is resilient too. It closed at US$106 per tonne yesterday. FMG is up 7% in recent trade, and ready to dump dividends all over its shareholders again. I’ve picked up a few for the yield in recent weeks.

That said, iron ore lacks the explosive potential to really break out in the short term, as gold has done over the last 12 months.

Where else can we look?

The obvious place to start is with the copper market. Here’s resource journalist Barry Fitzgerald with the basic case…

‘The copper price has been hanging together nicely despite the economic uncertainty that comes when a heavyweight like the US starts imposing tariff walls against friends and foes alike.

‘The red metal is known to be a bellwether of economic activity and so far at least, its $US4/lb-plus price handle says that while uncertainty has increased, the scale of the tariffs will be something much less than originally proposed by the White House on X.

‘Besides, copper it seems, will be OK, in the longer term anyway. The supply pressures coming from falling grades, mine exhaustions, approval delays and a lack of new developments – all at a time when the global electrification effort is in full swing – is an enduring thematic, unlike the politics of the day.’

It’s a familiar argument. However, I go along with it. The hard part is finding a way to play it.

I told you last week that the big fund managers could go for BHP and Rio Tinto because of their copper exposure.

But they’re less than ideal for you and me. They’re so big it’s hard to get their price to shift without big price moves in physical copper and iron ore.

2) To have a shot at a solid return – I’m talking a chance to double your cash – we need to throw something else into the mix.

What?

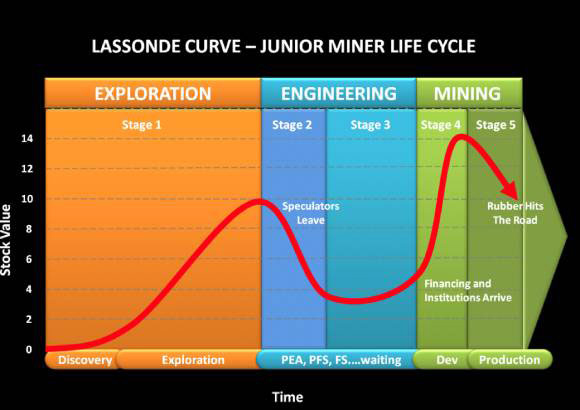

The Lassonde Curve is my favourite idea here. Do you know it?

A man named Pierre Lassonde was the founder of one of the first gold royalty companies.

30 years ago, he created a theoretical ‘curve’ to outline the life cycle of a junior mining company.

It looks like this:

| |

| Source: KJ Kuchling Consulting |

You want to position in these stocks at a certain time for the best chance of a fast up move.

Obviously, the biggest and riskiest phase is the exploration phase — you’re always dancing with the gods on that one.

The second and ideal phase to position for a strong up move is as a project ‘derisks’ in the eyes of the market toward first production.

If they hit their milestones to production, the market will bid up the stock to access the incoming cashflows.

This is the best part of the ‘Lassonde Curve’, after adjusting for risk.

In my service Australian Small-Cap Investigator, we’ve ridden this with great success before with Bellevue Gold [ASX:BGL] and, last year, Spartan Resources [ASX:SPR].

I’ve just recommended my latest idea to ride the Curve, last month.

Can we get third time lucky? No guarantees, small caps carry a high degree of risk, but the odds look bang on to have a crack.

You can get the story, including the name and ticker, by clicking on this link. You don’t have to subscribe or pay for anything.

Feel free to let me know what you think of the idea.

3) One final thing to think on when it comes to copper.

Analyst David Goldman points out that gold broke out of the general metal complex over the last few years.

See for yourself…

| |

| Source: David Goldman |

This is the market moving to protect itself from the general heightened level of systematic risk. Physical gold is a hard asset, with no counterparty risk.

So is copper. It just doesn’t have the same golden glamour. At some point, it’s easy to envisage a scenario similar to the years before 2008…where commodities were seen as a hedge against other asset classes.

In other words, I expect copper and the other metals to follow gold higher in the years ahead.

Best wishes,

|

Callum Newman,

Editor, Small-Cap Systems and Australian Small-Cap Investigator

Comments