This plea is NOT to central bankers or policymakers.

Their bloated egos, gross stupidity, and blatant self-interest rendered them deaf to anything other than fawning (but very much undeserved) applause and accolades.

No, dear reader, this plea to stop and listen to history is for you.

Personal responsibility is THE ONLY thing that’s going to protect your capital.

History is once again repeating itself.

The recent frantic sell-off in UK Government bonds and the British pound took British pension funds to the brink of insolvency:

‘LONDON, Sept 30 (Reuters) — British pension funds with big losses in gilt market derivatives have sought emergency funds from the companies they manage money for as they race to dump assets to raise cash, industry sources said on Friday.’

Compelled to do ‘whatever it takes’, the Bank of England (BoE) intervened to restore relative calm. Crisis averted…for now.

But if history tells us anything about asset bubbles, it’s that there’s never just one ‘mole’ in the bubble-deflating ‘whack-a-mole’ arcade show.

The trigger for the panicked sell-off was a little-known investment vehicle called…

Liability-driven investing (LDI).

What is it?

LDI is employed by pension funds to manage the risk of matching the return on current assets against future liabilities (indexed pension payments for members who are living much longer). Not an easy task in a world where traditional safe havens — like government bonds — yield next to nothing.

This headline tells you the basics of the LDI strategy:

|

|

| Source: Pension & Investments |

The article carried this confession from an industry insider (emphasis added):

‘Jeff Passmore, LDI solutions strategist at MetLife Investment Management, said the situation with U.K. pension plans “has been challenging, and the heavy use of derivatives in the U.K. LDI model has made the current situation worse than it would otherwise be.”’

A nuclear weapon in the hands of madmen

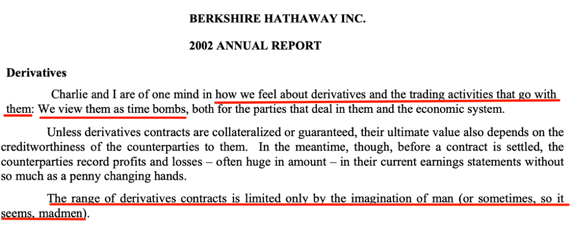

Here’s what Warren Buffett had to say about derivates 20 years ago:

|

|

| Source: Berkshire Hathaway |

In good times (and the past decade or so, just hasn’t been good, it’s been great for asset managers) lessons of the past get forgotten.

The longer and stronger the UP cycle, the more imaginative the investment strategies become…greed transforms people into madmen.

Buffett witnessed these transformations in the dotcom boom.

And here we are again…but only on a far greater scale. What was once a time bomb is now a nuclear weapon.

And it’s not like the BoE were unaware of the risk with LDIs.

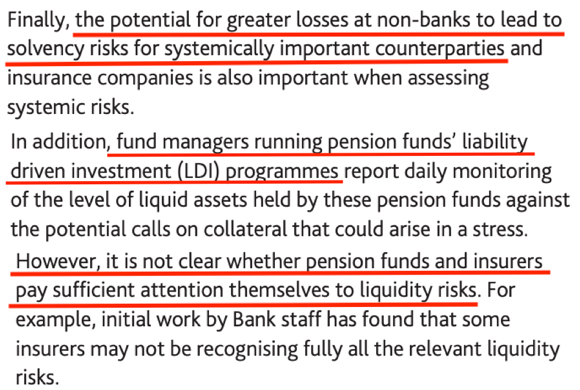

This is a composite from page 54 of the ‘Bank of England’s November 2018 Financial Stability Report’:

|

|

| Source: Bank of England |

Blind eyes get turned in a boom

The longer something doesn’t happen, the greater the belief in ‘it won’t happen’ grows…encouraging the ‘madmen’ to take on even more risk.

On its reporting of the UK meltdown, financial site Proactive Investors

(emphasis added):

‘Of course the risks of leveraged financial instruments [like LDIs] is nothing new, the cycle goes full circle as investors and regulators gradually forget, forgive or ignore the lessons of past crises and attitudes to risk change.

‘Memories of LTCM spring to mind — brought to its knees by the devaluation of the Russian rouble which sent US markets into freefall.

‘As a result, LTCM’s highly leveraged investments crumbled and by the end of August 1998, it had lost 50% of the value of its capital investments, pushing a number of banks and pension funds that had invested in LTCM close to bankruptcy.’

What we’ve seen play out in previous booms and busts — from tulips to tech stocks — is a predictable and repeatable pattern of behaviour.

The difference this time is the extent of the risk-taking and overvaluation within the system:

- Debt levels have never been greater.

- The global derivatives market — according to Investopedia — is more than US$1 quadrillion (that’s more than US$1,000 trillion)

- At their respective peaks, asset prices — shares, bonds, property, cryptos — have never been higher.

We have an economic and financial system that’s extremely fragile and highly vulnerable to the pressures of:

- Higher inflation.

