‘The crisis consists precisely in the fact that the old is dying and the new cannot be born; in this interregnum a great variety of morbid symptoms appear.’

—Antonio Gramsci

This is part three of my piece, Our Modern Interregnum. Click the link for the first section.

Today, I look at the structural costs borne by this crisis. The atrophied arms of the West. Then I look at the incentives that drove us to this point.

Because Globalisation was far more than just free trade. It was the financialisation of everything.

In that framework, cost reduction became the overriding imperative. Every cost a nail. Every market the hammer.

***

Central banks can create trillion-dollar credits with a keystroke while 555 aluminium components remain unavailable at any price.

The financial framework persists. The conversion it assumes does not.

This is our version of Gramsci’s morbid interregnum. The old intellectual framework has persisted since the beginning of this globalisation movement.

Financial hegemony of the West. Frictionless globalisation. The assumption that liquidity cures scarcity. These ideas are dying.

But its structures continue to govern. Simply because the new framework has not yet achieved hegemony.

The morbid symptoms multiply.

Morbid Symptoms

Once the interregnum is understood as structural rather than episodic, individual events cease to appear as isolated shocks and reveal themselves as symptoms of a single underlying condition.

Said another way, our modern crises follow the same pattern:

Financial logic drives the closure or degradation of physical capacity. The closure creates a dependency on external supply. The dependency creates a vulnerability. The vulnerability materialises as a crisis.

The crisis is treated as exceptional (a monster) rather than diagnosed as a morbid symptom of the structural condition. We’re seeing this play out in real-time in the Strait of Hormuz.

Australia’s gas paradox: Australia is the world’s third-largest LNG exporter. It sits on vast reserves. Yet domestic gas prices in eastern Australia tripled over the decade following the Queensland LNG export boom.

83% of all gas produced in 2025 was shipped offshore. Factories in the fertiliser, chemicals, plastics, and glass industries continue to close.

In recent years, thousands of manufacturing jobs were lost directly to high energy costs, with more under threat. Now we have warnings of structural gas shortfalls from 2028.

The Financial Ledger recorded a decade of export revenue. The Material Ledger recorded an industrial base priced out of its own energy supply. A country that sells its gas to the world and then watches its own manufacturers close for want of affordable fuel.

The three LNG consortia paid no corporate tax for almost a decade. The cost to Australian businesses and consumers was estimated in the tens of billions.

The industrial gas divergence: In February 2025, Air Products cancelled three major US projects and took a $3.1 billion write-down.

These were creatures of the Financial Ledger: green hydrogen and sustainable aviation fuel projects designed to harvest tax credits.

They failed the Material Ledger test: physically expensive and dependent on a premium the market refused to pay.

Meanwhile, Air Liquide expanded in Asia, acquiring operating gas units from Wanhua Chemical in China. Industrial gases are the lungs of the industrial base. You cannot make steel without them.

The world’s lung capacity is being embedded in China’s ecosystem because that is where capital can actually be converted into physical output.

<The rare earth stranglehold: China controls roughly 70% of global rare earth production.

More consequential is its grip on the downstream value chain: over 90% of oxide separation, metal refining, and magnet production.

It holds a near-total monopoly on dysprosium and terbium; elements essential for the permanent magnets used in F-35 fighters, Virginia-class submarines, electric vehicle (EV) motors, and wind turbines.

This dominance did not arise by accident. Beijing has invested with intention since the late 80s, treating processing facilities as strategic infrastructure rather than commercial ventures.

It tolerated environmental costs and subsidised production at prices that destroyed Western competitors. The same playbook it used in graphite, PVC, and solar panels.

The West did not merely fail to compete; it chose not to.

The Mountain Pass mine in California, one of the world’s richest rare earth deposits, operated for years without integrated refining, shipping ore to China for separation.

When Beijing restricted exports of seven critical elements and rare earth processing equipment in late 2025, Western manufacturers discovered that money could not buy what only one country knew how to make.

Total Chinese shipments of rare earth magnets fell 74% in a single month. The pain was immediate across the automotive, electronics, and defence sectors.

The IEA recently confirmed our underlying reality: 19 out of 20 important strategic minerals are refined by China.

This reality wasn’t just forged by China’s hand. We’ve also had a stake in our own demise.

The Incentive Architecture

There is a mechanism that connects these symptoms. It’s not a conspiracy. It’s the incentive structure.

For forty years, the Western professional class and elites operated under a framework that systematically rewarded the liquidation of physical capacity.

The incentives were coherent, mutually reinforcing, and devastating in aggregate.

Executive leadership compensation was tied to share price and quarterly earnings. The fastest route to both was cost reduction: close the domestic plant, offshore production, strip the balance sheet of physical assets, and return the savings to shareholders via buybacks.