- Rising interest rates.

- Climate policies taking us back to the 17th century.

- Wage demands.

- Geopolitical tensions.

- Social unrest.

The hidden risks within a highly leveraged, overly confident, and interconnected marketplace were the subject of the July 2019 issue of The Gowdie Letter.

Here’s an edited extract:

‘The power surges in markets

‘Every second of every day, live currents (money flows) are powering up markets…currencies, derivatives, shares, property, bonds, cryptos, commodities (agricultural, mineral, and livestock), private equity, venture capital.

‘And within these markets there are offshoots of other markets. In the bond market there are Government Bonds, Corporate Bonds, Junk Bonds. There is small-, mid-, and large-cap stocks. Commercial, residential, industrial, rural property markets.

‘In addition to the primary market, there are a myriad of structured products — designed primarily by the investment industry for fee generation purposes — that are manufactured to access a variety of “opportunities”.

‘Then there’s the interconnectivity of cables between markets — interest rates to property values to share prices to currency fluctuations to bullion price.

‘If someone could draw a flow chart of the power lines that exists within and between markets it would look like a giant bowl of spaghetti.

‘There are times when the voltage (money) flowing through certain markets — cryptos, subprime debt, tech stocks, corporate debt, margin lending, et al — is sufficient to power a major city.

‘The red glow coming from the cables powering these “hot” markets should serve as a warning…but somehow the danger remains invisible…even to the trained eye.

‘You may recall this from May 2007…

‘“We believe the effect of the troubles in the subprime sector on the broader housing market will be limited and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system,” [Ben] Bernanke said.

‘The person charged with the smooth operation of the world’s economic generator, had absolutely no idea that the subprime power cable was connected into the financial and economic grid.

‘If Bernanke didn’t see it, what hope did the average home handyman (investor) have?

‘But Bernanke had no excuse for not knowing. These red-hot power surges aren’t without precedent.

‘In the 1990s, a firm called Long-Term Capital Management (LTCM) was founded by highly trained and well qualified “sparkies” — John Meriwether (former head of fixed interest trading at Salomon Brothers) and two Nobel Prize-winning economists Myron Scholes and Robert Merton.

‘The founders all came to the table with extensive experience in investing in derivatives…they knew how to outperform the market.

‘[With LTCM] [t]here was leverage upon leverage — [the management] turning US$4 billion of equity into US$1 trillion of notional principal.

‘Did the Nobel Prize-winners not see the dangers in this structure?

‘LTCM was like one of those DIY disasters where you have multiple extension cords plugged into a multitude of power boards…running alongside the bathtub and pool.

What could possibly go wrong?‘The power cables connecting LTCM where…investor equity to lenders to derivative contract counterparties to the US banking system.

‘No one saw the danger in all these exposed cables lying around Wall Street.

‘How was it possible for all these trained professionals to not see danger? According to the Berkeley University report (emphasis added):

“Surely LTCM, with two of the original masters of derivatives and option valuation among its partners, would have put its portfolio through stress tests to match recent market turmoil. But, like many other value-at-risk (Var) modellers on the street, their worst-case scenarios had been outplayed by the horribly correlated behaviour of the market since August 17. Such a flight to quality hadn’t been predicted, probably because it was so clearly irrational.”

‘The industry thought — wrongly — that the Nobel Prize winners would have rigourously safety tested the products “power cords” to ensure they could handle an unexpected power surge…afraid not.

‘Please take note of the language used in highlighted section…horribly correlated behaviour and clearly irrational.

‘Professional market players were “shocked” by people panicking when the invisible danger became visible. Really? What did they expect, some sort of gentlemanly “You first. No, I insist you go first” discourse?

‘Human nature — especially when it moves to the extremities of the emotional scale- is a highly visible “known known”…been happening ever since Tulip Mania in the 1600s.

‘The failure to factor this obvious risk into the stress test was a grave oversight.

‘In the end, the New York Fed organised for 11 banks to provide US$3.6 billion in funding for the bail-out of LTCM.

‘Crisis averted.’

Learn from history or your capital will be history

The Fed (and its central bank counterparts) DID NOT learn (or have completely ignored) the lessons from LTCM, the dotcom boom and bust, the US Housing bubble, and GFC bust.

Each one of these financial disasters has been an exercise in progressively increased intensity.

The current asset bubble dwarfs all others.

Therefore, its implosion should come with a force unlike anything we’ve ever experienced.

What happen in London a couple of weeks ago was an early warning sign…similar to Bear Stearns in early 2008.

We are building to a Lehman Brothers moment.

The only way to avert this crisis is by taking personal responsibility for the stewardship of your money.

PLEASE, PLEASE, PLEASE listen and learn from history…if you don’t, then your capital will be history.

Regards,

|

Vern Gowdie,

Editor, The Daily Reckoning Australia