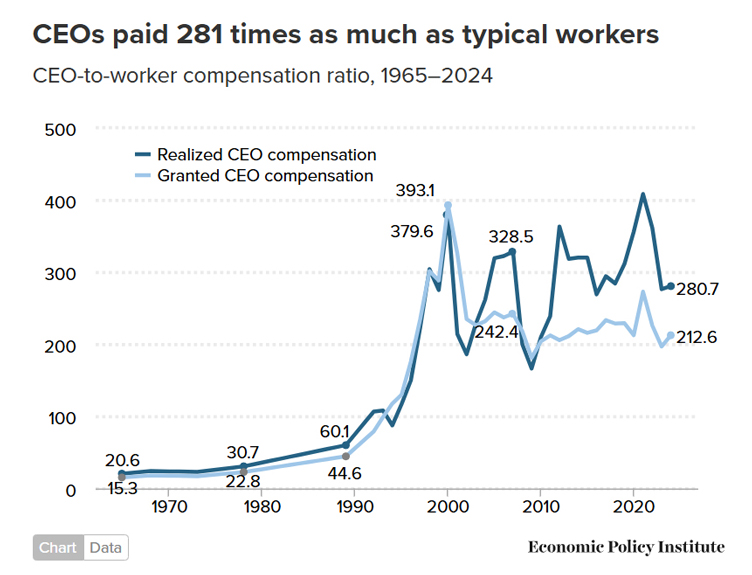

While manufacturing jobs were being lost in droves. CEO pay soared to many hundreds of times the typical worker’s pay.

Source: Economic Policy Institute

[Click to open in a new window]

Meanwhile, Wall Street rewarded ‘asset-light’ business models with higher multiples. A company that owned nothing and outsourced everything traded at a premium to one that maintained factories and employed skilled workers.

The logic was internally consistent: if you could buy the input cheaper from China, why produce it yourself?

Fund managers reinforced this by punishing companies that invested in long-cycle physical capacity — mines, smelters, chemical plants — whose returns measured in decades rather than quarters.

Capital flowed toward software, financial engineering, and platform businesses with high margins and minimal physical footprint.

Commodities suffered as the digital economy flourished.

The consulting class provided the intellectual justification, repackaging deindustrialisation as ‘focusing on core competencies.’

Politics favoured globalised trade deals and specialisation over individual resilience. Multinationals defined our mutual engagements and eroded our laws.

Central banks backstopped the entire arrangement with cheap credit, ensuring that any temporary friction in the supply of physical goods could be papered over with liquidity.

That cheap credit structurally favoured those who already held wealth and power. Those with wealth could borrow more and ultimately own a larger share of these diminished assets.

No individual in this chain set out to destroy Western productive capacity or create strategic dependency on a rival. Each acted rationally within the prevailing moment.

<p”>But the accumulated weight of millions of individually rational decisions produced an outcome that was collectively ruinous.***

The tide is now turning. In my last part tomorrow, I’ll outline three potential futures to this crisis.

One of those futures has a clear investable path. And that’s what my colleague Lachlann Tierney covers in his new investment thesis.

It’s called Pax Silica. Click here to view his latest presentation.

Tomorrow, we’ll look at how this interregnum can end.

Until then.

Regards,

Charlie Ormond,

Small-Cap Systems and Altucher’s Investment Network Australia

***

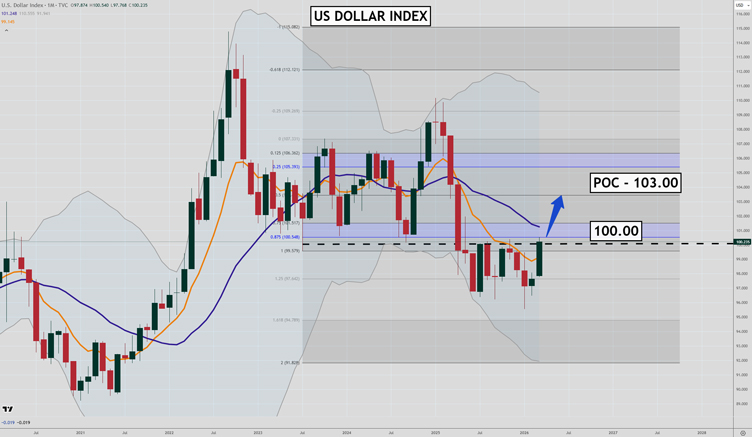

Murray’s Chart of the Day – US Dollar Index

Source: TradingView

The US Dollar Index [TVC:DXY] looks primed for more upside after spending the last year stuck in a range between 96.00 and 100.00.

The psychologically important level of 100.00 was strong support from 2023 to 2025, and then became stiff resistance in 2025 after it couldn’t hold.

The long-term trend for the US Dollar Index remains down, so a rally could meet strong selling pressure, and the downtrend could resume.

But in the short term, the risk is to the upside, with a breakout above 100.00 targeting 103.00.

That is the Point of Control, or midpoint, of the range the US Dollar Index has traded in over the past three years.

Regards,

Murray Dawes,

Retirement Trader and International Stock Trader

Comments